Table of Contents >> Show >> Hide

- The Scoreboard: Same IPO Era, Different Revenue Universes

- Why the Curves Diverged: Five Forces That Quietly Decide the Winners

- 1) The Market You Pick Is a Growth Rate You Inherit

- 2) Take-Rate Beats Seat-Rate When Your Customers’ Volume Explodes

- 3) Distribution Compounds More Than ProductBecause It Buys You More Product

- 4) Platform Expansion Is Not “More Features.” It’s “More Reasons to Stay.”

- 5) Competitive Gravity: Bundles Are Black Holes

- Company-by-Company: The Playbooks Behind the Outcomes

- The Counterintuitive Lesson: The Biggest IPO Revenue Didn’t Win the Revenue Race

- What Founders and Operators Can Steal From This Comparison

- So… Was This “Wildly Different” Outcome Inevitable?

- Field Notes: of “Lived Experience” Watching These Journeys Play Out

Three companies. Three IPOs in the same graduating class (2014–2015). Three wildly different “how big did you get?” answers.

If you like business stories with plot twists, this one has a few: the company that looked smallest at IPO now posts a revenue run-rate that could bench-press the other twocombined. And the one that looked biggest early on? It’s now the “steady and profitable” adult in the room… but not the revenue giant.

Before we jump in, a quick translation guide: public companies don’t always report “ARR” the same way startups do.

In public-market conversations, people often use ARR as shorthand for annual revenue run-rate

(latest quarter revenue × 4) or last-twelve-month revenue. That’s the spirit of the numbers in this article:

a scoreboard for scale, not a perfectly standardized SaaS metric.

The Scoreboard: Same IPO Era, Different Revenue Universes

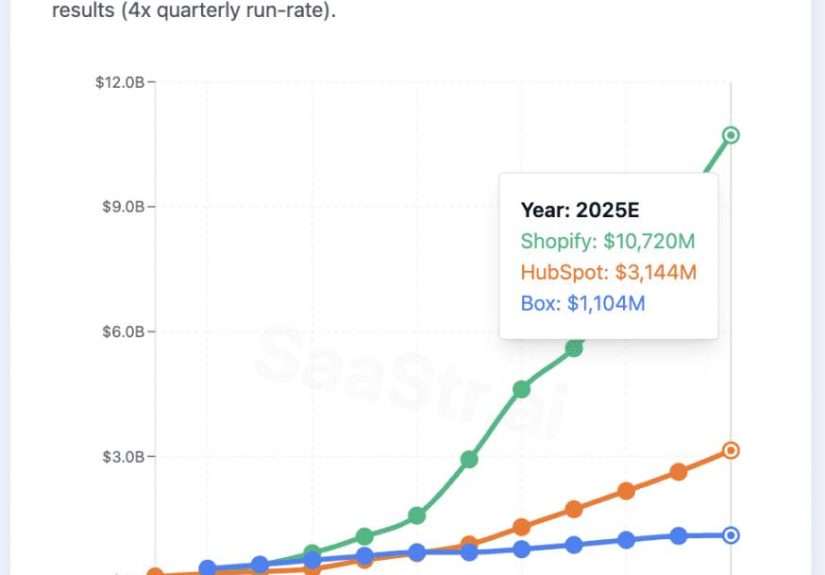

Let’s put the “then vs. now” side-by-side. (All figures rounded; “now” reflects reported results and guidance from 2025-era filings and earnings releases.)

| Company | IPO Timing (2014–2015) | Revenue Around IPO Era | “Now” Revenue Run-Rate / Revenue Scale | One-Line Read |

|---|---|---|---|---|

| Shopify | May 2015 IPO pricing at $17/share | ~$205M total revenue (2015) | ~$10–11B+ annualized pace (e.g., $2.844B in Q3’25) | Commerce platform + payments = compounding flywheel |

| HubSpot | Oct 2014 IPO pricing at $25/share | ~$116M total revenue (2014) | ~$3.1B+ revenue guidance for FY2025 | SMB-to-midmarket “customer platform” expansion done right |

| Box | Jan 2015 IPO pricing at $14/share | ~$216M revenue (FY2015) | ~$1.09B revenue (Fiscal 2025) | Enterprise content is valuable… and brutally competitive |

If you’re thinking, “Wait, Box was bigger than Shopify back then?”yep. That’s why this comparison is so useful.

