Table of Contents >> Show >> Hide

- Why It Feels Like Money Is Everywhere

- Money Is Not Just Spending Power. It Is Also Stored Power.

- Where the Money Actually Sits

- If There Is So Much Money, Why Do So Many People Feel Broke?

- The Cultural Side of Financial Abundance

- What This Means for Businesses, Investors, and Households

- So, Is “So Much Money Everywhere” a Good Thing?

- Experiences That Make “So Much Money Everywhere” Feel Real

- Conclusion

Walk through any major city and the signs are impossible to miss. New towers are going up. Luxury stores are still glowing like they run on pure confidence. Startups raise rounds with names that sound like movie sequels. Government debt counters move so fast they look like they are trying to escape the screen. Your social feed is full of private jets, private credit, private islands, and very public bragging. It creates a strange modern feeling: there is so much money everywhere.

And yet, plenty of ordinary households are staring at rent, groceries, insurance bills, and medical costs like they are boss fights in a video game. That tension is the real story. This is not just an article about “lots of money.” It is about where money sits, how it moves, why asset-rich economies can still feel financially exhausting, and why abundance at the system level does not automatically translate into ease at the kitchen-table level.

In other words, yes, there is a lot of money around. No, that does not mean it is in your checking account wearing a friendly smile.

Why It Feels Like Money Is Everywhere

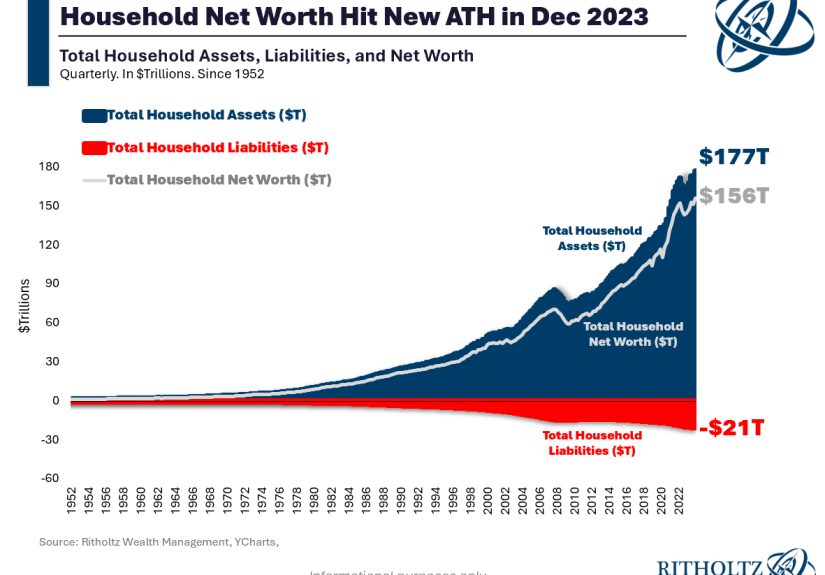

Modern economies are not built around piles of cash stacked in a cartoon vault. Money today is largely digital, institutional, and layered. It shows up as bank deposits, money market fund balances, Treasury securities, retirement accounts, real estate equity, private equity commitments, corporate bonds, and lines of credit. That matters because when people say, “There is so much money everywhere,” they are usually reacting to the scale of financial assets, not a sudden nationwide outbreak of overflowing wallets.

The United States alone operates inside a financial system measured in tens of trillions of dollars. Household wealth is enormous. Money market funds have hit record levels. Debt issuance remains huge. Asset managers oversee jaw-dropping pools of capital. Private markets continue to attract institutional investors hunting for yield, scale, and control. Even cautious savers are parking cash in interest-bearing vehicles that once sounded too boring to trend.

This creates a world in which money is constantly visible through prices, valuations, fundraising headlines, home values, stock indexes, and government financing. It is everywhere because finance is everywhere. It sits behind the mortgage market, retirement plans, venture capital, infrastructure deals, municipal bonds, and the humble checking account that still somehow makes you feel rich for seven minutes after payday.

Money Is Not Just Spending Power. It Is Also Stored Power.

One reason the economy can look cash-soaked is that money is stored in assets, not merely spent in stores. When home prices rise, people may not feel richer in daily life, but on paper their balance sheets swell. When stock markets climb, retirement accounts rise with them. When short-term rates remain attractive, savers move funds into money market accounts. When institutional investors commit capital to private markets, that money does not vanish. It waits, earns, rotates, and reappears in another corner of the system.

