Table of Contents >> Show >> Hide

- Introduction: Deferred Compensation Is Not “Future You’s Problem”

- What Is Deferred Compensation?

- How to Account for Deferred Compensation: 7 Steps

- Step 1: Identify the Deferred Compensation Arrangement

- Step 2: Determine Whether the Employee Has Earned the Compensation

- Step 3: Measure the Deferred Compensation Liability

- Step 4: Record the Initial Journal Entry

- Step 5: Account for Rabbi Trusts and Plan Assets Correctly

- Step 6: Handle Payroll Taxes, Income Taxes, and Employer Deductions

- Step 7: Revalue, Disclose, and Settle the Obligation

- Common Mistakes When Accounting for Deferred Compensation

- Practical Example: A Full Deferred Compensation Accounting Walkthrough

- Internal Controls for Deferred Compensation

- Experience-Based Insights: What Real Teams Learn When Accounting for Deferred Compensation

- Conclusion

Note: This article is written for educational publishing purposes and summarizes widely used U.S. accounting and tax concepts related to deferred compensation, including GAAP treatment, nonqualified deferred compensation plans, rabbi trusts, payroll taxes, and practical journal-entry examples.

Introduction: Deferred Compensation Is Not “Future You’s Problem”

Deferred compensation sounds like one of those accounting topics designed to make normal people suddenly remember they left the oven on. But at its core, it is simple: an employee earns compensation now, while the employer pays it later. The tricky part is making sure the company records the obligation at the right time, measures it properly, updates it consistently, and does not pretend the liability wandered off into the woods wearing a disguise.

In business, deferred compensation can appear in many forms: executive bonus deferrals, supplemental retirement arrangements, salary deferral plans, incentive compensation payable after vesting, phantom stock plans, and nonqualified deferred compensation plans. For employers, accounting for deferred compensation is not just a bookkeeping task. It affects the balance sheet, income statement, payroll tax reporting, tax deductions, internal controls, cash-flow planning, and sometimes employee trust.

This guide explains how to account for deferred compensation in 7 steps, using plain English, practical examples, and a few well-placed accounting seat belts. Whether you are a business owner, controller, HR leader, startup founder, or finance student trying to survive the phrase “present value of future obligation,” this article will help you understand the process without needing a three-day retreat and a gallon of coffee.

What Is Deferred Compensation?

Deferred compensation is compensation earned by an employee in one period but paid in a later period. Instead of paying the full amount immediately, the employer promises payment at a future date, often after retirement, separation from service, vesting, or another plan-defined event.

There are two broad categories:

Qualified Deferred Compensation

Qualified plans, such as 401(k) plans, follow specific retirement-plan rules and are generally covered by federal retirement-benefit regulations. These plans usually have contribution limits, nondiscrimination requirements, and separate plan assets.

Nonqualified Deferred Compensation

Nonqualified deferred compensation, often called NQDC, is usually designed for executives, highly compensated employees, or selected key employees. These arrangements are more flexible than qualified plans, but they come with strict tax rules, especially under Internal Revenue Code Section 409A. In many cases, the employer keeps the obligation on its books, and the employee becomes an unsecured creditor until payment is made. In other words, the employee has a promise, not a locked treasure chest guarded by dragons.

How to Account for Deferred Compensation: 7 Steps

Step 1: Identify the Deferred Compensation Arrangement

The first step is to understand exactly what kind of deferred compensation arrangement exists. Do not start with journal entries. Start with the agreement. Accounting without reading the contract is like assembling furniture by staring confidently at the screws.

Review the plan document, employment agreement, board approval, bonus letter, or compensation policy. Determine what the employee is entitled to receive, when the payment will be made, whether the amount is fixed or variable, and what conditions must be satisfied before payment occurs.

Important questions include:

- Is the compensation already earned, or must the employee provide future service?

- Is the amount fixed, indexed, or based on investment returns?

- Does the employee need to vest before becoming eligible?

- Is payment triggered by retirement, separation, death, disability, change in control, or a fixed date?

- Is the arrangement funded, unfunded, or supported by a rabbi trust?

For example, suppose a company promises an executive a $100,000 bonus payable three years from now if the executive remains employed through the vesting date. That is different from a $100,000 bonus already earned this year but voluntarily deferred until retirement. The first arrangement may require expense recognition over the service period. The second may create a liability once the compensation is earned and deferred.

