Table of Contents >> Show >> Hide

- The venture market is not dead. It is just extremely picky.

- EY’s central message: dollars up, deals down

- Why AI is absorbing so much venture capital

- But the AI boom is not evenly distributed

- Why deals are down outside the AI spotlight

- The Bay Area is back at the center of gravity

- What founders should do now

- What investors should watch

- Practical experience: what this market feels like from the trenches

- Conclusion: venture is recovering, but not returning to normal

Venture capital has entered one of those confusing seasons where the headline number and the hallway conversation seem to be arguing with each other. On one side, the dollars are back. Big checks are flying again, especially into artificial intelligence companies with infrastructure needs, foundation-model ambitions, enterprise AI platforms, and enough compute demand to make a data center blush. On the other side, many founders are still hearing the dreaded phrase: “We love what you’re building, but we’re going to wait.” Translation: the venture market has money, but it is not sprinkling it around like confetti at a 2021 startup party.

That is the big message behind recent EY venture capital analysis: venture investment is up in dollar terms, but the number of deals is still down. AI is not just participating in the market. It is lifting the market, tilting the market, and, in some quarters, practically dragging the market by the hoodie strings.

For founders, investors, limited partners, and anyone trying to decode startup finance without needing three coffees and a spreadsheet therapist, the story is simple but not small: venture capital is recovering unevenly. The winners are getting larger rounds. The middle is getting squeezed. The “AI premium” is real. And for everyone outside the AI spotlight, the bar for funding has become much higher.

The venture market is not dead. It is just extremely picky.

The biggest mistake people make when reading venture headlines is assuming that more dollars means more opportunity for everyone. That is not what the data suggests. Venture capital today looks less like a rising tide lifting all boats and more like a few very large yachts making the harbor look busy.

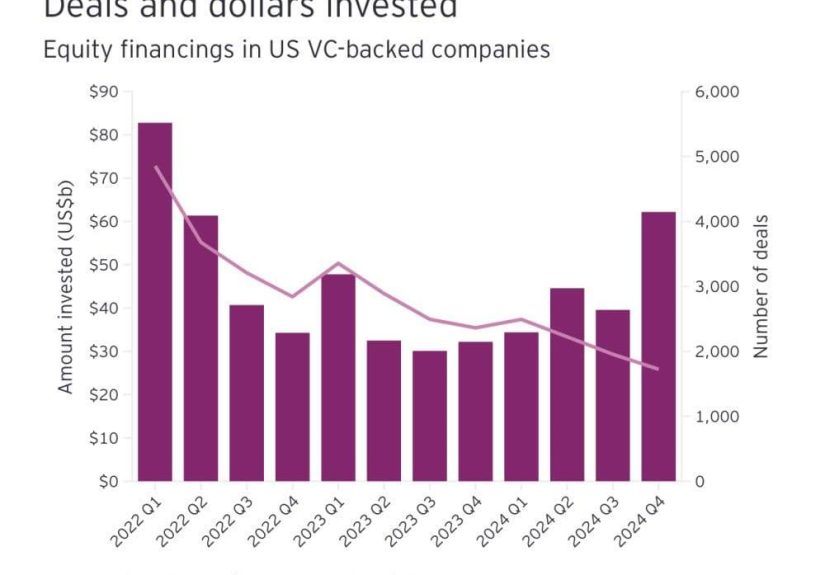

EY reported that U.S. VC-backed companies raised more than $62 billion in Q4 2024, a major jump from Q3. The quarter was powered by several huge AI deals, and AI represented more than 60% of all Q4 fundraising. That sounds like a roaring comeback until you notice the other half of the equation: the total number of VC deals fell below 10,000 for the year, the lowest annual level since 2012.

In other words, the venture capital market is not short on conviction. It is short on broad conviction. Investors are willing to write very large checks when they believe a company sits directly in the path of a massive platform shift. They are much less willing to fund companies that look like “nice-to-have” software, incremental consumer apps, or business models still relying on yesterday’s growth math.

This is why many startup founders feel whiplash. They read that venture funding is up, then pitch 40 funds and receive 39 polite rejections plus one “circle back in Q3.” The reason is not imaginary. The market is concentrated.

