Table of Contents >> Show >> Hide

- 1. Why do stocks sometimes go up even when the economy feels bad?

- 2. Are interest rates still the main thing investors should watch?

- 3. Is inflation still the biggest threat to the economy?

- 4. If the job market is still decent, why are people worried about recession?

- 5. Are stocks too expensive right now?

- 6. Does the economy really matter more than company earnings?

- 7. What should ordinary investors actually do with all this information?

- Final Thoughts on Stocks, Inflation, Rates, and the Bigger Picture

- Personal Experience and Real-World Reflections on Stocks & The Economy

Trying to understand stocks and the economy can feel a little like trying to read a restaurant menu during an earthquake. One minute everyone is cheering about a “soft landing,” the next minute somebody on TV is waving a chart like it’s the final clue in a national treasure hunt. Markets go up, inflation cools, rates stay high, jobs look solid, and somehow people still feel weirdly nervous. Welcome to modern investing.

This is exactly why so many readers keep asking the same big questions: Why do stocks rise when the economy feels shaky? Why do interest rates matter so much? Is inflation still the villain, or just an annoying side character now? And perhaps the most emotionally loaded question of all: should normal people be doing anything differently with their money?

In this article, we’ll walk through seven practical questions about stocks and the economy in plain American English, with zero jargon confetti and only the amount of market drama strictly required by law. The goal is not to predict the future like a financial wizard in a navy suit. The goal is to understand what matters, what doesn’t, and why the stock market can behave like an overcaffeinated golden retriever while the broader economy moves more slowly.

1. Why do stocks sometimes go up even when the economy feels bad?

This is the first great mystery. People hear about layoffs, high grocery bills, expensive mortgages, and political uncertainty, then glance at the market and see major indexes acting like everything is fabulous. It feels rude. But the stock market is not the economy. It is a forward-looking machine that constantly tries to price in what investors think will happen next.

That means stocks do not wait for the economy to look pretty. They often start moving before headlines improve. If investors believe inflation is cooling, earnings will hold up, or the Federal Reserve may eventually cut rates, stocks can rally even while households still feel pressure. In other words, Wall Street is often trading six to twelve months ahead, while Main Street is trying to survive this month’s utility bill.

There is another wrinkle: stock indexes are not equal-weight popularity contests. A small group of giant companies can pull the whole market higher, even if many smaller companies or sectors are struggling. So when someone says, “the market is up,” that does not always mean every stock is thriving. Sometimes it means a handful of heavyweight firms showed up in superhero capes and carried the index on their backs.

2. Are interest rates still the main thing investors should watch?

They are not the only thing, but they are still a very big thing. Interest rates influence borrowing costs for businesses, mortgage rates for families, credit card pain for nearly everyone, and valuation math for stocks. When rates are high, money is more expensive. Companies may slow expansion, consumers may spend more carefully, and investors become pickier about how much they are willing to pay for future profits.

Growth stocks are especially sensitive to this. Why? Because much of their value depends on earnings expected years into the future. When rates rise, those future earnings are discounted more heavily, making expensive stocks look less attractive. That does not mean every tech or AI-related stock is doomed. It means the market stops giving out sky-high valuations like free samples at a warehouse club.

At the same time, higher rates can make bonds and cash-like investments more competitive with stocks. If investors can earn a decent yield with less risk, they may demand more from equities before jumping in. This is why rate policy matters so much: it quietly changes the entire menu of investment choices.

What this means for regular investors

If you are building a long-term portfolio, do not treat every Fed meeting like the Super Bowl. But do understand the broader theme: interest rates and stocks are tightly connected, and rate expectations often shape market mood long before the economy fully reflects the change.