It shows why early revenue size is a snapshot, not a destiny.

Why the Curves Diverged: Five Forces That Quietly Decide the Winners

1) The Market You Pick Is a Growth Rate You Inherit

Shopify rode the rise of direct-to-consumer, social commerce, and “everyone can be a merchant” tailwinds. HubSpot rode the steady digitization of marketing and sales

for small-to-midmarket businessesbig enough to be massive, structured enough to sell into, and messy enough that customers gladly pay to reduce chaos.

Box, meanwhile, lived in the land of “files, storage, and collaboration,” where giants already owned distribution and bundling power.

2) Take-Rate Beats Seat-Rate When Your Customers’ Volume Explodes

Here’s a simple (and slightly unfair) rule of thumb: if your revenue is tied to customer success volume, you get to grow when they grow.

Shopify isn’t just charging for software access; a meaningful portion of its business scales with merchant activitypayments, attach products, and services that rise with GMV.

HubSpot is mostly seat- and tier-based subscription (plus usage-like elements), which is still fantasticjust structurally less “automatic” than commerce volume.

Box is seat-based in a category where “good enough” frequently comes pre-installed in a broader suite.

3) Distribution Compounds More Than ProductBecause It Buys You More Product

Shopify built an ecosystem: apps, partners, agencies, developers, and a merchant community that sells the product for the company.

HubSpot did something similar with inbound content, certifications, partners, and a platform of hubsplus freemium on-ramps that turn curiosity into pipelines.

Box built strong enterprise relationships and compliance credibility, but enterprise distribution is slower, more procurement-heavy, and less viral.

4) Platform Expansion Is Not “More Features.” It’s “More Reasons to Stay.”

The real magic is when product expansion increases switching costs and earned retention.

Shopify expanded from “storefront + basics” into payments, checkout acceleration, enterprise capabilities, and a larger commerce operating system.

HubSpot expanded from inbound marketing into CRM, sales, service, operations, content/CMS, and newer commerce-related toolingbecoming the place where customer data lives.

Box has expanded into Intelligent Content Management, workflows, and securityvaluable, yesbut still adjacent to ecosystems customers already rent from Microsoft and Google.

5) Competitive Gravity: Bundles Are Black Holes

Box’s core problem isn’t that it’s a bad product. It’s that it’s an excellent product fighting bundle gravity.

When a product category is “included,” the buying conversation becomes, “Why should we pay extra?” That forces pricing pressure, longer sales cycles, and slower net-new growth.

Shopify and HubSpot have competition too, but their categories are less easily “thrown in for free” without breaking the buyer’s workflow.

Company-by-Company: The Playbooks Behind the Outcomes

Shopify: The Commerce Flywheel That Learned How to Lift

Shopify’s secret sauce is that it sells “running a business,” not “building a website.”

The storefront is the front door. The money is in what happens after customers walk in: checkout, payments, shipping logic, marketing integrations, analytics, and a thousand

“please don’t make me duct-tape this together” moments.

A useful way to visualize Shopify is as a set of compounding loops:

- More merchants → more GMV → more payment volume → more revenue to reinvest.

- More GMV → more partners and apps want to build → ecosystem gets stronger → more merchants join.

- More features → higher merchant maturity (SMB → midmarket → enterprise) → bigger accounts and longer retention.

By Q3 2025, Shopify reported revenue of $2.844B with strong year-over-year growth and an emphasis on free cash flow efficiency.

That’s the part a lot of people miss: Shopify didn’t just “grow.” It learned how to grow with discipline while still feeding the engine.

