Table of Contents >> Show >> Hide

- Why rates hit purchase borrowing harder than people expect

- Refinancing didn’t just slowit became a different species

- So what do borrowers do instead?

- Who still borrows when rates are elevated?

- Evidence of the squeeze: sales, affordability, and what’s “improving” (even when it doesn’t feel like it)

- What would it take for mortgage borrowing to rebound?

- Conclusion: rates are the headline, but the story is bigger

- Real-World Experiences: What This Rate Era Feels Like (About )

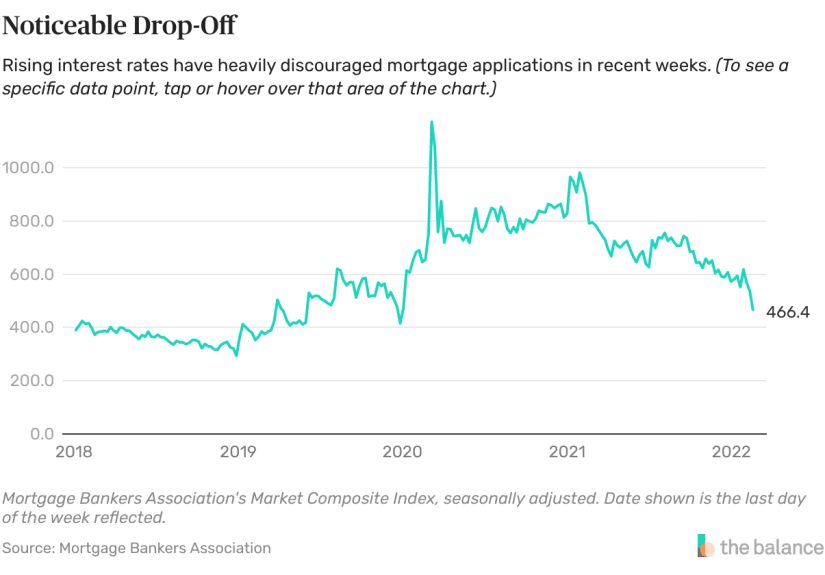

Mortgage rates have a special talent for ruining everyone’s plans at once. When rates rise, refinancing slowsno surprise.

But what’s been more telling in this cycle is how higher borrowing costs have also throttled new mortgage demand:

fewer purchase loans, fewer move-up buyers, and more would-be homeowners staring at a monthly payment like it just insulted their family.

In early 2026, the average 30-year fixed rate has hovered a little above 6%, according to the weekly survey that many housing

pros treat like a national mood ring. That’s meaningfully lower than the highs seen in prior years, but still miles away from

the pandemic-era “three-handle” rates that turned ordinary people into amateur real-estate moguls. With rates elevated, home prices

still high in many markets, and supply constrained, borrowing doesn’t just get expensiveit gets psychologically expensive.

And psychology, in housing, is half the underwriting.

Why rates hit purchase borrowing harder than people expect

1) The monthly payment math is brutal (and it shows up fast)

Let’s do the kind of math that makes group chats go quiet. Suppose someone borrows $320,000 on a 30-year fixed mortgage.

At 3%, the principal-and-interest payment is about $1,349/month. At 6%, it’s about $1,919/monthroughly $570 more, every month,

for the same house. Taxes and insurance are extra, and they haven’t exactly been on a diet lately.

This is why “rates are only a few points higher” is a misleading sentence. Mortgage rates aren’t like a mild sauce you can ignore;

they’re the main ingredient. Even when rates ease modestly, buyers are often still priced out because the payment is being

calculated on today’s prices, not 2019 prices.

2) The “rate lock-in” effect freezes existing inventoryand that freezes buyers

A huge share of homeowners are sitting on mortgage rates well below what’s available now. Moving means trading a low-rate mortgage

for a higher-rate one, which can feel like voluntarily downgrading your life. The result: fewer listings, less turnover,

and a market that doesn’t “clear” the way it normally would.

This lock-in dynamic isn’t just a seller story. Buyers get hit too, because when resale inventory is limited, choices shrink and

prices stay stickier than they should. Even when demand softens, a shortage of homes can keep prices from falling enough to restore

affordability. In other words: rates reduce demand, but tight supply can prevent demand from translating into better deals.