Step 2: Determine Whether the Employee Has Earned the Compensation

The heart of deferred compensation accounting is matching. Under accrual accounting, companies recognize compensation cost when employees provide the related service, not necessarily when cash leaves the bank account. The payroll department may care about payday Friday; the accounting department cares about when the obligation was created.

If an employee has already performed the required services and the company has a present obligation, the employer generally records compensation expense and a liability. If the employee must continue working to earn the benefit, the company typically recognizes the expense over the required service period.

Consider this simple example:

A company grants a manager a $60,000 deferred retention bonus. The manager must work for three years to receive it. The company may recognize $20,000 of compensation expense each year, assuming straight-line recognition is appropriate and no other measurement adjustments are required.

The same entry would be recorded in Year 2 and Year 3, adjusted if facts change. By the end of Year 3, the company has recognized the full $60,000 liability. When the payment is made, the liability is reduced.

This approach keeps the income statement honest. The company does not wait until the payment date to suddenly recognize three years of expense like an accounting jump scare.

Step 3: Measure the Deferred Compensation Liability

After identifying the obligation, the next step is measurement. Some deferred compensation liabilities are easy to measure because they are fixed. Others require more judgment because the final payment may depend on investment returns, company stock value, interest credits, performance metrics, or other variables.

If the promise is a fixed cash amount, the liability may be measured based on the amount earned to date. If the payment will occur far in the future, present value may be relevant, especially when the timing and amount are reasonably estimable. If the plan credits notional investment returns, the liability may change as those returns change.

Example:

An executive defers a $50,000 bonus. The plan credits the deferred amount with a notional return based on a market index. At year-end, the account balance has increased to $54,000. The employer should update the liability to reflect the plan terms. The additional $4,000 is generally recognized as additional compensation cost or another appropriate expense classification based on the company’s accounting policy and the nature of the plan.

The key is consistency. The company should measure the obligation based on the formula in the plan document and apply that method every reporting period.

Step 4: Record the Initial Journal Entry

Once the company determines that compensation has been earned and measures the obligation, it records the initial entry. The basic entry is straightforward:

This entry recognizes that the employee has earned compensation and the employer now owes it, even though cash payment will happen later.

For example, assume a company owes an executive $80,000 of deferred compensation earned during the current year. Payment will be made five years later.

This liability appears on the balance sheet. Depending on the expected payment date, part or all of it may be classified as noncurrent. If payment is due within one year, the relevant portion may be classified as current.

Classification matters because lenders, investors, and management use current and noncurrent liabilities to evaluate liquidity. A deferred compensation liability due next quarter is not the same as one due after the CEO retires in 2038, buys a boat, and names it “Accrual Basis.”

Step 5: Account for Rabbi Trusts and Plan Assets Correctly

Some employers use a rabbi trust to informally fund nonqualified deferred compensation obligations. A rabbi trust is designed to hold assets that may be used to pay deferred compensation benefits. However, the assets generally remain subject to the claims of the employer’s creditors if the company becomes insolvent.

This point is extremely important. A rabbi trust may make employees feel more comfortable, but it usually does not remove the employer’s liability. The employer still records the deferred compensation obligation. The trust assets are also generally recorded on the employer’s balance sheet because they are not protected from creditors in the same way qualified retirement plan assets may be.

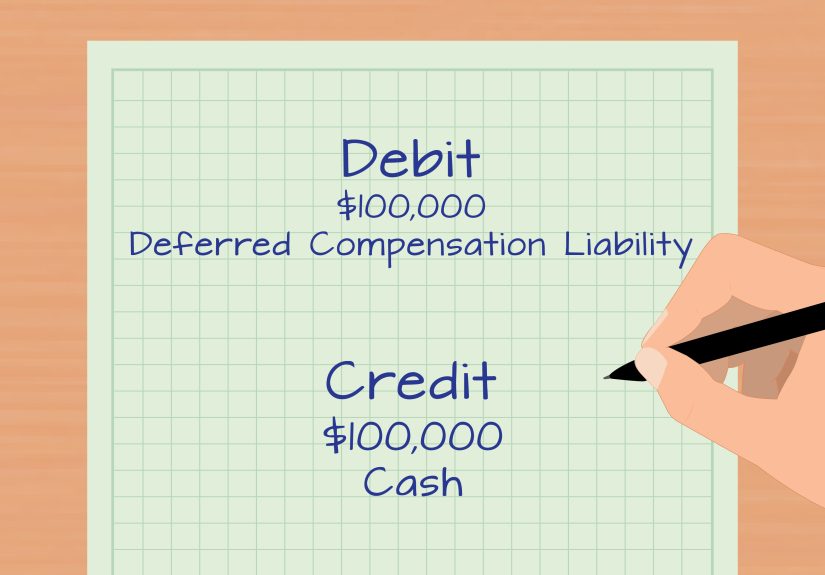

For example, assume a company contributes $100,000 to a rabbi trust to help pay a deferred compensation obligation.