EY’s central message: dollars up, deals down

EY’s analysis captures the split personality of today’s venture capital market. Q4 2024 delivered one of the strongest funding quarters since the post-2021 reset, but the strength came from a narrow group of AI-centered companies. Then Q1 2025 continued the theme, with a single massive AI transaction dramatically lifting the entire quarter.

Q4 2024: AI pushed the market higher

In Q4 2024, venture-backed companies raised more than $62 billion, and four large AI deals accounted for more than $26 billion of that total. That is not a normal distribution. That is a venture capital elephant standing on one side of the seesaw.

EY also noted that 2024 became the third-largest year on record for U.S. venture investment, but the achievement comes with a giant asterisk: fewer companies captured more of the money. AI-driven deals increased dramatically from the prior year, and mega-rounds became the defining feature of the market.

That means the venture ecosystem is recovering in value before it is recovering in volume. Investors are not yet funding a wide range of startups at a healthy pace. They are backing fewer companies with bigger checks, especially when those companies can plausibly claim a role in AI infrastructure, AI software, model development, semiconductors, data platforms, cybersecurity automation, enterprise productivity, or energy demand tied to compute.

Q1 2025: one AI deal changed the entire picture

Q1 2025 made the concentration even clearer. EY reported that VC-backed companies raised about $80 billion in the quarter, the strongest level since Q1 2022. But that headline was heavily influenced by a single $40 billion AI deal. Without that deal, EY said venture investment would have declined sharply from Q4 2024.

That is the cleanest summary of venture today: the market can look hot from 30,000 feet and cold from the founder’s pitch deck. One mega-round can make the quarterly chart look beautiful. It does not mean seed-stage SaaS founders are suddenly being chased through parking lots by investors waving term sheets.

EY also reported that the number of $100 million-plus transactions fell in Q1 2025 compared with Q4 2024. So even inside the world of mega-rounds, investors were becoming more selective. Big AI dollars were still up, but they were not automatically spreading across every company with “agent,” “copilot,” or “LLM-powered” in the tagline. The market has learned to ask the rude but necessary question: “Is this actually a business, or is it a demo with a nice gradient background?”

Why AI is absorbing so much venture capital

AI is attracting capital for three main reasons: market size, infrastructure intensity, and strategic urgency.

First, the market size is enormous. Generative AI, agentic AI, machine learning infrastructure, enterprise automation, AI security, AI data tooling, and domain-specific AI applications all point toward large future markets. Investors are not just betting on one product category. They are betting on a computing platform shift.

Second, AI is expensive to build. Frontier model development, high-performance computing, specialized chips, data centers, energy contracts, technical talent, and model training all require serious money. A traditional SaaS company may be able to reach meaningful traction with a lean team and cloud tools. A frontier AI company may need capital just to compete for compute capacity. In AI, the entry ticket can look less like a startup budget and more like a small national infrastructure plan.

Third, strategic buyers and corporate investors do not want to miss the platform shift. Large technology companies, cloud providers, enterprise software vendors, consulting firms, and corporate venture groups are all trying to understand where AI value will settle. That creates aggressive interest in the companies viewed as foundational to the next software cycle.

This helps explain why AI funding can rise even while the broader startup market stays cautious. AI is not being treated as a normal sector. It is being treated as a new layer of the economy.

But the AI boom is not evenly distributed

Here is the catch: “AI” is not a magic fundraising password. Investors are getting better at separating true AI leverage from AI decoration. A startup that merely connects to a third-party model and calls itself revolutionary may struggle. A startup that owns proprietary data, solves a painful workflow, reduces measurable cost, improves revenue, or controls a critical layer of infrastructure has a much stronger argument.

In the current market, AI startups generally fall into several groups:

- Infrastructure companies building chips, compute orchestration, data platforms, monitoring tools, security systems, and development frameworks.

- Foundation model companies developing large models or specialized models with significant technical and capital requirements.

- Application-layer companies using AI to improve real workflows in finance, healthcare, legal, sales, software development, customer support, manufacturing, and operations.