And Shopify’s category is huge because it’s not limited to “online stores.” It sits at the intersection of:

payments, logistics, customer identity, sales channels, and increasingly,

the “where commerce happens next” question. When AI-driven discovery changes shopping behavior, the companies closest to checkout can benefitbecause

they’re literally wired into the moment of transaction.

The punchline: Shopify’s revenue outcome looks “wild” because commerce is a volume gameand Shopify learned to capture that volume across the stack.

HubSpot: The SMB Customer Platform That Never Stopped Expanding the Job-to-Be-Done

HubSpot’s origin storymake marketing less painfulwas the wedge. The long-term plan was always bigger:

become the system of record and system of action for scaling businesses that don’t want a Frankenstein tech stack.

HubSpot’s growth advantage is that it sells to a market that is:

- Large (millions of SMBs and midmarket companies)

- Under-served (too big for spreadsheets, too small for heavyweight enterprise suites)

- Habit-forming (once your CRM and automation live somewhere, you don’t casually move it)

In Q3 2025, HubSpot reported total revenue of $809.5M, and issued full-year 2025 revenue guidance of roughly $3.113B–$3.115B.

The numbers matterbut the mechanism matters more: the company keeps increasing the number of teams that depend on the platform (marketing, sales, service, ops, content),

and it keeps reducing the friction to adopt (free tools, better onboarding, and platform cohesion).

There’s also a subtle strategic win: HubSpot turned “content and education” into a distribution asset.

The brand isn’t just known; it’s taught. That creates a talent pipeline of users who show up at new jobs already trained,

which is about as close as B2B gets to consumer-like pull.

The punchline: HubSpot’s revenue outcome is “smaller than Shopify” mainly because the underlying economic engine is different.

It’s still a monster outcomejust a subscription platform outcome, not a commerce take-rate outcome.

Box: Enterprise Content, Security Credibility, and the Long Shadow of the Suite

Box went public with strong momentum and meaningful revenue scale for the era.

It also had a clear enterprise story: secure content collaboration, governance, and compliance. That’s not a hobbyregulated industries pay real money for it.

In fiscal 2015, Box reported revenue of $216.4M. Fast forward to fiscal 2025, and Box reported revenue of $1.09B with strong gross margins

and leaned into Intelligent Content Management (ICM) and AI-powered capabilities.

So why isn’t Box in the $3B–$10B+ club?

- Category overlap: file storage and collaboration became table stakes inside broader suites.

- Procurement physics: enterprise deals are powerful but slower, and “rip-and-replace” is rare.

- Bundling pressure: even if Box is better, “already paid for” is a persuasive competitor.

To be clear: $1B+ revenue with strong margins is not failure. It’s a different kind of victorymore “durable enterprise utility” than “explosive platform compounding.”

The market simply rewards these two stories differently on the scale dimension.

The Counterintuitive Lesson: The Biggest IPO Revenue Didn’t Win the Revenue Race

HubSpot and Shopify were smaller businesses around the IPO era than Box on certain snapshots. Today, both are far larger by annual revenue pace.

That’s not a dunk on Boxit’s proof that the shape of your business model matters as much as early traction.

A few “shape” differences that show up over a decade:

-

Attach surface area: Shopify’s merchant stack has many places to add value (and revenue).

HubSpot does too, but it’s still mostly subscription expansion rather than transaction scale. - Volume tailwind: commerce GMV can surge with macro shifts and new channels; software seats generally grow more steadily.

-

Bundle resistance: HubSpot and Shopify are harder to replace with “included” alternatives without meaningful workflow pain.

Box’s core use case is more exposed to suite bundling.

What Founders and Operators Can Steal From This Comparison

Steal #1: Pick a core metric that naturally compounds

Shopify’s compounding metric is merchant activity; HubSpot’s is team adoption across the customer journey; Box’s is enterprise trust and governance.

None are “wrong.” But some compound faster by default.

