Table of Contents >> Show >> Hide

- The IPO Window Did Not Reopen by Accident

- The Data Says the Market Is Back Even If the Counting Gets Weird

- Five Forces Driving the Rebirth of the IPO

- Proof the Comeback Is Real: Recent IPOs That Mattered

- Why This Comeback Looks Better Than the Last Mania

- Who Benefits Most From the Rebirth?

- What Could Still Derail the Momentum?

- The Experience of the IPO Rebound: What It Feels Like on the Ground

- Conclusion: The IPO Is Back, but in a Smarter Form

For a while, the IPO market looked less like a launchpad and more like a waiting room with bad coffee. Founders waited. Bankers rehearsed optimism. Private equity firms stared at aging portfolio companies the way people stare at leftovers on day four: still technically fine, but increasingly concerning.

Then something changed.

Not overnight, and not with the wild, confetti-cannon energy of 2021. The comeback has been slower, stricter, and a lot more grown-up. But that is exactly why it matters. The rebirth of the IPO is not just a return of stock market debuts. It is a return of confidence, price discovery, and a healthier relationship between private ambition and public scrutiny.

In other words, Wall Street did not fall in love with IPOs again because it got sentimental. It fell back in love because the math started to work.

The IPO Window Did Not Reopen by Accident

To understand why the IPO market is back, it helps to remember why it went quiet in the first place. The post-2021 freeze was driven by a brutal mix of high interest rates, valuation compression, inflation fears, geopolitical tension, and a stock market that had very little patience for unprofitable growth stories. Companies that might have gone public in an easier era chose to stay private, raise secondary capital, cut costs, refine their narratives, and wait for friendlier conditions.

That waiting period mattered. It forced discipline. It also created a backlog. By the time markets improved, there was a long line of companies that were bigger, older, and better prepared than the average IPO candidate from earlier cycles. Many had spent extra years improving margins, tightening governance, and proving they could survive without a permanent IV drip of cheap capital.

That is one reason today’s IPO rebound looks more durable than a sugar rush. The companies approaching the market are not showing up with a dream, a slogan, and a suspiciously optimistic slide deck. They are increasingly showing up with real revenue, clearer business models, and a more credible path to profitability.

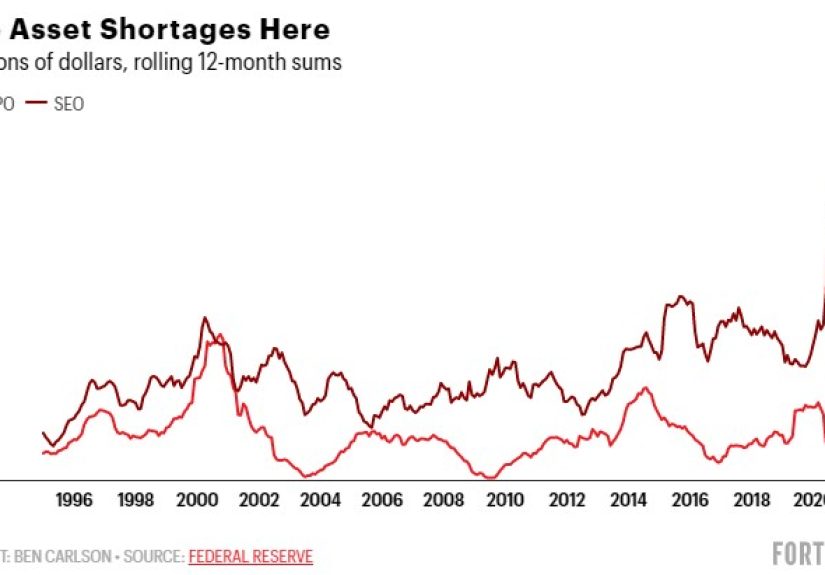

The Data Says the Market Is Back Even If the Counting Gets Weird

The strongest sign of the rebound is simple: the numbers are finally moving in the right direction. But because capital markets love complexity almost as much as they love fees, different organizations count IPOs differently.

That means several headline figures can all be true at once. Nasdaq counted 354 U.S. equity market IPOs in 2025, up sharply from 2024 and 2023. EY, using a narrower lens, counted 216 U.S. IPO deals in 2025 and roughly $47.4 billion in proceeds. SEC quarterly statistics also showed momentum building through 2025, with IPO counts rising from 84 in the first quarter to 96 in the second and 110 in the third. By late December, Reuters, citing Dealogic, reported that U.S. IPOs had raised roughly $75 billion for the year, the biggest haul since 2021.

So yes, the totals vary. No, that does not mean the rebound is fake. It means one dataset is counting a broader equity universe, another is focused on traditional offerings, and another is capturing year-end proceeds through a different methodology. Capital markets are like that. Put three bankers in a room and you may get four definitions.

What matters is the direction: activity rose, proceeds rose, and investor appetite improved.

Five Forces Driving the Rebirth of the IPO

1. Interest Rates Finally Stopped Being the Villain in Every Scene

For much of 2022 and 2023, higher rates made future earnings worth less in present terms, which hit high-growth companies especially hard. When rates began easing and expectations for a more supportive financing environment improved, IPO math started looking less painful. Companies could model better valuations. Investors could stomach growth stories again, provided those stories came with some adult supervision.

Lower rates did not create a free-for-all. They simply made public listings more plausible. That distinction matters. The market did not reopen because risk disappeared. It reopened because risk became priceable again.