- AI-enabled incumbents that already have customers and are using AI to deepen product value, improve margins, or expand into adjacent markets.

The best-funded companies tend to sit in the first two groups, because infrastructure and model development can require enormous capital. But the next big opportunity may increasingly move toward the application layer, where customers care less about model architecture and more about whether the product saves time, saves money, reduces risk, or makes teams look smarter in Monday meetings.

Why deals are down outside the AI spotlight

The decline in deal count has several causes. The first is the hangover from the 2020 and 2021 funding boom. Many startups raised at valuations that assumed years of near-perfect growth. Then interest rates rose, public software multiples compressed, IPO activity slowed, and investors became allergic to “growth at all costs.” The phrase did not age well. It now sounds like something you would find on a T-shirt in a museum exhibit called Things Founders Said Before Burn Multiples Became Scary.

The second reason is liquidity. Venture capital depends on exits. When IPOs and large acquisitions slow down, venture firms return less cash to limited partners. When limited partners receive less cash, they become more cautious about committing to new venture funds. When venture funds raise less money, they deploy more carefully. The result is a slower funding cycle.

The third reason is portfolio triage. Many VCs are spending more time supporting existing companies rather than chasing every new deal. They are deciding which portfolio companies deserve follow-on capital, which need to cut costs, which should seek strategic exits, and which may not survive. That is not glamorous work, but it is part of the current venture reality.

The fourth reason is quality control. Investors today want evidence. They want revenue durability, efficient customer acquisition, strong retention, credible gross margins, and a path to profitability. The market no longer rewards “we’ll monetize later” with the same cheerful generosity. Later has arrived, and it brought a calculator.

The Bay Area is back at the center of gravity

Another important trend is geographic concentration. EY reported that the San Francisco Bay Area accounted for a major share of U.S. VC investment in Q4 2024 and nearly 70% of VC investment in Q1 2025. That does not mean every great startup must be in Silicon Valley, but it does show how AI has pulled attention back toward dense technical ecosystems.

The Bay Area benefits from a unique combination of AI talent, major labs, cloud infrastructure relationships, experienced founders, deep investor networks, and fast-moving early customers. New York, Boston, Austin, Seattle, Los Angeles, and other markets remain important, but the AI wave has strengthened the gravitational pull of the Bay Area.

For founders outside those hubs, the lesson is not “move immediately.” The lesson is to build stronger network access. In a selective market, warm introductions, category credibility, customer proof, and visible technical authority matter more than ever.

What founders should do now

Founders should not interpret today’s venture market as closed. It is open, but it has a stricter door policy. If your company is raising capital, the pitch needs to answer the questions investors are actually asking now.

Show why you deserve capital now

Investors are wary of funding companies simply because they exist in a trendy category. Explain why now is the right time, why your team is uniquely suited to win, and why the next round of capital will create a measurable step-change in value.

Prove that AI improves the business model

If AI is part of your story, show how it changes margins, workflow speed, customer outcomes, data advantage, or product defensibility. “We use AI” is not enough. So does everyone with a browser tab and curiosity.

Manage burn like the market may stay picky

Even strong companies should plan for longer fundraising cycles. Keep runway healthy. Know your must-hit milestones. Avoid hiring ahead of proof. A lean company with traction has options. A high-burn company with vague momentum has motivational posters.

Build relationships before you need money

In this environment, investors prefer to watch companies over time. Share updates, show progress, and create familiarity before launching a formal raise. Trust compounds, and unlike some startup metrics, it is not usually adjustable in a dashboard.

What investors should watch

For investors, the challenge is avoiding both fear and FOMO. Ignoring AI may be dangerous, but blindly chasing AI valuations can be just as risky. The best venture investors will likely combine technical understanding with classic business judgment.

They will ask whether the company has a real wedge, whether customers are willing to pay, whether the product improves as it scales, whether data advantages are durable, and whether gross margins can support venture outcomes. They will also ask whether the company can survive if model costs fall, open-source alternatives improve, or a large platform copies part of the product.

