Table of Contents >> Show >> Hide

- Why stolen inventory is an accounting issue, not just a security issue

- Step 1: Confirm that the shortage is real

- Step 2: Separate theft from general shrinkage

- Step 3: Value the missing inventory at cost

- Step 4: Decide whether the loss is immaterial or material

- Step 5: Record the journal entry

- Step 6: Handle insurance claims and tax treatment carefully

- Step 7: Update your records and keep a strong support file

- Step 8: Fix the control problem that allowed the loss

- Common mistakes to avoid

- Real-world experiences businesses often have with stolen inventory

- Final thoughts

- SEO Tags

Inventory has an annoying habit of disappearing at the worst possible moment. Sometimes it is true theft. Sometimes it is damage, a receiving error, bad labeling, a ghost SKU, or a spreadsheet that has been living a double life. Either way, when the count in your system does not match what is physically on the shelf, your accounting has to catch up.

If you want your financial statements to stay honest and your tax return to stay out of the danger zone, you need a clean process for stolen inventory. That means confirming the shortage, valuing the missing goods correctly, posting the right journal entry, documenting the loss, and tightening controls so the same problem does not keep replaying like a bad rerun.

This guide breaks the process into eight practical steps. It is written for business owners, bookkeepers, controllers, and anyone else who has ever stared at an empty shelf and thought, “That item definitely did not invoice itself into thin air.”

Why stolen inventory is an accounting issue, not just a security issue

When inventory is stolen, your books still show an asset that no longer exists. That overstates inventory on the balance sheet and can understate expense on the income statement. In plain English, your numbers start flattering you in all the wrong ways.

That is why stolen inventory usually gets recorded as an inventory shrinkage adjustment or a write-off at cost. The key phrase there is at cost. You are not recording the missing goods at the retail selling price or at what you wish they had sold for on a wonderful holiday weekend. You are removing the asset based on the cost method your business already uses.

For tax purposes, things can be a little more nuanced, especially if insurance reimbursement is involved. So while the steps below are practical and grounded in real accounting treatment, businesses with audited financials, multiple locations, or large losses should loop in a CPA.

Step 1: Confirm that the shortage is real

Before you record stolen inventory, make sure you are not booking a loss for inventory that is actually sitting in the wrong bin, assigned to the wrong SKU, or counted in the wrong unit of measure. A missing case of product can mysteriously reappear when someone realizes the system was tracking units by case while the warehouse counted individual pieces. Accounting loves surprises about as much as cats love bath time.

What to do first

Recount the items. Then check product descriptions, item codes, locations, packaging, and units of measure. Review recent sales, returns, transfers, and receiving activity. If you use perpetual inventory, compare the system trail to the physical count. If you use periodic inventory, make sure the full count was performed consistently.

This step matters because not all inventory discrepancies are theft. Some are administrative errors, vendor issues, damage, spoilage, or timing problems between the floor and the ledger. If you skip this verification step, you can end up writing off the wrong amount and solving the wrong problem.

Step 2: Separate theft from general shrinkage

Once you confirm the shortage, decide whether you are dealing with a specific theft event or general inventory shrinkage. That distinction matters for documentation, internal reporting, insurance claims, and sometimes tax handling.

A specific theft event might involve a break-in, a known employee scheme, or a clearly documented loss from a specific location and date. General shrinkage is broader. It often includes theft, but also counting errors, vendor fraud, returns abuse, unrecorded damage, and administrative mistakes. In many businesses, the accounting entry looks similar either way, but the support file should not.

Build an incident file

Create a file that includes the date discovered, SKUs affected, quantity missing, unit cost, location, the staff member who identified the shortage, count sheets, system reports, camera footage if available, and any police report or internal investigation memo. If the loss may be insured, start gathering proof immediately. If you wait until three weeks later, the story gets fuzzy and the paper trail gets theatrical.

Step 3: Value the missing inventory at cost

This is where many businesses get tripped up. The missing inventory should generally be valued using the same cost basis your company uses for inventory accounting. That could be FIFO, LIFO, weighted average, or specific identification, depending on your system and accounting method.

Do not record the loss at the retail sales value. Retail price may be useful for operational analysis or an insurance discussion, but the book entry that removes inventory should usually reflect the item’s carrying amount in your records.

Example

Suppose you discover that 40 wireless speakers are gone. The retail price is $125 each, but your weighted average cost is $68 per unit. Your accounting loss is based on the $68 cost, not the $125 sales price.