3) People don’t buy houses; they buy uncertainty

When rates are high and everyone expects them to fall “soon,” many buyers pause. Builders report this directly: a large share say

their biggest challenge is buyers waiting for prices or interest rates to drop. That waiting game shrinks purchase loan volume

even if the economy isn’t collapsing. Why lock in a payment today if you believe tomorrow’s payment might be cheaper?

4) Higher rates tighten the underwriting funnel

Higher payments push more borrowers against debt-to-income limits. That can turn a “pre-approved” shopper into a “pre-approved for

disappointment” shopper. Add in down payment requirements, credit standards, and the reality that starter homes aren’t always cheap

anymore, and a big chunk of demand never becomes an application.

Refinancing didn’t just slowit became a different species

Refinancing is usually the first thing to disappear when rates rise, because it’s a pure math decision. If you already have a 3%

mortgage, refinancing at 6% is like trading a bicycle for a treadmill and calling it “transportation.”

But refis also tell a deeper story: they often represent household balance-sheet management. When refinancing volume collapses,

fewer people are lowering their monthly payments, fewer are consolidating debt into a cheaper loan, and fewer are tapping equity via

cash-out refinances (which were popular when rates were low and prices were rising). That changes consumer behavior beyond housing:

less “found money,” fewer renovations financed via refi, and more reliance on other credit products.

The key point is that higher rates don’t only block optional refis. They ripple into purchase activity, move decisions, construction,

and household cash flowand they can keep the market sluggish even when rates drift down from their peaks.

So what do borrowers do instead?

Discount points, lender credits, and the return of “rate shopping”

When the sticker rate hurts, buyers look for ways to reshape it. Discount points are one of the most common tools: pay more upfront,

get a lower interest rate over the life of the loan. Lender credits flip the trade: pay a higher rate, reduce closing costs now.

The right choice depends on how long you’ll keep the mortgage and whether you expect to refinance later.

In a higher-rate environment, points become a strategic lever. Borrowers who expect to stay put for years may accept higher cash-to-close

in exchange for a lower payment. Others refuse to “pay extra” for a rate that still feels high, and instead focus on negotiating

seller concessions or choosing a less expensive home.

Builder incentives and mortgage rate buydowns

New-home builders have responded to affordability pressure by leaning hard on incentivesespecially mortgage rate buydowns.

Instead of dropping the headline price (which can upset prior buyers and reset comps), builders often prefer to subsidize the rate,

because it directly targets the monthly payment that buyers actually feel.

Think of it as the housing market’s version of “0% APR financing.” The home isn’t free, but the payment looks less terrifying.

This can shift borrowing away from the resale market toward new construction in certain metros, even if the broader market remains soft.

Smaller homes, different locations, and “good enough” decisions

When rates stay high, buyers compromise. They buy smaller. They choose a different neighborhood. They accept a longer commute.

They postpone a renovation. They bring in a co-borrower. In many cases, “forever home” becomes “for now home,” and the plan is to

refinance later if rates fall meaningfully.

Assumable loans and creative financing (within reason)

Some borrowers explore assumable mortgages, which can be available on certain government-backed loans, allowing a buyer to take over

a seller’s existing mortgage rate (subject to qualifications and logistics). Others use second mortgages or home equity lines to

reduce the size of the first mortgage. These strategies can be complex and aren’t universally available, but they reflect a simple truth:

when rates are high, people get motivatedand occasionally ingenious.

Who still borrows when rates are elevated?

1) Life-event buyers

Not all borrowing is optional. People move for jobs, marriage, kids, divorce, caregiving, and “my upstairs neighbor is practicing

the drums at 2 a.m.” Life events can overpower rate sensitivity.

2) First-time buyers (but at a lower share than a “healthy” market)

First-time buyers typically keep the market alive because they don’t have a low-rate mortgage to give up. But they also face the

toughest affordability math. When rates rise, first-timers feel it immediately, and the market loses a critical source of demand.

3) Buyers who can offset rates with cash, income, or concessions

Households with strong incomes, sizable down payments, or sellers willing to offer concessions can still transact. That creates a

market that feels uneven: some homes sell quickly, others sit, and many buyers feel like they’re losing to people with better balance sheets.

