Table of Contents >> Show >> Hide

- From Pensions to Personal Responsibility: Why the 401(k) Matters More Than Ever

- 401(k) by the Numbers: How Central It Has Become

- Generations and the 401(k): Different Starting Lines, Same Race

- Why the 401(k) Is Increasingly Non-Optional

- Common-Sense Ways to Get the Most from Your 401(k)

- Experiences From the Front Lines of 401(k) Saving

- Conclusion: Treat Your 401(k) Like the Essential Tool It Is

If retirement once felt like a comfy pension-powered train that showed up on time, today it’s more like a “build-your-own-vehicle” project.

For most American workers, that vehicle is the 401(k). Love it or hate it, this employer-sponsored plan has become the centerpiece of retirement savings in the United States, and its importance just keeps growing.

Traditional pensions are fading, Social Security faces long-term questions, and the cost of living in retirement keeps climbing.

In the middle of all that, the humble 401(k) has quietly turned into one of the primary tools for building a future paycheck.

Understanding how it works – and how to use it wisely – is no longer optional. It’s common sense.

From Pensions to Personal Responsibility: Why the 401(k) Matters More Than Ever

A generation or two ago, many workers could rely on defined benefit pensions. You worked for a company, the company promised a monthly income for life, and the math was largely their problem, not yours.

Today, that world is disappearing. Access to traditional pensions is now concentrated in a shrinking slice of employers, especially in the private sector, while defined contribution plans like 401(k)s dominate.

At the same time, access to 401(k)-style plans has broadened dramatically. More and more employers – including small businesses – now offer some version of a workplace retirement plan, often with automatic enrollment, an employer match, or both.

In many industries, not offering a retirement plan makes it hard to compete for talent. The result: for a majority of private-sector workers, if you’re going to build long-term wealth, your 401(k) is front and center.

The Big Shift: From Guaranteed Income to DIY Nest Egg

This shift from pensions to 401(k)s isn’t just a paperwork change; it’s a change in who carries the risk:

- Investment risk moved from company actuaries to individual workers.

- Longevity risk – how long your money has to last – is now your problem to solve.

- Behavior risk – skipping contributions, cashing out early, chasing hot stocks – matters far more.

The upside? If you contribute regularly, invest sensibly, and start early, a 401(k) can be an incredibly powerful compounding machine.

The downside? If you ignore it, it will ignore you right back – and future you may not find that very funny.

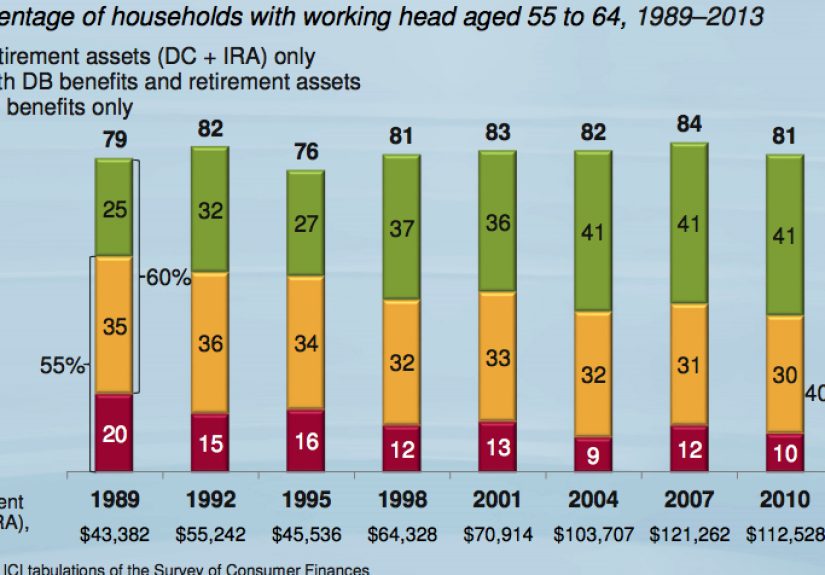

401(k) by the Numbers: How Central It Has Become

To understand why the 401(k) has become so important, it helps to look at a few broad trends and statistics. Across the retirement system, trillions of dollars now sit in defined contribution plans, including 401(k)s, 403(b)s, and similar accounts.