If you suspect the goods still have some recoverable value, that is usually a write-down conversation, not a stolen inventory conversation. Stolen goods are gone. Gone inventory does not get a second act on the balance sheet.

Step 4: Decide whether the loss is immaterial or material

Now decide how the loss should be presented. Small, routine shrinkage is often recorded through cost of goods sold or a shrinkage expense account. Larger or unusual losses may deserve a separate line item such as Loss on Stolen Inventory so management can see the hit clearly and gross margin does not get distorted.

This is partly an accounting policy issue and partly a judgment call. A $600 loss in a busy retail operation may be noise. A $60,000 loss in a small distributor is absolutely not noise. That is a siren, a flashlight, and probably an emergency meeting.

Rule of thumb

If the loss is recurring and ordinary, many businesses run it through operating expense or COGS. If it is large, unusual, or tied to a one-time event, separate presentation usually gives management better visibility.

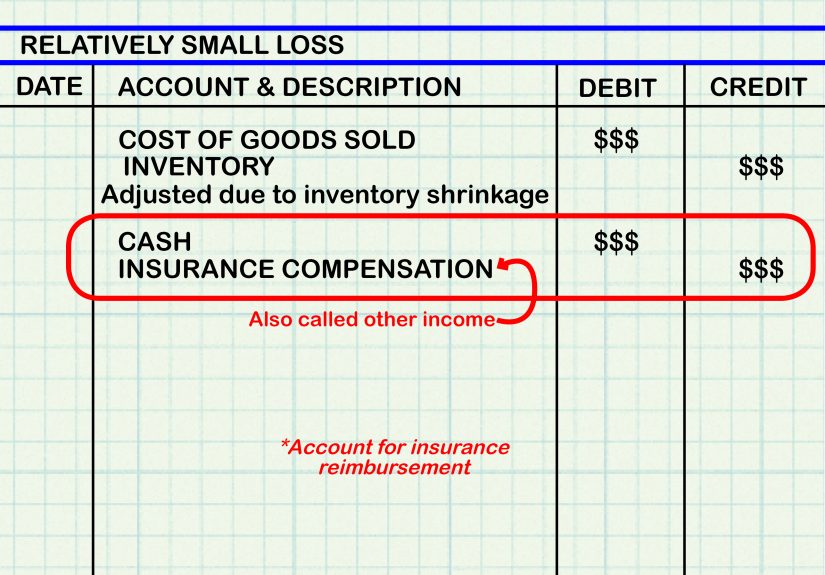

Step 5: Record the journal entry

Once you know the amount and presentation, it is time to post the entry. The basic idea is simple: remove the missing inventory asset and record the loss.

Common journal entry for a routine loss

Common journal entry for a material theft loss

Some larger businesses also use an allowance or reserve approach for normal expected shrinkage during the period, then true it up after counts. In that setup, estimated losses are accrued first, and actual write-offs later reduce the allowance. That can be useful for retailers or operators with predictable recurring shrinkage patterns. Small businesses, however, often keep things simpler and record the write-off when the shortage is confirmed.

Whichever method you use, consistency matters. Do not post one loss to COGS, another to office supplies, and a third to “miscellaneous adjustments” because the chart of accounts started feeling creative that day.

Step 6: Handle insurance claims and tax treatment carefully

This is the part where stolen inventory stops being merely annoying and starts getting technical.

If you expect insurance reimbursement, track it separately from the inventory write-off. The missing inventory still needs to come off the books. Any claim recovery should be documented and recorded under your normal accounting policy for reimbursements and receivables. Do not leave the inventory asset sitting there just because you hope the insurer will make you whole later.

For federal tax purposes, the IRS allows business inventory theft losses to be handled in one of two ways. One approach is through cost of goods sold by properly reporting opening and closing inventory. The other is as a separate deduction. The catch is that you cannot deduct the same loss twice. If you deduct it separately, the affected inventory must be removed from COGS by adjusting opening inventory or purchases. Reimbursements also affect the tax treatment, so the mechanics change depending on which route you take.

Translation: do not freestyle this part. If the loss is meaningful, talk to your tax preparer before filing. Tax rules are not the place for vibes.

Step 7: Update your records and keep a strong support file

Accounting entries without backup are how ordinary problems turn into ugly audit questions. Your file should be strong enough that an owner, auditor, insurer, or tax preparer can understand what happened without needing a dramatic reenactment.

