Table of Contents >> Show >> Hide

- What Gartner’s “40% Growth” Really Means (and Why It’s Plausible)

- Why SaaS Spending Keeps Climbing

- 1) SaaS is still the easiest “yes” in a world that hates big upfront commitments

- 2) The app stack keeps getting taller

- 3) Security, compliance, and resilience are spending multipliers

- 4) AI is making SaaS both more valuable and more expensive

- 5) Cloud marketplaces and composable apps speed up adoption

- Where the Money Is Going: SaaS Is the Anchor, But Platforms Are the Engine

- The Two-Sided Reality: Growth Meets Governance

- A Practical Playbook for the Next Two Years

- Three Scenarios for SaaS Spend Through 2027

- Conclusion: The Forecast Is a Tailwind, Not Autopilot

- Field Notes: of Real-World Experiences From the SaaS Spend Surge

If “software is eating the world,” SaaS is the part that keeps ordering seconds… and dessert… and then signing up for the loyalty program.

Gartner’s forecast that SaaS spending can jump roughly another 40% over a short window is the kind of headline that makes investors nod,

CFOs squint at renewal calendars, and IT leaders quietly whisper, “Please tell me we didn’t buy three project-management tools again.”

But this story isn’t just “SaaS good, number go up.” The more interesting question is why SaaS spending keeps climbing,

where that money is going, and what smart organizations do to turn bigger budgets into better outcomeswithout

accidentally funding an entire shadow economy of unused licenses.

What Gartner’s “40% Growth” Really Means (and Why It’s Plausible)

The math behind the headline

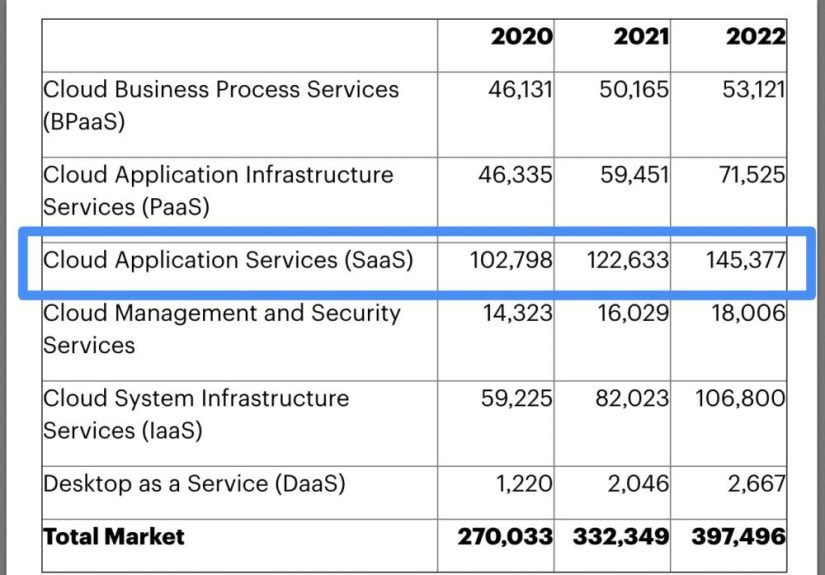

Gartner’s public-cloud forecasts show how quickly SaaS can scale in just a couple of years.

One example: Gartner projected worldwide end-user SaaS spending rising from about $102.8B (2020)

to $145.4B (2022)a gain of roughly 41% in two years. That’s the “another ~40%” idea in numeric form:

not a vague vibe, but a real acceleration over a tight timeframe.

Later Gartner updates kept the same themefast growth, just on bigger base numbers. In Gartner’s more recent cloud spending outlooks,

worldwide SaaS spend is projected to approach $300B by 2025, following a 2024 level a bit above $250B.

The exact figures shift as Gartner refreshes assumptions, but the direction stays consistent: SaaS is still the biggest slice of cloud spending,

and it’s still growing at a pace most “mature” categories would envy.

Forecasts change because the market changes (and definitions evolve)

If you’ve ever tried to predict how many cups of coffee you’ll drink next week, you already understand forecasting humility.

Gartner’s numbers can move across updates because vendor pricing changes, adoption speeds up or slows down, currency and macro conditions shift,

and market definitions get refined. The useful takeaway isn’t to obsess over the third decimal placeit’s to recognize the

compounding effect: double-digit SaaS growth, year after year, quickly becomes “another 40%.”

