Table of Contents >> Show >> Hide

- What “boring” bonds are actually for

- The quiet secret: bond returns are often driven by the starting yield

- When boring bonds get “spicy”: the risks people forget

- Bond funds vs. individual bonds: why they feel different

- Why “bonds are supposed to be boring” is also an investing psychology lesson

- How to keep bonds boring (in a good way)

- Inflation-protected options: TIPS and I bonds

- The bottom line

- Experiences investors commonly have with “boring bonds” (and what they learn)

- Experience #1: “Wait… my bond fund is down? I thought bonds couldn’t lose.”

- Experience #2: “I chased yield, and now my ‘income’ is a stress subscription.”

- Experience #3: “I sold after rates rose… and then I missed the boring part where income rebuilds.”

- Experience #4: “I finally understood inflation when my ‘safe’ return felt smaller in real life.”

- Experience #5: “Bonds made me a better investor because they trained my patience.”

Bonds are the finance world’s beige minivan: not flashy, rarely trending, and somehow still doing

80% of the real work. When bonds are “exciting,” it usually means something weird is happening

the kind of weird that makes investors refresh their apps like they’re watching playoff overtime.

The truth is, bonds are supposed to be boring because their job is not to entertain you.

Their job is to help your portfolio survive. And if you’ve ever lived through a market drop and

realized your “high-risk tolerance” was mostly just good vibes in a bull market… you already

understand why boring can be beautiful.

What “boring” bonds are actually for

A plain-vanilla bond is basically a loan. You lend money to an issuer (like the U.S. government,

a city, or a company) and, in return, you get interest payments and your principal back at maturity

(assuming the issuer can pay). That’s it. No hype. No “to the moon.” Just math and receipts.

In a well-built plan, bonds usually play three roles:

- Stability: They tend to swing less than stocks (most of the time).

- Income: Interest payments can provide cash flow.

- Diversification: They can help cushion a portfolio when stocks struggle.

Notice what’s missing: “make you feel like a genius at parties.” Bonds don’t do that.

They’re more like the friend who brings an umbrella and snacks. Uncool, until you need them.

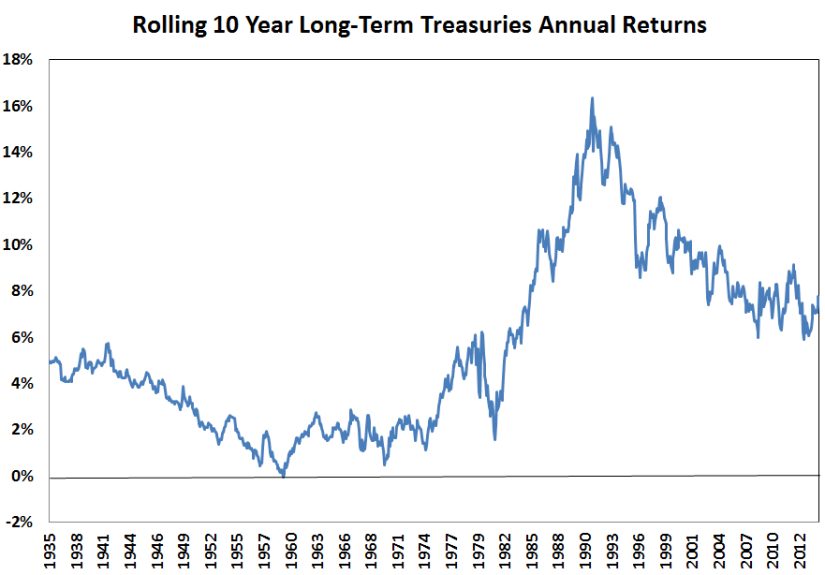

The quiet secret: bond returns are often driven by the starting yield

Stocks can surprise yougood or badbecause earnings, sentiment, and valuations can change in ways

that are hard to predict. Bonds are different. Over longer periods, bond returns are heavily influenced

by the yield you start with. In plain English: if you buy bonds when yields are higher, the math

generally gives you a better runway for future returns than when yields are near the floor.

This is one reason people say bonds are “math-y.” Over time, interest payments (“clipping coupons,”

as the old-school crowd says) do a lot of the heavy lifting. Price changes matter, but income matters too,

and the balance between the two depends on yields and time.