These balances make up a large chunk of total household financial assets in the United States.

Access and Participation

In recent years, the percentage of workers with access to a retirement plan at work has climbed, especially in larger companies and certain industries.

Automatic enrollment, state-facilitated retirement programs, and federal incentives have all nudged more employers to adopt 401(k)-style plans.

Yet there is still a meaningful coverage gap: millions of Americans, especially lower-wage and part-time workers, have no workplace plan at all.

Even when workers do have access, not everyone participates. Some never enroll, some defer too little to make a difference, and some cash out when they change jobs.

That’s one reason policy makers have pushed for automatic enrollment and auto-escalation features – they make the “right” decision the default decision.

Average Balances and the Reality Check

Look at average 401(k) balances, and things can seem encouraging. In recent reports from major providers, average balances across all participants have reached record or near-record levels, helped by market gains and higher savings rates.

Long-time savers who have stayed invested for decades can accumulate substantial nest eggs; some even cross the “401(k) millionaire” threshold after years of steady contributions and compounding.

The median, however, tells a different story. Many households sit far below those eye-catching averages.

A typical worker’s retirement savings might be in the tens of thousands rather than hundreds of thousands, especially if they started late, changed jobs frequently, or spent periods out of the workforce.

For near-retirees, that gap between what they have and what they’ll likely need can be sobering.

As living costs in retirement – housing, healthcare, food, transportation – continue to climb, relying solely on Social Security and a modest 401(k) balance can leave a serious shortfall.

That’s exactly why using your 401(k) thoughtfully has become a matter of necessity, not just financial hobbyism.

Generations and the 401(k): Different Starting Lines, Same Race

Another reason the 401(k) looms so large: almost every generation now interacts with it in some way.

Gen Z: The Early-Bird Advantage

Many Gen Z workers are entering the workforce with automatic enrollment in a 401(k) from day one. Their balances are still small – think four to five figures – but they have something the rest of us would pay dearly for: time.

With decades of compounding ahead, even relatively modest contributions can snowball into serious money later.

The key for Gen Z is simple but powerful:

- Stay enrolled – don’t opt out just to “wait until later.”

- Capture the full employer match – that’s free money, not a suggestion.

- Embrace long-term investing – broad, diversified funds instead of chasing memes or timing markets.

Millennials: In the Middle of Everything

Millennials are now well into their prime earning years, but many are balancing competing financial pressures: student loans, kids, housing costs, and uneven career paths.

Their average 401(k) balances are higher than Gen Z’s but often still behind where retirement experts would like to see them.

For this group, small changes can have big long-term impact:

- Increase contribution rates a percent or two each year, especially after raises.

- Consolidate old 401(k)s from previous jobs instead of cashing them out.

- Avoid loans or early withdrawals that restart the compounding clock in the wrong direction.

Gen X and Boomers: The Home Stretch

Gen X and Baby Boomers hold much of the total 401(k) assets. Their average balances can look impressive on paper, but remember: averages are pulled up by those with very high savings. Many near-retirees still have balances that are too small to fully cover their expected living expenses, especially over a multi-decade retirement.

Catch-up contributions, delayed retirement, and careful withdrawal strategies all become crucial at this stage.

The 401(k) isn’t just a savings account anymore; it’s the engine that may need to convert into a paycheck replacement – ideally for as long as you’re around to spend it.

Why the 401(k) Is Increasingly Non-Optional

So what is actually driving the “increasing importance” of the 401(k)? Several forces are at work, all pointing in the same direction.