Why SaaS Spending Keeps Climbing

1) SaaS is still the easiest “yes” in a world that hates big upfront commitments

Subscriptions don’t feel like a capital project. They feel like a utility billuntil you realize you’ve been paying for “utilities”

in 47 different places. SaaS lets teams deploy fast, iterate quickly, and scale usage without waiting for long procurement cycles or

on-prem buildouts. That speed is addictive, especially when competitors are shipping features weekly.

2) The app stack keeps getting taller

SaaS isn’t a single purchase; it’s an ecosystem. Collaboration tools, CRM, customer support, data compliance, identity, analytics,

marketing automation, HR systems, and industry-specific platforms pile up.

Okta’s Businesses at Work reporting shows the “average number of apps” per customer topping 100a milestone that underscores

how many SaaS tools the typical organization touches. More apps usually means more subscriptions, and more subscriptions means… well, you know.

3) Security, compliance, and resilience are spending multipliers

Every new SaaS app expands the attack surface and adds data governance responsibilities. That drives spending in adjacent categories:

identity and access management, monitoring, backup, and compliance tooling. Gartner has even projected that SaaS backup becomes a much more

common “must-have” requirement over the next few yearsbecause the data inside SaaS apps is now core enterprise data, not disposable fluff.

4) AI is making SaaS both more valuable and more expensive

GenAI is sliding into product roadmaps like it owns the placeand it’s not doing it for free. Gartner has pointed out that GenAI features

are becoming ubiquitous across enterprise software and that these features cost more money. In plain English:

“Congrats on your new productivity boost. Here’s your updated invoice.”

5) Cloud marketplaces and composable apps speed up adoption

Gartner has discussed how enterprises increasingly buy and deploy SaaS through cloud marketplaces, and how teams break monolithic apps into

more composable parts to move faster with DevOps. Both trends reduce frictionfewer obstacles between “we need this tool” and “it’s live by Friday.”

Reduced friction often equals increased spending.

Where the Money Is Going: SaaS Is the Anchor, But Platforms Are the Engine

SaaS remains the biggest segment

In multiple Gartner public-cloud forecasts, SaaS sits at the top by end-user spending.

Recent outlooks put global SaaS spending near $250B in 2024 and nearing $300B in 2025still huge,

still growing, still the category that finance teams notice first because it shows up as recurring operating expense.

Infrastructure and platform services are growing fastthanks in part to AI

SaaS doesn’t run on hope. It runs on cloud infrastructure, data platforms, and increasingly expensive compute.

Gartner has highlighted strong growth in infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS) alongside SaaS,

with AI workloads amplifying demand for cloud capacity.

Gartner also reported the worldwide IaaS market growing sharply in 2024, driven by demand for AI infrastructure and ongoing migration/modernization.

Why does that matter for a SaaS spending forecast? Because when infrastructure gets pricier, SaaS providers feel it too.

Some of that cost pressure gets absorbed, some gets optimized away, and some gets passed along through price increases,

higher-tier packaging, or “AI add-on” SKUs. The buyer experiences it as: “Same tool, new price, now with an AI button.”

The Two-Sided Reality: Growth Meets Governance

More spend doesn’t mean “spend however you want”

Organizations are spending more on SaaS, but they’re also getting pickier.

Flexera’s State of the Cloud reporting has repeatedly flagged cloud spending management as a top challenge,

and it notes that a meaningful share of organizations report very high annual spend levels (including SaaS).

Translation: budgets are large, but patience is not infinite.

FinOps is showing up to the SaaS party

FinOps began as “cloud cost management,” but the mindset spreads naturally to SaaS: measure usage, tie spend to value,

and create shared accountability between engineering/IT, finance, and business owners.

The FinOps Foundation describes FinOps as an operational framework and cultural practice to maximize business value and enable

data-driven decision-making with financial accountability. That’s exactly what SaaS leaders need when renewals pile up.

Consolidation is the new cardio

When spending rises, rationalization follows. Many companies are consolidating vendorsreducing overlap,

standardizing on fewer platforms, and negotiating harder. The motivation isn’t only cost; it’s also security, support, and simplicity.

Fewer tools can mean fewer integrations to maintain and fewer places for data to leak.

A Practical Playbook for the Next Two Years

If you’re buying SaaS: how to grow spend without wasting it

- Build a real SaaS inventory. Not “a spreadsheet we update during panic week.” A living catalog with owners, renewals, and usage data.

- Stop paying for shelfware. Track seats used vs. seats purchased, and re-harvest licenses quarterly, not annually.

- Design for consolidation (before you need it). Standardize on core platforms for comms, identity, ticketing, and analytics where possible.

- Attach security and resilience requirements to procurement. Include backup, access controls, audit logs, and data retention up front.

- Make renewals earn their keep. Every renewal should answer: “What outcome did we get, and how do we measure it next year?”