The AI boom is real, but it will not make every AI company a winner. Platform shifts create giants, but they also create very expensive roadkill. The difference is usually distribution, product depth, customer urgency, technical edge, and timing.

Practical experience: what this market feels like from the trenches

The experience of raising venture capital today feels different depending on where a company sits. For an AI infrastructure startup with elite technical talent, early revenue, and a clear connection to enterprise demand, the market can feel surprisingly energetic. Meetings happen quickly. Investors ask sharp questions but stay engaged. Strategic funds appear. Valuation discussions may still be ambitious. The company may even have the unusual problem of choosing between interested firms.

For a solid but non-AI SaaS company, the experience can be much more complicated. The business may have happy customers, decent retention, and a useful product, yet investors may hesitate because growth is not fast enough or the category feels crowded. These founders often hear praise without commitment. Their metrics are “interesting,” their market is “large,” and their team is “impressive,” but the term sheet remains as visible as a unicorn wearing camouflage.

For consumer startups, the journey can be even tougher unless there is breakout engagement or a powerful distribution advantage. Investors remember how expensive consumer growth can be and how quickly attention shifts. A beautiful product is not enough. The question is whether the company can acquire users efficiently, retain them naturally, and monetize without ruining the experience.

Inside board meetings, the mood has also changed. Boards are less impressed by raw growth if it comes with heavy burn. They want operating discipline. They want realistic forecasts. They want teams to know which customers are profitable, which channels work, and which experiments are just expensive confetti. This does not mean founders should stop being ambitious. It means ambition now needs a financial operating system.

Pitch meetings are more evidence-driven as well. Founders are expected to know their numbers cold: net revenue retention, gross margin, payback period, pipeline quality, churn reasons, activation rates, usage frequency, and expansion potential. In AI, they also need to explain model costs, data rights, security posture, latency, evaluation methods, and how the product avoids becoming a thin wrapper around someone else’s API.

There is also a psychological shift. During the boom, fundraising itself became a signal of success. Today, survival and execution matter more. A company that grows steadily, keeps burn under control, and solves a painful customer problem may be healthier than a company with a flashy round and no clear path to durable revenue. This is a healthier mindset, even if it feels less glamorous.

The best founders are adapting. They are not waiting for the 2021 market to return like a lost golden retriever. They are building for the market that exists now. They are narrowing their ICP, improving sales efficiency, using AI to increase internal productivity, negotiating better cloud costs, and treating every investor conversation as a chance to sharpen the business. They know the funding market is selective, but they also know selective markets reward clarity.

The practical lesson is this: venture capital has not disappeared. It has become more judgmental. That can be frustrating, but it can also be useful. Strong companies are forced to become stronger earlier. Weak stories get exposed faster. And founders who can combine vision with proof have a real chance to stand out.

Conclusion: venture is recovering, but not returning to normal

So, what is really going on in venture today? Deals are down, but big AI dollars are up. EY’s data shows a market where capital is flowing again, but not evenly. AI mega-rounds are making the venture market look healthier in dollar terms, while declining deal counts reveal continued caution underneath.

This is not a simple boom. It is a selective reallocation of capital toward companies that investors believe can define the next technology cycle. AI infrastructure, foundation models, enterprise AI, data systems, automation, and application-layer winners are attracting serious money. Meanwhile, startups outside the AI spotlight must prove efficiency, urgency, and durable customer demand.

For founders, the message is not to panic. It is to prepare. Build a company that can survive scrutiny. Show real customer value. Use AI where it strengthens the product or business model, not where it merely improves the pitch deck. For investors, the challenge is to stay disciplined while still recognizing that major platform shifts rarely wait for perfect market conditions.

The venture market is not back to easy mode. It may never be, and honestly, easy mode made everyone a little weird. But capital is available for companies that can prove they matter. In today’s VC market, the best pitch is not “we are in AI.” It is “we solve a painful problem, AI makes us meaningfully better, and the numbers prove it.” That sentence may not fit on a hoodie, but it just might get funded.

Note: This article is a synthesized editorial analysis based on public venture-capital market reports and current AI funding trends. It is written for web publication without embedded source links.