Your support file should include

- Physical count sheets and recount results

- Inventory valuation report showing unit cost

- SKU and quantity detail

- General ledger entry and approval

- Incident report, internal memo, or investigation notes

- Police report, if one was filed

- Insurance correspondence, if applicable

- Any photos, camera review notes, or exception reports

If your books are electronic, preserve the audit trail. A proper adjustment note in the inventory system can save hours of confusion later. “Adjusted by admin” is not a useful description. “Adjusted after cycle count confirmed 12 units stolen from warehouse B, approved by controller on March 14” is much better.

Step 8: Fix the control problem that allowed the loss

Recording stolen inventory is important. Preventing the next loss is even more important. Otherwise, you are basically becoming a very organized historian of your own problem.

Controls that usually help

- Separate custody of inventory from recordkeeping and adjustment authority

- Require approval for write-offs, returns, credits, and stock adjustments

- Perform regular cycle counts, especially on high-value and high-theft items

- Restrict access to high-risk inventory areas

- Review shrinkage by location, shift, employee group, or product family

- Use exception reports for voids, refunds, transfers, and unusual adjustments

- Train staff on receiving, labeling, returns, and documentation procedures

One of the most effective principles is old-school but powerful: the person who controls the records should not also control the asset. When one person can receive goods, adjust counts, approve write-offs, and reconcile reports, you are not running a control environment. You are handing out backstage passes.

Common mistakes to avoid

Even smart businesses make the same mistakes over and over. Here are the big ones:

- Recording the loss at selling price instead of cost

- Calling every discrepancy “theft” before verifying the count

- Leaving the asset on the books while waiting on insurance

- Posting the write-off without documentation or approval

- Claiming a tax deduction twice through both COGS and a separate loss

- Ignoring recurring shrinkage instead of investigating trends

The best stolen inventory accounting process is not flashy. It is boring in the most beautiful possible way: confirm, value, record, document, review, improve.

Real-world experiences businesses often have with stolen inventory

In the real world, stolen inventory rarely shows up as a cinematic event with a smashed window and a conveniently placed clue. More often, it starts with a count that looks off by just enough to make people suspicious but not enough to make them confident. A small hardware store might notice that premium drill bits are always short after weekend sales. At first, management assumes counting errors. Then the cycle counts keep showing the same pattern: high-theft items near the front counter are bleeding units. The accounting lesson is not just “book the loss.” It is “book the loss at cost, document the trend, and move the merchandise to a more secure display.” In that type of business, the fix often combines accounting discipline with store-layout changes.

An apparel boutique may have a very different experience. The owner might initially label all shortages as shoplifting, only to discover that part of the problem is sloppy receiving. Boxes are checked in too quickly, sizes are mixed, and returns are restocked without being scanned properly. On paper, it looks like theft. In practice, it is a messy blend of process failure and shrinkage. That is why experienced accountants are careful with language. They do not jump straight to “stolen” unless the facts support it. They start with a discrepancy, then refine the conclusion as evidence comes in.

Restaurants and bars also teach useful lessons. Missing liquor inventory may look like obvious theft, but sometimes the real culprit is overpouring, waste, or comps that never made it into the POS system. The accounting entry still removes missing value from inventory, but management decisions change depending on the cause. If the issue is theft, access controls and manager review become the focus. If the issue is waste, training and standard pour controls matter more. Either way, frequent reconciliation turns vague suspicion into useful data.

Manufacturers face yet another version of the problem. If raw materials disappear, the loss may ripple into work-in-process, production planning, and purchasing. A manufacturer that only adjusts finished goods while ignoring missing components can end up with distorted job costing and unreliable margins. In those environments, the experience often teaches a hard but useful lesson: inventory theft is not just a warehouse problem. It affects costing, forecasting, financial reporting, and operations all at once.

Across industries, the businesses that handle stolen inventory best are usually not the ones with the fanciest software. They are the ones with disciplined habits: frequent counts, clean approvals, good notes, and zero tolerance for mystery adjustments. They treat every discrepancy like a signal. Sometimes the signal says theft. Sometimes it says training issue. Sometimes it says system setup problem. But when management listens early, the accounting gets cleaner, the operational fixes get smarter, and the losses usually get smaller.

Final thoughts

Accounting for stolen inventory is not just about cleaning up a bad day. It is about protecting the accuracy of your financial statements and learning something useful from the loss. The right process is straightforward: verify the shortage, separate theft from general shrinkage, value the missing goods at cost, decide how to present the loss, record the journal entry, handle tax and insurance correctly, keep strong documentation, and tighten internal controls.

Do that consistently, and your books will tell the truth even when your inventory room does not. And in accounting, truth is still the most valuable thing you can keep in stock.