A simple example (with numbers you can actually picture)

Imagine you buy a 10-year bond with a face value of $1,000 and a 4% coupon rate. If you hold it to maturity

and nothing weird happens with the issuer, you’ll receive interest (typically semiannually for many Treasuries)

and you’ll get your $1,000 back at the end. The “boring” part is that the basic promise is clear from day one.

But here’s where investors get confused: between now and maturity, the bond’s market price can move around

if interest rates change. That doesn’t change the bond’s coupon payment, but it does change what someone else

would pay for your bond today.

When boring bonds get “spicy”: the risks people forget

Bonds aren’t risk-free. They’re just different-risk. If stocks are a roller coaster, bonds are a moving walkway.

Still not a great place to trip.

1) Interest-rate risk (the classic)

Bond prices and interest rates generally move in opposite directions. When new bonds are issued at higher yields,

older bonds with lower coupons become less attractiveso their prices tend to fall to compensate. When rates fall,

existing bonds with higher coupons look betterso prices tend to rise.

The key idea most people need (and most people ignore until it hurts) is duration: a measure of how

sensitive a bond (or bond fund) is to interest-rate changes. As a rough rule of thumb, if a bond fund has a duration

of 6 years, a 1% rise in yields might correspond to about a 6% decline in price (all else equal). Longer duration

usually means more sensitivitymore “spice.”

2) Inflation risk (the sneakier villain)

Inflation is the silent pickpocket of investing. It doesn’t need a dramatic headline to do damage; it just quietly

reduces what your dollars can buy. Bonds can look “safe” in nominal termsmeaning you might get your dollars back

but still disappoint after inflation is factored in.

Historically, it’s possible for bonds to have long stretches where real (after-inflation) returns are weak or even negative.

That’s not a bond failure. That’s bonds doing what bonds do: providing contractual payments, not guaranteed purchasing power.

Stocks have historically done a better job beating inflation over long horizons, but with a bumpier ride.

3) Credit risk (because not everyone is the U.S. Treasury)

U.S. Treasuries are often treated as having very low credit risk because they’re backed by the federal government.

Corporate bonds and municipal bonds can be excellent tools too, but they add the possibility that the issuer can’t pay.

That’s why credit ratings exist and why lower-rated bonds usually offer higher yields: investors demand compensation for risk.

“Higher yield” can mean “higher income”… or “higher chance of regret.” Sometimes both.

4) Reinvestment risk (the under-discussed annoyance)

Even short-term bonds have a risk people don’t talk about much: what happens when they mature (or when coupons come in)

and new yields are lower? You may have to reinvest at worse rates. This is one reason “short duration” isn’t automatically

“no risk.” It can mean “different trade-off.”

Bond funds vs. individual bonds: why they feel different

A common shock for newer investors is realizing that bond funds can lose moneyeven when they hold “safe” bonds.

The reason is simple: bond funds are priced every day, and their holdings are marked to market. If rates rise,

the market value of the fund’s bonds tends to fall, and you see it immediately in the fund price.

With an individual bond, you can also lose money if you sell before maturity during a rate spike. But many people

mentally file individual bonds under “set it and forget it” because they focus on holding to maturity and receiving

principal back. With bond funds, there is no single maturity date for the fund itself. It’s a rolling portfolio.

That makes bond funds great for diversification and convenience, but emotionally harder during rate swings.

So which is “better”?

Neither is universally better. It depends on what you’re using bonds for:

- Simple diversification + broad exposure: Funds can be efficient and easy.

- Known cash-flow timing: Individual bonds (or ladders) can feel more predictable if held to maturity.

- Behavior management: The “best” choice is the one you won’t sabotage when rates move.

Why “bonds are supposed to be boring” is also an investing psychology lesson

The phrase isn’t just about bond math. It’s about investor behavior.

When bonds behave calmly, people complain they’re “dead money.” When bonds get volatile, people panic

because bonds weren’t supposed to do that.

One useful way to think about it is time frame:

- Short term: bonds can bounce around more than you expect, especially longer-maturity bonds.

- Longer term: bond returns tend to be more tightly tied to yield and the passage of time.

The real enemy is often temptation: the urge to jump in and out based on rate predictions,

headlines, or vibes. Trying to “game” interest rates can turn a stabilizing allocation into a stress hobby.

And unlike a fun hobby (like cooking), stress hobbies don’t end with snacks.

How to keep bonds boring (in a good way)

You can’t control rates, inflation, or what the internet yells about today. You can control structure and expectations.

Here are practical ways investors often keep their bond allocation doing its job:

Match the bond type to the job

- Short-term needs: prioritize stability and liquidity; watch duration.