1. Traditional Pensions Are Rare Outside Government and Legacy Employers

In most private-sector industries, defined benefit pensions are either closed, frozen, or simply never existed. Workers who still have pensions are the exception, not the rule.

That leaves the 401(k) as the primary workplace vehicle for retirement saving.

2. Social Security Is a Foundation, Not a Full Plan

Social Security provides a crucial baseline of income, but for most people it won’t cover everything.

The program was designed to replace a portion of your pre-retirement income, not to single-handedly fund a comfortable lifestyle, healthcare costs, and the occasional plane ticket to go hug your grandkids.

As life expectancies increase and healthcare costs remain high, relying on Social Security alone becomes riskier.

Your 401(k) – plus other savings and possibly IRAs or taxable investments – helps fill the gap between “bare minimum survival” and “reasonably comfortable retirement.”

3. Policy and Employer Design Are Pushing More Savings into 401(k)s

Over the past decade, policy changes have steadily nudged people toward saving in 401(k)-type plans.

Tax credits for small businesses, state-run auto-IRA programs, federal rules encouraging automatic enrollment, and potential future matching credits for low-income savers all reinforce the status of the 401(k) as the default retirement channel.

Meanwhile, plan design has improved. More plans now:

- Automatically enroll new employees at a default contribution rate.

- Offer auto-escalation, nudging contributions higher over time.

- Provide target-date funds as an easy, age-based investment option.

- Negotiate lower fees and a curated menu of diversified funds.

All of this makes it easier for the average participant to do “pretty much the right thing” without being a market expert.

4. The Behavior Gap: The 401(k) Rewards Consistency

One of the underrated reasons the 401(k) matters so much is that it’s behaviorally friendly when set up well.

Contributions are taken straight from your paycheck before you can talk yourself out of saving. Employer matches create a built-in incentive not to quit.

And the tax advantages make saving feel less painful than it would in a regular taxable account.

Over long periods, the biggest driver of 401(k) success isn’t picking the perfect fund; it’s sticking with a sensible plan through market ups and downs.

That ability to “set it and mostly forget it” is a big reason 401(k)s, despite their flaws, have become such a central pillar of American retirement.

Common-Sense Ways to Get the Most from Your 401(k)

If the 401(k) is increasingly important, the next logical question is: how do you use it wisely? Here are some practical, evidence-based, common-sense guidelines.

1. Don’t Miss the Match

If your employer offers a match – for example, 50% on the first 6% you contribute – make it your minimum savings goal to get all of it.

Not contributing enough to earn the full match is like turning down a raise that’s written right into your benefits package.

2. Aim for a Double-Digit Savings Rate Over Time

Many retirement experts suggest a total savings rate (your contributions plus employer match) in the low- to mid-teens as a long-term target.

You don’t have to get there in year one – especially if you’re just starting your career – but use raises and bonuses as opportunities to bump up your deferral.

A simple rule: every time you get a raise, send 1% of that new salary directly to your 401(k) before lifestyle creep eats it.

3. Use Simple, Diversified Investments

Most 401(k) plans offer a menu of mutual funds or ETFs. You don’t need to love picking funds to invest effectively:

- Consider a target-date fund that automatically adjusts as you age.

- If you prefer to build your own mix, focus on broad index funds for U.S. and international stocks plus a core bond fund.

- Keep an eye on fees – lower-cost funds tend to outperform, especially over long horizons.

4. Avoid “Raiding” Your 401(k)

Loans and early withdrawals may seem like easy money, but they come at a serious cost: taxes, penalties, and years of lost compounding.

Try to treat your 401(k) as a “do not touch until retirement” account. Emergency fund first, credit card second, 401(k) break-glass-only-if-it’s-absolutely-dire.

5. Stay the Course During Market Turbulence

Markets will rise, fall, and occasionally scare the daylights out of you. That’s normal.

What typically matters most is staying invested, continuing contributions, and resisting the urge to panic-sell when headlines are loudest.