In practical terms, the phrase “so much money everywhere” often reflects a world full of claims on future income. Stocks represent claims on future profits. Bonds represent claims on future payments. Real estate reflects the present value of future rents or housing services. Private funds collect capital now to deploy later. Government debt lets spending happen in the present while repayment is spread into the future. Modern finance is less a bucket of cash than a giant machine for moving value across time.

That is why periods of high asset values can feel oddly detached from everyday cash flow. A family can own a home worth far more than it was five years ago and still dislike the price of eggs. A retiree can watch a portfolio recover while still cutting restaurant visits. A founder can raise capital and still worry about runway. Abundance and anxiety can coexist quite comfortably. Annoyingly comfortably.

Where the Money Actually Sits

1. Household Wealth and Retirement Assets

A huge share of modern money is embedded in household balance sheets. That includes housing equity, pensions, retirement accounts, brokerage accounts, and other financial holdings. On paper, that makes the economy look spectacularly wealthy. In reality, access to that wealth depends on age, income, geography, timing, and whether you can tap it without triggering taxes, debt, or regret.

Retirement wealth is a perfect example. A 401(k) may look healthy, but it is not the same as spending cash. It is future consumption wearing a suit and asking you to be patient. For millions of Americans, wealth exists, but it is locked behind time, market risk, and the basic social rule that liquidating your retirement plan to buy groceries is generally a bad plot twist.

2. Money Market Funds and Safe-Haven Cash

One of the clearest examples of money feeling “everywhere” is the sheer amount parked in money market funds. These funds became especially attractive when short-term interest rates offered savers a decent return without requiring heroic risk tolerance. That shift matters because it reveals a key truth about modern money: even caution can become a large-scale financial event.

When households, companies, and institutions move cash into money market vehicles, the result is not a dramatic shopping spree. It is quiet financial accumulation. The money is still there. It is simply sitting in a high-visibility parking lot, collecting yield and waiting for instructions.

3. Debt Markets

Debt is the shadow twin of abundance. The world can look full of money partly because it is also full of borrowing. Governments issue debt. Companies refinance and expand through debt. Consumers use mortgages, credit cards, auto loans, and personal loans. Debt allows money to appear in the present by pulling future income forward.

This is why a debt-heavy world can feel wealthy and fragile at the same time. Credit fuels growth, investment, consumption, and liquidity. But it also creates obligations, rollover risks, and pressure when rates stay higher for longer. A world rich in capital is often equally rich in promises.

4. Private Capital and Nonbank Finance

Another reason money seems to be everywhere is that more of it now lives outside traditional banks. Private equity, private credit, infrastructure funds, hedge funds, insurance-linked vehicles, and other nonbank financial institutions play a larger role in allocating capital than they once did. This shift broadens the financial ecosystem and makes capital more mobile, more specialized, and sometimes more opaque.

For businesses, this can mean more funding channels. For the financial system, it means more complexity. For the average person, it means the word “liquidity” now appears in articles that should honestly come with a cup of coffee and a translator.

If There Is So Much Money, Why Do So Many People Feel Broke?

Because aggregate abundance is not the same thing as broad comfort.

This is the most important idea in the whole discussion. A country can have enormous household net worth, giant capital markets, and record fund balances while many residents still feel squeezed. That happens when money is concentrated in specific assets, specific institutions, and specific income groups. It also happens when the prices of essential goods rise faster than the emotional ability of human beings to stay calm in a grocery aisle.

Distribution matters. Asset ownership matters. Timing matters. A surge in stock values mostly benefits people who own a meaningful amount of stocks. A rise in home values helps owners more than renters. Higher short-term yields reward savers with cash balances but can raise borrowing costs for households carrying variable-rate debt or businesses refinancing loans. The same financial condition can feel like a blessing in one zip code and a nuisance in the next.

Affordability adds another layer. Even when inflation cools, the price level remains higher than it was before the recent inflation spike. Households do not compare today’s prices only to last month. They compare them to what life felt like before bills started acting like they had a personal grudge.

That is why the economy can produce two honest statements at the same time: there is a vast amount of money in the system, and a large number of people still feel financially stressed. Both are true. The first describes scale. The second describes access.

The Cultural Side of Financial Abundance

The feeling that money is everywhere is also cultural. It comes from visibility. We live in an age when wealth is more public, more aesthetic, and more algorithmically amplified. Luxury once lived in neighborhoods. Now it lives in feeds. A person does not have to walk past a mansion to feel poor. They can just open an app while eating leftover pasta.

This changes how financial abundance feels. It is no longer only a matter of economic statistics. It is also a matter of performance. Wealth gets packaged as content. Capital becomes a vibe. A funding round is announced like a movie trailer. A home renovation becomes a lifestyle brand. The result is a strange psychological economy in which money is not merely used or invested. It is displayed.