Steal #2: Make expansion feel like relief, not upsell

The best expansion doesn’t feel like “Would you like fries with that?” It feels like, “Thank you for removing another headache.”

Shopify did this by moving deeper into payments and commerce operations; HubSpot did it by connecting teams inside one platform.

Steal #3: Build distribution that’s not purely paid

Content, community, partners, agencies, app ecosystemsthese are not marketing “nice-to-haves.”

They’re long-duration growth assets that keep working when acquisition costs get cranky.

Steal #4: Avoid categories where the best competitor is “already on the invoice”

If you’re going to live near a giant suite, you need a plan: either be so differentiated that the suite can’t match you,

or become the default partner inside the suite’s ecosystem. Otherwise, you’re fighting gravity with a paper airplane.

So… Was This “Wildly Different” Outcome Inevitable?

Not inevitablebut path-dependent. Shopify caught a once-in-a-generation commerce platform moment and built a take-rate and ecosystem machine.

HubSpot executed a decade-long platform expansion into a coherent customer suite for scaling businesses.

Box built an enterprise-grade product in a category where bundling and incumbents compress growth.

Same IPO era. Different market physics. Different revenue engines. Different outcomes.

And that’s the real lesson: decade-scale results are less about “who was hot at IPO” and more about “whose model compounds the longest.”

Field Notes: of “Lived Experience” Watching These Journeys Play Out

If you’ve ever been in a planning meeting where someone says, “We just need to add one more feature and growth will happen,” these three stories are the polite,

real-world rebuttal. What it feels like to watch Shopify, HubSpot, and Box over a decade is realizing that growth isn’t one leverit’s a room full of levers,

and some companies keep finding new ones without snapping the old ones off.

With Shopify, the experience is watching merchants go from “I made my first sale!” to “I have a finance team now,” and noticing how the platform shows up at every stage.

The early days feel like templates and themes and shipping labels. Then a merchant starts caring about conversion, checkout speed, and abandoned carts.

Then payments, fraud tooling, and multi-channel inventory become existential. The “aha” moment is when you realize Shopify didn’t just sell software to start a storeit

positioned itself where merchants’ money moves. When the holiday rush hits, nobody says, “I hope my logo looks nice.” They say, “Please let checkout survive.”

Being close to that moment of truth is how you earn pricing power without acting like a villain.

HubSpot’s journey feels like watching a tool become a language. Early on, people talk about inbound marketing like it’s a trick: blog, SEO, nurture emails, repeat.

Then the sales team shows up and says, “Wait, where are the leads?” and suddenly CRM stops being a department tool and becomes a company tool.

The experience operators often describe is “We didn’t plan to buy five hubswe just kept trying to stop duct-taping systems together.”

The funniest part is how quickly teams normalize improvements. After a month, it’s not “Wow, automation saved us.” It’s “Why doesn’t everything work like this?”

That’s how platforms quietly win: not with fireworks, but with fewer headaches at 4:55 p.m. on a Friday.

Box feels like the enterprise version of growing up: fewer memes, more compliance. The lived experience here is security reviews, procurement cycles,

“Can you show me the audit trail?” conversations, and the realization that being trusted is a product feature.

When Box leans into Intelligent Content Management and AI, the promise is compellingmake the mountain of content not just stored, but useful.

But you also feel the weight of competing against “default choices.” In the enterprise, the hardest competitor to beat is not a better productit’s inertia.

People don’t switch because they’re busy. They switch when pain becomes bigger than effort.

The shared operator takeaway across all three is surprisingly human: companies scale when they repeatedly remove friction at the exact moment customers feel it most.

Shopify does it at checkout and commerce operations. HubSpot does it across the customer journey and internal handoffs.

Box does it in trust, governance, and secure content workflows. The revenue outcomes look “wildly different,” but the lived experience is consistent:

compounding is less about one big bet and more about a thousand small decisions that make customers say, “Okay… I’m not leaving.”