Historically, long-term investors who stick with a diversified 401(k) portfolio through multiple cycles have been rewarded, while those who jump in and out of the market often lock in losses and miss recoveries.

Experiences From the Front Lines of 401(k) Saving

Statistics are helpful, but personal stories often make the stakes feel real. Here are a few composite examples, based on common real-world patterns, that show how 401(k) behavior can play out over time.

Sara: The Early Starter

Sara starts her first full-time job at 23. HR auto-enrolls her in the 401(k) at 4% of pay, with a company match of 100% up to 4%. She’s not thrilled about seeing less in her paycheck, but the idea of “free money” hooks her.

Over the next decade, Sara nudges her contribution up by 1% every year or two, especially when she gets a raise. By her mid-30s, she’s saving 10% of her salary plus the employer match, all in a low-cost target-date fund.

She lives through a couple of market downturns but resists the temptation to stop contributing. When she logs into her account in her early 40s, she’s shocked: the balance is larger than she’d ever imagined.

It’s not magic – it’s simply the combination of time, steady saving, employer money, and compounding doing their thing quietly in the background.

Jason: The Late Realization

Jason spends most of his 20s and early 30s hopping jobs and prioritizing immediate expenses. He contributes sporadically to his 401(k)s and sometimes cashes out small balances when he changes employers –

that “tiny” $5,000 account never feels worth rolling over.

At 40, he and his partner sit down with a financial planner and realize that their combined retirement savings are far below where they’d like to be. The goal of retiring in their early 60s still looks possible, but it will require a much higher savings rate going forward.

Jason starts maxing out his 401(k) contributions, rolls all old accounts into his current plan, and stops raiding his retirement money for short-term needs.

He also uses catch-up contributions once he hits 50. While he’ll probably never reach the same level as someone who started early and stayed consistent, his course correction still dramatically improves his outlook.

Linda: The Almost-There Reality Check

Linda is 58 and has been with the same employer for years. She’s done a lot of things right: contributed steadily, captured the full match, and kept her 401(k) invested in a balanced mix of stock and bond funds.

On paper, her balance looks strong compared with national averages.

But when she and her advisor run the numbers, they discover that her 401(k), plus expected Social Security benefits, will only cover a portion of her desired retirement lifestyle.

She wants to travel more, help her grandkids with college, and feel secure about healthcare costs.

Instead of panicking, Linda chooses a multi-step plan: work a couple of extra years, increase contributions during those years, and be flexible about her retirement budget.

Her 401(k) doesn’t magically become a pension, but thoughtful planning turns a potential shortfall into a manageable gap.

What These Stories Have in Common

Each of these stories highlights a few key truths about the increasing importance of the 401(k):

- Starting early is a huge advantage, but starting now is always better than waiting.

- Behavior – savings rate, consistency, and staying invested – matters at least as much as investment selection.

- Course correction is possible, especially if you’re honest about the gap between where you are and where you need to be.

None of these people needed to be financial geniuses. They simply needed to treat their 401(k) as a core part of their financial life, not a dusty side account they only remember when HR sends a reminder email.

Conclusion: Treat Your 401(k) Like the Essential Tool It Is

The 401(k) isn’t perfect. It doesn’t solve coverage gaps for all workers, it relies heavily on individual behavior, and it can be confusing for newcomers.

But in the real world we live in – with fewer pensions, rising longevity, and uncertain future benefits – it has become one of the most powerful and flexible tools available for building financial independence.

Using your 401(k) wisely doesn’t require complicated strategies. It requires common sense:

- Enroll early and stay enrolled.

- Grab the full employer match.

- Aim for a healthy long-term savings rate.

- Invest in diversified, low-cost funds.

- Resist panic and short-term temptations.

Do those things, and your 401(k) can move from “vague line on a pay stub” to “cornerstone of your future freedom.”

In a world where more responsibility is landing on individual shoulders, that’s not just smart investing – it’s a wealth of common sense.