That visibility can distort expectations. It can make extreme wealth look normal, easy, and common. It can blur the difference between genuine financial security and flashy consumption financed by leverage, timing, or branding. Not every luxury car is a balance sheet. Sometimes it is just a very expensive selfie with monthly payments.

What This Means for Businesses, Investors, and Households

For businesses, a money-rich environment can create opportunity. There may be more capital available, more investors seeking returns, and more demand for financial products, services, and innovation. But it also raises expectations. Capital becomes choosier when risks rise. Investors still want growth, but now they also want discipline, cash flow, and fewer fairy tales.

For investors, the lesson is that scale does not erase risk. Record asset values, giant debt markets, and abundant liquidity can coexist with volatility, concentration, and painful repricing. Money everywhere does not mean safety everywhere.

For households, the main takeaway is simpler: do not confuse the size of the financial system with your own financial position. The economy may be awash in money, but your plan still needs to be personal. Emergency savings, debt management, diversified investing, and realistic spending choices remain stubbornly useful. Boring advice survives because it works.

So, Is “So Much Money Everywhere” a Good Thing?

It can be. A deep, well-capitalized financial system can support innovation, retirement security, homeownership, government services, and business growth. It can cushion shocks and expand opportunity. In that sense, a large and liquid economy is a feature, not a bug.

But scale without balance creates tension. When money pools faster than access broadens, people notice. When wealth rises faster than affordability, people notice. When financial headlines feel euphoric while everyday budgets feel tight, people definitely notice.

So much money everywhere is not really a story about excess alone. It is a story about placement. Where money sits. Who owns it. Who borrows it. Who manages it. Who pays more to access it. And who gets told the economy is strong while quietly checking the price of detergent.

That is the paradox of modern abundance. The money is real. The imbalance is real too.

Experiences That Make “So Much Money Everywhere” Feel Real

The saver’s experience is one of the strangest. For years, many people earned next to nothing on cash, then suddenly money market yields became interesting again. A cautious person who never wanted to chase hot stocks could finally park cash somewhere and feel mildly competent instead of financially invisible. On paper, that is a win. In practice, it is also a reminder that even “safe money” is now part of a giant, highly responsive market machine. Grandma’s cash is no longer just in a drawer. It is participating.

The renter’s experience is different. They hear that markets are up, household wealth is enormous, and investors are optimistic, but their own budget feels like a stressed-out group project. Rent is still high. Moving costs money. Deposits are painful. Buying a home feels like trying to board a train that left the station, circled the planet, and came back with higher interest rates. To them, money is definitely everywhere. It is just mostly visible in home values, developer projects, and listings they cannot afford.

The small-business owner sees abundance in fragments. Customers still spend, lenders still market products, and headlines keep talking about capital flowing into this fund or that sector. But payroll is expensive, insurance bites, borrowing is not cheap, and one slow month can still ruin the mood for an entire quarter. Their experience of money everywhere is not carefree. It is more like standing in the middle of a river and realizing none of the water belongs to you unless you can route it, price it, and invoice it correctly.

The professional investor or startup founder experiences abundance as both opportunity and pressure. There may be more capital vehicles than ever, but there is also more scrutiny. Money is available, yet it wants a better story, cleaner economics, and a credible path to returns. In earlier boom times, charisma sometimes got the first meeting. Now the spreadsheet wants a speaking role too. The feeling of “so much money everywhere” remains, but it has matured. Capital is interested, not naive.

The ordinary family often lives in the contradiction most clearly. Their retirement account might be up. Their home might be worth more than expected. Their paycheck may even be larger than it was a few years ago. Yet groceries still feel expensive, health costs remain unpredictable, and one broken appliance can turn a calm week into a budgeting summit. Their life explains the topic perfectly: abundance can exist at the macro level while vulnerability remains stubbornly personal. That is why the phrase sticks. It sounds flashy, but underneath it is a serious question about who actually gets to feel the economy’s wealth in everyday life.

Conclusion

“So Much Money Everywhere” is more than a catchy phrase. It is a useful way to describe the modern economy’s most obvious contradiction: enormous financial scale living side by side with very ordinary financial stress. The system is bigger, deeper, and more liquid than ever. Wealth is vast. Capital is mobile. Markets are dense. Debt is huge. Cash has places to go. Investors have vehicles for everything from short-term safety to long-term speculative ambition.

But none of that cancels out the lived reality of affordability, inequality, and uneven access. The money is there. The question is how evenly it is distributed, how productively it is used, and whether the people who generate the economy’s energy actually feel its rewards. That is the real heart of the story. Not whether there is money everywhere, but whether abundance can become more livable.