The company does not debit the deferred compensation liability simply because it placed money into the trust. The liability remains until the employee is paid or the obligation is otherwise settled.

If the trust assets change in value, the employer accounts for those investment changes under the applicable accounting rules for the asset type. Meanwhile, the deferred compensation liability is adjusted based on the plan obligation. The asset and liability may move in similar directions, but they are not automatically the same thing. Think of them as two people walking near each other at the mall, not identical twins wearing matching sweaters.

Step 6: Handle Payroll Taxes, Income Taxes, and Employer Deductions

Deferred compensation accounting is not only a GAAP issue. Tax rules matter, too. For nonqualified deferred compensation, Internal Revenue Code Section 409A is especially important. It generally requires careful rules around deferral elections, payment timing, and permissible distribution events.

From the employer’s perspective, tax accounting can differ from book accounting. For financial reporting, compensation expense may be recognized when the employee earns the benefit. For income tax purposes, the employer’s deduction is often delayed until the employee includes the compensation in taxable income. This creates a temporary difference that may require deferred tax accounting.

Example:

A company records $100,000 of book compensation expense in Year 1 for deferred compensation. The employee will not receive or recognize the income until Year 5. If the employer cannot deduct the amount for tax purposes until Year 5, the company may record a deferred tax asset, assuming realization is more likely than not.

This example assumes a 21% corporate tax rate. Actual tax accounting depends on the company’s facts, tax position, and valuation allowance assessment.

Employment taxes also require attention. For many nonqualified deferred compensation arrangements, FICA taxes may apply when the compensation is earned or when it vests, even if payment occurs later. That creates a timing mismatch: the employee may not receive cash until the future, but payroll tax may be due earlier. If that sounds rude, welcome to payroll compliance.

Companies should coordinate accounting, payroll, tax, HR, and legal teams so the plan is administered correctly. A beautiful journal entry cannot rescue a plan that violates tax rules.

Step 7: Revalue, Disclose, and Settle the Obligation

Deferred compensation accounting does not end after the first entry. Companies must review the liability each reporting period. If the obligation changes because of additional service, investment credits, interest, forfeitures, changes in assumptions, or plan amendments, the accounting records should be updated.

Common period-end procedures include:

- Recalculating employee account balances

- Reviewing vesting status

- Updating current and noncurrent classification

- Reconciling payroll records to the general ledger

- Comparing plan obligations with rabbi trust assets

- Evaluating deferred tax assets or liabilities

- Preparing management reports and financial statement support

When the company finally pays the deferred compensation, it reduces the liability and records the cash payment. If payroll withholding applies, the entry should reflect taxes withheld and remitted.

This simplified example assumes $35,000 is withheld for taxes. In real life, payroll tax and withholding calculations should be handled carefully based on federal, state, and local rules.

Common Mistakes When Accounting for Deferred Compensation

Mistake 1: Waiting Until Cash Is Paid

The most common mistake is recognizing expense only when payment occurs. Under accrual accounting, expense recognition usually follows employee service and obligation creation, not cash payment.

Mistake 2: Ignoring Vesting Conditions

If the employee must provide future service, the company should usually recognize the expense over the service period. Recording the full liability too early may overstate expenses and liabilities.

Mistake 3: Treating Rabbi Trust Assets as Settlement

Funding a rabbi trust does not usually eliminate the liability. The company still owes the employee, and the assets may remain available to creditors.

Mistake 4: Forgetting Tax Timing Differences

Book expense and tax deductions may occur in different years. This can create deferred tax assets and requires coordination with the tax provision process.

Mistake 5: Poor Documentation

Deferred compensation plans should be supported by written agreements, board approvals, employee elections, vesting schedules, and calculation workpapers. If the documentation is messy, the accounting will eventually start wearing a fake mustache and causing trouble.

Practical Example: A Full Deferred Compensation Accounting Walkthrough

Assume BrightTrail Software grants its chief operating officer a $120,000 deferred compensation award. The executive must remain employed for four years. Once vested, the amount will be paid two years later. The award does not earn interest or investment credits.