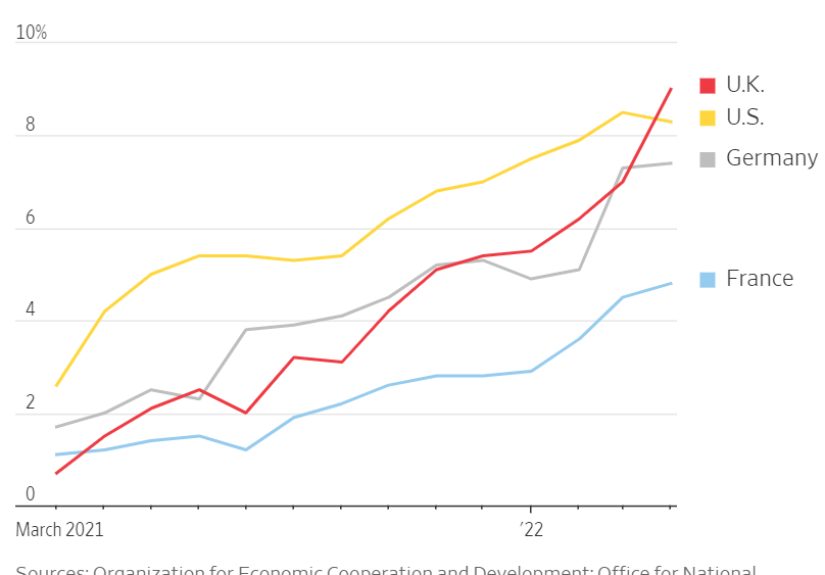

3. Is inflation still the biggest threat to the economy?

Inflation has cooled from its ugliest peak, but it is not fully gone from the conversation. That matters because inflation changes how consumers behave, how companies price products, and how aggressively the Fed thinks it needs to act. Even when headline inflation improves, sticky areas like services, housing-related costs, and everyday essentials can keep people feeling squeezed.

This is one of the most misunderstood parts of the economy and stock market story. Inflation does not have to be at crisis levels to affect sentiment. If prices are still higher than people are comfortable with, households may cut back on discretionary spending. That can affect retailers, travel companies, restaurants, and other consumer-driven businesses.

For investors, the key question is not simply, “Is inflation up or down?” It is, “Is inflation moving toward a range where the Fed can relax without reigniting price pressures?” That answer influences rate policy, wage dynamics, profit margins, and ultimately stock valuations. So yes, inflation still matters. It is just less of a horror movie monster now and more of a stubborn houseguest who keeps saying, “I’ll leave after one more coffee.”

4. If the job market is still decent, why are people worried about recession?

Because the economy is rarely all good or all bad at once. A strong labor market can coexist with slower growth, cautious consumers, tighter credit, and business uncertainty. Jobs data is one of the most important indicators in the U.S. economy, but it is not the whole economy. A healthy unemployment rate does not automatically guarantee smooth sailing.

Recession fears usually come from a combination of signals: slower GDP growth, weakening manufacturing activity, tighter lending standards, lower corporate confidence, and concern that high rates could eventually do more damage than expected. Investors also watch the yield curve and other market-based indicators because financial markets tend to sniff out trouble before official declarations arrive.

That is why headlines can seem contradictory. You may read that payroll growth continues and unemployment remains relatively contained, then hear analysts warn about downside risks. Both can be true. Economic slowdowns often begin quietly. They do not send an engraved invitation.

The practical takeaway

Do not judge the entire U.S. economy by one data point, whether it is jobs, inflation, or GDP. The market reacts to the full mosaic. And like all mosaics, it looks clearer from a distance than when your face is pressed against one oddly shiny tile.

5. Are stocks too expensive right now?

This is the question that launches a thousand nervous portfolio checkups. The honest answer is: some are, some are not, and the answer changes by sector, company quality, earnings expectations, and how much optimism investors have already priced in. Broad indexes can look reasonably valued by one measure and stretched by another, especially when a few mega-cap names dominate performance.

Valuation matters, but it is a terrible short-term timing tool. A market can stay expensive for longer than impatient investors can tolerate. A cheap market can stay unloved for months. What valuation does tell you is something more modest and more useful: elevated prices may lower future returns and increase the odds of volatility, especially if earnings growth fails to justify the optimism.

This is why investors should separate two questions that often get mashed together:

Question one: Are stocks overpriced right now?

Question two: Should I stop investing altogether?

Those are not the same question. A market can be pricey and still worth approaching through a disciplined, diversified plan. Stopping entirely because things look “too high” has burned many investors who waited for a perfect entry point that never arrived.

6. Does the economy really matter more than company earnings?

In the long run, company earnings matter enormously. Stocks are ownership in businesses, not magic beans. Over time, profits, margins, innovation, balance sheets, and competitive advantage drive returns. But the economy creates the backdrop in which those earnings either flourish or struggle.

Think of the economy as the weather and company fundamentals as the quality of the house. A strong house can survive a storm better than a weak one, but even excellent companies do not operate in a vacuum. Consumer demand, wage pressure, interest costs, currency moves, regulation, and business confidence all shape earnings results.

This is why the market swings so wildly during earnings season and macro announcements. Investors are constantly trying to answer a layered question: how much of a company’s future depends on its own execution, and how much depends on the economic environment? The answer differs from industry to industry. Utilities and consumer staples may respond differently than semiconductor firms, banks, or homebuilders.