- Intermediate goals: balance income and interest-rate sensitivity.

- Long-term goals: understand that longer duration can swing moresometimes a lot more.

Don’t confuse “higher yield” with “free lunch”

Higher yields are often compensation for risks: credit risk, liquidity risk, or duration risk. If you reach for yield

without naming the risk you’re taking, you’re basically agreeing to mystery meat. And mystery meat is rarely premium.

Use diversification like a seatbelt, not a souvenir

Diversification doesn’t prevent bumps; it helps you survive them. A mix of bond types (and a thoughtful blend of stocks and bonds)

can reduce the chance that one specific risk dominates your life for the next two years.

Inflation-protected options: TIPS and I bonds

If inflation risk is the big fear, inflation-protected bonds can helpjust with their own quirks.

Treasury Inflation-Protected Securities (TIPS) adjust principal based on inflation measures, while Series I savings bonds

combine a fixed component and an inflation component and have specific purchase and redemption rules.

These tools can be useful in the right context, but they don’t magically erase interest-rate sensitivity or eliminate

all real-world trade-offs. Inflation protection is a feature, not a force field.

The bottom line

Bonds are supposed to be boring because they’re built to be the portfolio’s shock absorbers. They can still have rough

patchesespecially when rates move quickly or inflation flares upbut the core idea remains: bonds are often about

planning, not excitement.

If you treat bonds like a side quest for thrills, you’ll probably end up with the worst of both worlds:

less stability and more stress. If you treat them like the quiet foundation they’re meant to be,

you give the rest of your portfolio room to do what it does best.

Experiences investors commonly have with “boring bonds” (and what they learn)

Because bonds aren’t glamorous, people rarely talk about them until something feels “off.” Here are real-world

types of experiences investors commonly reportand the lessons they tend to take away.

(These aren’t personal stories from me; they’re patterns that show up again and again in how people react to bonds.)

Experience #1: “Wait… my bond fund is down? I thought bonds couldn’t lose.”

This is the classic moment of financial betrayal. An investor buys a broad bond fund for stability. Then interest rates rise,

fund prices fall, and suddenly the “safe” part of the portfolio looks like it caught the same cold going around.

The lesson is usually uncomfortable but valuable: bond funds have price risk, especially when duration is longer.

Over time, higher yields can help future returns, but the transition can feel like getting splashed by a puddle you didn’t see.

Experience #2: “I chased yield, and now my ‘income’ is a stress subscription.”

When yields on safer bonds look meh, it’s tempting to move into higher-yield corporate bonds, lower-rated debt,

or more complex bond categories. Sometimes it works fineuntil a credit cycle turns or a scary headline hits.

Investors often learn that yield is not just “extra money.” It’s often payment for taking on a risk that can show up

at the worst possible time. The best takeaway isn’t “never take risk”it’s

know which risk you’re renting and what it costs when markets get cranky.

Experience #3: “I sold after rates rose… and then I missed the boring part where income rebuilds.”

This one happens when investors react to losses by selling bonds after a rate spike. Emotionally, it feels like “stopping the bleeding.”

But selling can lock in losses right before higher yields start doing the long-run repair work: new bonds and new fund purchases

now pay more interest. Many investors later realize that the point of bonds wasn’t to never dipit was to remain functional

while the rest of the portfolio does what it does. The lesson: bonds work best when you let time do its job.

Experience #4: “I finally understood inflation when my ‘safe’ return felt smaller in real life.”

People often “get” inflation intellectually, then truly understand it when everyday costs rise and their conservative returns

don’t stretch as far. That’s when they begin to frame bond performance in real terms: not just “did I make money,” but

“did my money keep up with life?” This can lead to smarter diversification choices: combining assets with different strengths,

rather than expecting any single asset class to be perfect.

Experience #5: “Bonds made me a better investor because they trained my patience.”

Oddly enough, some investors end up appreciating bonds because bonds force a mindset shift. Stocks reward excitement and narrative;

bonds reward consistency and acceptance of trade-offs. People who stick with a sensible bond allocation often say the same thing later:

bonds didn’t make them rich, but bonds made it easier to stay invested in everything else. That’s a huge win.

A portfolio that you can actually hold through ugly markets is often more valuable than a portfolio that looks perfect on paper.

If bonds feel boring, that’s not a design flaw. That’s the design working.

The best compliment you can give your bond allocation is: “I barely noticed it.”