BrightTrail determines that the compensation should be recognized over the four-year service period. Each year, the company records:

After four years, the liability equals $120,000. During the two-year waiting period before payment, no additional compensation cost is recorded because the amount does not earn interest or investment credits. If the company determines present value accounting is required, it may recognize accretion over time, depending on the facts and accounting policy.

When BrightTrail pays the executive, it records the settlement entry, including tax withholding:

This example is intentionally simple, but it shows the basic rhythm: identify the arrangement, recognize expense as earned, record the liability, update the balance, and settle it when paid.

Internal Controls for Deferred Compensation

Strong controls are essential because deferred compensation often involves senior executives, complex tax rules, long payment timelines, and large dollar amounts. A company should not manage deferred compensation with a lonely spreadsheet named “Final_v7_REALLY_FINAL.xlsx.”

Useful controls include:

- Legal review of plan documents before approval

- Board or compensation committee approval for executive plans

- Formal tracking of employee deferral elections

- Quarterly reconciliation of plan balances to the general ledger

- Independent review of vesting and payment triggers

- Tax review for Section 409A and payroll compliance

- Clear segregation of duties between HR, payroll, accounting, and treasury

These controls reduce the risk of incorrect expense recognition, late payroll tax deposits, improper payments, and financial statement misclassification.

Experience-Based Insights: What Real Teams Learn When Accounting for Deferred Compensation

In practice, accounting for deferred compensation is rarely difficult because of the debit and credit. The hard part is gathering the right information from the right people at the right time. The accounting team may know the general ledger, but HR often owns the employee agreement. Legal may understand the plan language, but payroll controls tax withholding. Treasury may manage rabbi trust funding, while executives remember the original business purpose. Deferred compensation sits in the middle of all these departments like a conference-room spider plant: everyone sees it, but nobody is completely sure who waters it.

One common real-world experience is discovering that the plan document says one thing, while the spreadsheet says another. For instance, a bonus agreement may state that an executive vests after three years, but the internal tracking file may start expense recognition immediately without considering forfeiture risk or service requirements. This is why finance teams should read the actual agreement before building the accounting model. A five-minute document review can prevent five months of cleanup later.

Another lesson is that deferred compensation plans need calendar discipline. Payment dates, deferral elections, vesting dates, and tax deadlines should be tracked carefully. Missing a date can create compliance issues, employee frustration, and awkward meetings where everyone uses the phrase “process improvement” while silently panicking. A shared compliance calendar, reviewed quarterly, is one of the simplest tools a company can use.

Companies also learn that rabbi trusts can create confusion. Executives may believe the trust fully protects their benefit, while accounting may assume the trust assets offset the liability. Neither assumption should be made casually. The trust arrangement must be reviewed carefully. In many cases, the employer still records both the asset and the deferred compensation liability, and the employee remains exposed to employer credit risk. Clear communication helps avoid misunderstandings.

From an audit perspective, deferred compensation balances require strong support. Auditors often ask for plan documents, participant-level rollforwards, vesting schedules, reconciliation to payroll records, fair value support for trust assets, and evidence of management review. The best accounting teams prepare these schedules before year-end. The less prepared teams spend January digging through email threads with subject lines like “Quick question from 2021.”

A practical best practice is to create a deferred compensation memo for each major plan. The memo should summarize the plan terms, accounting conclusion, expense recognition method, liability measurement, tax considerations, journal-entry approach, and disclosure considerations. This memo does not need to be dramatic. It just needs to be clear enough that someone new can understand the logic two years later without summoning the former controller from LinkedIn.

The biggest lesson is simple: deferred compensation accounting rewards consistency. Once a company establishes the correct method, it should apply that method every period, update assumptions when facts change, and document the review. Good accounting is not about making the plan look better. It is about making the financial statements reflect the economic reality: employees earned compensation, the company owes payment, and that promise belongs in the books.

Conclusion

Accounting for deferred compensation does not have to feel like decoding ancient runes in a windowless conference room. The process becomes manageable when broken into seven steps: identify the arrangement, determine when compensation is earned, measure the liability, record the initial entry, account for rabbi trusts properly, handle tax timing, and revalue or settle the obligation each period.

The most important principle is accrual accounting. If employees have earned compensation and the company has an obligation, the company should generally recognize the expense and liability even if payment happens later. Deferred compensation may delay cash payment, but it does not delay financial responsibility.

For businesses, clean deferred compensation accounting supports accurate financial statements, smoother audits, better tax coordination, and stronger employee trust. For accountants, it is another reminder that the balance sheet has a long memory. Promises made today often become liabilities tomorrow, and the best time to account for them correctly is before they start sending calendar invites.