If you’re selling SaaS: how to ride the wave without wiping out

- Prove ROI in the customer’s language. Time saved, revenue protected, risk reducedtied to metrics the buyer already reports.

- Package AI carefully. If AI raises prices, it must also raise outcomes. Ship “wow” moments, not “meh” feature lists.

- Invest in trust: security, compliance, resilience. Buyers are maturing; “security later” is no longer a charming startup personality trait.

- Expect procurement to be sharper. Build negotiation playbooks, multi-year discount structures, and clear value tiers.

- Win the consolidation conversation. Position as the platform that replaces two or three tools, not the 18th tab in someone’s browser.

Three Scenarios for SaaS Spend Through 2027

Base case: steady growth with periodic “optimization winters”

SaaS spending grows, but buyers run regular cleanup cycles. Seat-count trimming and vendor consolidation happen every year,

while truly strategic SaaS categories keep expanding (security, data, core collaboration, industry platforms).

Bull case: AI-driven app expansion accelerates budget “flush” cycles

More workloads shift to cloud platforms, AI features become standard across software portfolios, and organizations invest aggressively

in productivity and modernization. Budgets rise faster than plannedbecause the business demands outcomes now, not in next year’s roadmap.

Bear case: growth continues, but the bar for renewals rises sharply

If macro uncertainty spikes, SaaS still grows, but the easy renewals disappear. Customers demand proof, consolidate aggressively,

and move spend toward platforms that reduce tool sprawl. Weak vendors feel churn; strong vendors capture share.

Conclusion: The Forecast Is a Tailwind, Not Autopilot

Gartner’s view that SaaS spending can grow roughly another 40% over a short two-year stretch is believable because the drivers are structural:

app proliferation, cloud-first architecture, AI-enabled software, and the ongoing shift from monoliths to modular systems.

But the “growth story” now comes with a “governance story.” SaaS budgets may expand, yet scrutiny is expanding too.

The winnersbuyers and vendors alikewill be the ones who treat SaaS spending as a portfolio:

invest where value compounds, cut where value evaporates, and build the operational muscle to manage subscriptions continuously.

In other words: grow smart, not just big.

Field Notes: of Real-World Experiences From the SaaS Spend Surge

When SaaS spending accelerates, the first thing that changes is the tone of conversations inside organizations.

Early on, teams talk about features: “Does it integrate?” “Is the UI clean?” “Can we go live this sprint?” Then the renewal calendar fills up,

and the questions become sharper: “Who owns this tool?” “What departments actually use it?” “Why do we have 600 licenses and 190 weekly active users?”

That shiftfrom excitement to accountabilityisn’t a sign SaaS is failing. It’s a sign SaaS has become important enough to manage like a real asset.

A common pattern is the “three-tools-for-one-job” moment. Marketing might have one analytics platform, product has another,

and leadership is staring at dashboards that disagree. The spending isn’t the only issuethe confusion is. In many companies, consolidation starts

not because finance demands it, but because teams want a single source of truth. When SaaS grows quickly, the hidden cost is often fragmentation:

duplicated workflows, duplicated data, duplicated vendor meetings (which is a special kind of pain).

Another recurring experience is what some teams call “AI invoice surprise.” A vendor adds a helpful AI assistant, bundles it into

higher tiers, or introduces usage-based pricing. The feature might be legitimately valuable, but buyers get caught off guard if value measurement

isn’t already in place. The organizations that handle this best tend to do two things: they pilot AI features with a defined success metric

(time-to-resolution, content throughput, lead-to-meeting conversion, fewer support escalations), and they decide up front whether the feature is

a must-have or a nice-to-have. That prevents the classic scenario where you pay premium prices for AI that nobody adopts after the novelty wears off.

On the operational side, the most successful teams treat SaaS management like hygieneboring, regular, unavoidable, and wildly beneficial.

They run quarterly access reviews, maintain a clean app catalog, and bake “license harvesting” into offboarding and role changes.

They also get serious about ownership: every major tool has a business owner responsible for adoption and outcomes, not just an admin responsible for

configurations. That one shiftassigning outcome ownershipoften turns SaaS from a cost center into a measurable productivity engine.

Finally, as stacks expand, resilience becomes personal. Outages and misconfigurations are no longer abstract IT risks; they interrupt payroll,

block customer support, pause sales pipelines, and delay shipments. That’s why practices like SaaS backup, stronger identity controls, and vendor risk reviews

show up more often in mature organizations. The “experience” of rapid SaaS growth is ultimately this: SaaS becomes the business, so it has to be run like one.