Evidence of the squeeze: sales, affordability, and what’s “improving” (even when it doesn’t feel like it)

Early 2026 data show existing-home sales running at a subdued pace, with prices still elevated and inventory tight relative to historical norms.

Even in periods when affordability metrics improve, the lived experience of buyers can remain harsh because the baseline is so stretched.

There are signs of incremental improvement in some placesmuted price growth, slightly lower rates than a year prior, and pockets where

income requirements are easing. But “improving” doesn’t always mean “good.” It can mean “still tough, but slightly less impossible.”

What would it take for mortgage borrowing to rebound?

A meaningful rate movenot just a tiny dip

Modest rate declines can help on the margin, but big behavioral shifts usually require a clearer signal. Many buyers need to see rates

fall enough to change the monthly payment in a way that feels realnot just “$27 less, wow, we’re saved.”

More inventory (especially resale listings)

If rate lock-in continues to suppress listings, the market can remain constrained even if demand returns. A healthier flow of homes

for sale would reduce bidding pressure and help prices normalize, making financing more feasible for a broader slice of buyers.

Stability and confidence

Housing doesn’t like surprises. When consumers feel uncertain about jobs, inflation, or where rates are headed, they pause.

A steadier outlookcombined with real affordability gainswould do more for borrowing than a thousand optimistic headlines.

Conclusion: rates are the headline, but the story is bigger

Yes, higher mortgage rates crush refinancing. But the bigger plot twist is how they also suppress purchase borrowing by reshaping

payments, freezing inventory through rate lock-in, tightening qualification, and changing buyer psychology. Even with rates hovering in the

low-6% range, many households are still doing the same math and reaching the same conclusion: “Not yet.”

The market can thawbut it likely needs a combination of lower borrowing costs, more homes for sale, and a sense that the next step won’t

immediately be punished by the rate gods. Until then, mortgage borrowing remains a story of hesitation, workarounds, and the occasional

buyer who shrugs and says: “Life’s happening. We’re doing it anyway.”

Real-World Experiences: What This Rate Era Feels Like (About )

If you want to understand how rates squelch borrowing, skip the spreadsheets for a second and listen to the way people talk about the process.

Many borrowers describe it as a three-stage journey: optimism, negotiation, and existential questioning.

Stage one is the hopeful scroll. A buyer sees a listing and thinks, “We can do this.” Then the mortgage calculator loads, and reality arrives

like a pop-up ad you can’t close. Buyers who would have comfortably qualified a few years ago suddenly find themselves playing defense:

raising the down payment, trimming the budget, or considering a smaller home that they swear is “cozy” (the real estate translation is

“we removed the dining room to make space for one extra closet”).

Stage two is the negotiation Olympics. Buyers become fluent in terms they didn’t know existed: seller concessions, discount points, temporary

buydowns, lender credits, and “please explain why the closing costs look like a luxury car payment.” Some buyers treat points like a

long-term investmentpay more now to pay less later. Others refuse on principle: “I’m not paying extra for the privilege of a still-high rate.”

Many end up striking a compromise: a smaller purchase price plus a buydown, or a slightly higher rate paired with lower cash needed at closing.

Stage three is the lock-in reality check. Move-up buyers often feel trapped by their current mortgage rate. They’ll say things like,

“We’d love more space, but our payment would jump by $800,” or “We can afford the new house, but it feels financially irresponsible.”

That hesitation keeps listings off the market, which frustrates buyers hunting for resale homesand it quietly pushes some demand toward

new construction, where builders can offer incentives that individual sellers usually can’t.

Another common experience is “rate whiplash.” Borrowers watch the market the way sports fans watch a close game. A small rate drop triggers a

burst of activitycalls to lenders, updated pre-approvals, frantic weekend showingsfollowed by another pause when rates tick back up or when

the perfect house gets snapped up by someone with more cash. Over time, this creates fatigue. People don’t just delay purchases because of money;

they delay because the process feels exhausting and unpredictable.

Yet deals still happenespecially for life-event buyers. In those cases, the mindset shifts from “timing the market” to “solving a problem.”

A couple expecting a baby, a family relocating for work, or someone downsizing after a major change may decide to buy now and refinance later if

rates fall. In this rate era, that’s the dominant emotional pattern: cautious optimism paired with a backup plan.