So yes, the economy matters. But investors who obsess only over macro headlines and ignore earnings quality risk missing the point. The best long-term investing decisions usually happen when you respect both: the economic backdrop and the business itself.

7. What should ordinary investors actually do with all this information?

First, breathe. Second, stop trying to out-scream the market. Most people do not need a hotter take. They need a repeatable process. That process usually includes diversification, realistic time horizons, steady contributions, and a willingness to accept that markets are occasionally dramatic for no excellent reason.

If you are investing for long-term goals, this environment does not require clairvoyance. It requires discipline. Diversification still matters because no one knows which asset class, sector, or region will lead next. Chasing whatever just had a great year is one of the oldest and most expensive hobbies in finance. It is right up there with timing the market based on vibes.

Dollar-cost averaging remains useful for investors who are building positions over time. It removes the pressure of needing to call the perfect bottom. Asset allocation matters more than many investors realize, because the mix of stocks, bonds, and cash often determines how much risk you can actually tolerate when markets get ugly.

And perhaps most important: match your strategy to your life, not to social media. A 22-year-old investing for retirement, a 45-year-old funding college and retirement at once, and a 67-year-old living off portfolio withdrawals should not all behave the same way just because a guy online made a chart with arrows and a fire emoji.

Final Thoughts on Stocks, Inflation, Rates, and the Bigger Picture

The relationship between stocks and the economy is complicated because markets are forward-looking, people are emotional, and economic data arrives in pieces rather than with a tidy narrator explaining everything. Stocks respond not only to what is happening now, but to what investors expect next. The economy affects earnings, rates affect valuations, inflation affects policy, and all of it filters through human psychology, which has never once been accused of being calm.

That is why the smartest approach is usually not to chase certainty, but to build understanding. Ask better questions. Watch the big indicators without worshipping them. Focus on long-term financial habits. And remember that the market can be wrong in the short run, weird in the medium run, and still rewarding over the long run for investors who stay disciplined.

In other words, you do not need to predict every twist in the economy. You just need a plan sturdy enough to survive the plot.

Personal Experience and Real-World Reflections on Stocks & The Economy

One of the strangest experiences about following the stock market is realizing how often your personal life and the market headlines seem to be living in different zip codes. You might walk out of a grocery store holding one bag and a receipt that looks like a ransom note, then open your phone and see a headline announcing that investors are “celebrating resilience.” Celebrating with what, exactly? Half a carton of eggs?

I have had seasons where the economy felt abstract until it hit something specific: rent negotiations, insurance premiums, travel costs, a surprise car repair, or the moment a monthly subscription pileup starts looking like a tiny hostile takeover. Those are the moments when macroeconomics stops sounding academic and starts sounding personal. Inflation is no longer a chart. It is the reason you suddenly develop a deep emotional relationship with store-brand pasta.

The same thing happens with stocks. In theory, investing sounds rational and elegant. In practice, many people check their accounts after a red day and immediately become part-time philosophers. “What is value?” “What is patience?” “Was I foolish to buy that index fund on a Tuesday?” The emotional side of investing is real. Even disciplined investors feel it.

I have also noticed that people tend to swing between overconfidence and total doom. When markets rise, everyone suddenly becomes a strategic genius. When they fall, people start talking like the financial system is one missed earnings report away from becoming a barter economy. Most of the time, reality is less cinematic. The economy bends, slows, reaccelerates, absorbs shocks, and keeps moving. Markets panic, recover, overreact, and repeat.

What has proved most useful over time is not having perfect predictions. It is building habits that still make sense when predictions fail. Saving consistently. Staying diversified. Not assuming the latest winning trade is a permanent law of nature. Understanding that headlines are designed to grab attention, while real wealth-building usually happens through boring consistency.

There is also something humbling about watching how quickly narratives change. One quarter the market is obsessed with inflation. The next it is growth. Then it is rates. Then earnings. Then AI. Then geopolitics. Then suddenly everyone has rediscovered “quality” as if it was buried in a backyard for years. This is why a calm process beats a dramatic personality.

For ordinary investors, the biggest lesson may be this: you do not have to feel fully comfortable to make smart decisions. You can feel uncertain and still contribute to your retirement account. You can worry about the economy and still rebalance your portfolio. You can admit that nobody knows exactly what stocks will do next and still invest with purpose. That combination of humility and discipline is underrated. It is not flashy, but neither is financial regret, and regret tends to hang around longer.