2. Public Investors Wanted Better Businesses, and Private Companies Adapted

One of the biggest lessons of the IPO drought was that investors had changed. They no longer wanted “growth at all costs.” They wanted resilient revenue, stronger margins, better governance, and sensible balance sheets. Morgan Stanley and KPMG both described a market rewarding preparedness, maturity, and valuation discipline.

That has led to a more selective IPO environment. The winners tend to be companies that can explain not only how they grow, but why that growth is durable. Investors want to see customer retention, recurring revenue, pricing power, long-term contracts, cash generation, or at least a believable road map toward it. The era of “trust us, profits will arrive eventually” is no longer the default script.

3. AI Gave the Market a Fresh Story

Every IPO cycle has a theme, and in this one, artificial intelligence has been impossible to ignore. EY, Deloitte, KPMG, and Morgan Stanley all pointed to investor interest in AI infrastructure, cloud computing, semiconductors, and adjacent software as a major source of energy. That does not mean anything with “AI” in the pitch deck gets a standing ovation. It means investors have been more willing to engage with companies that fit into a credible AI buildout story.

That enthusiasm has helped re-open the market for tech, especially where the businesses are tied to real demand rather than wishful futurism. Investors may still ask hard questions, but they are at least back in the room.

4. Private Equity and Venture Capital Needed Exits

The IPO rebound is also an exit story. Private equity and venture firms have spent years waiting for better liquidity conditions. As holding periods stretched and limited partners wanted capital returned, pressure built. A functioning IPO market is not just a headline generator. It is a release valve.

McKinsey reported that IPO exit value in private equity jumped 98% in 2025, with the increase driven heavily by very large offerings. KPMG likewise noted that a reopened exit window for private equity and venture capital helped fuel the 2025 pipeline. That matters because sponsors often own some of the most IPO-ready assets in the market. Once the window opens even a little, they tend to line up at the door.

5. Valuation Discipline Made Debuts Look Better

Another reason the comeback has legs is that companies are pricing more carefully. In a buyer’s market, issuers cannot assume investors will chase anything with a ticker symbol. That has pushed companies and bankers toward more grounded pricing, often leaving room for healthy aftermarket trading.

It is not as flashy as maxing out the range and declaring victory on CNBC. But it is healthier. A stock that debuts well and trades constructively does more for market confidence than a deal that arrives overhyped and spends the next month falling down a staircase.

Proof the Comeback Is Real: Recent IPOs That Mattered

The rebound has not been theoretical. It has shown up in real offerings across tech, fintech, healthcare, and payments.

Arm’s 2023 debut helped break the psychological ice after the market’s deep freeze. In 2024, Reddit ended its first day up 48%, while Astera Labs surged as much as 76% in its Nasdaq debut, showing that public investors still had an appetite for recognizable platforms and AI-linked semiconductor stories.

Late 2024 added another signal with ServiceTitan, which priced above its expected range and raised roughly $625 million. That was not the behavior of a market shut for repairs. It was the behavior of a market slowly remembering how to function.

Then 2025 brought stronger confirmation. Chime jumped 59% in its debut. Klarna opened 30% above its IPO price in September 2025, underscoring fresh demand for fintech listings when the company, the valuation, and the timing lined up. In December 2025, Medline delivered a blockbuster result, raising about $6.26 billion in what Reuters described as the largest private-equity-backed IPO ever and the biggest global IPO of the year. That was not just a good deal. It was a statement.

Even in early 2026, the tone remained constructive. PayPay opened roughly 19% above its offer price in its March 2026 Nasdaq debut, despite a volatile geopolitical backdrop. That is important because it suggests investor appetite is not vanishing the second the macro headlines get noisy. The market may be picky, but it is not closed.

Why This Comeback Looks Better Than the Last Mania

Here is the paradox at the heart of the IPO revival: it looks healthier precisely because it is less euphoric.

The 2021 market was hot, but it was also sloppy. Too many deals got done on vibes, velocity, and the assumption that public investors would tolerate almost any narrative as long as it arrived wrapped in “disruption.” That era produced some spectacular debuts, but it also produced plenty of broken post-IPO charts and bruised confidence.

The new environment is stricter. Investors are more skeptical. Due diligence is tougher. Valuations are more grounded. Many companies are staying private longer and entering the market only after they can show stronger metrics. That makes the rebound slower, but also sturdier.

Think of it this way: the champagne is back, but it is being poured into much smaller glasses.

Who Benefits Most From the Rebirth?

The clearest winners are mature private companies that can show scale, profitability potential, and a believable reason to be public now. That includes AI infrastructure plays, enterprise software firms with sticky customers, fintechs with defensible positions, industrial and defense-related businesses with durable demand, and sponsor-backed companies that can tell a clean value-creation story.

Employees benefit too, especially at late-stage companies where equity has been locked up for years. A healthier IPO market creates more paths to liquidity, whether through the offering itself, post-lockup sales, or structured programs that allow broader employee participation.

Public investors benefit when the pipeline improves in quality. More seasoned issuers mean better chances of buying businesses built for public ownership rather than businesses simply escaping private-market fatigue.

The losers, at least for now, are weaker candidates. If a company lacks scale, still burns cash aggressively, depends on a fragile story, or wants a valuation disconnected from public comps, the window may still be closed. The market has reopened, but it did not turn into a charity.

What Could Still Derail the Momentum?

Rebirth is not the same thing as invincibility. The IPO market remains highly sensitive to volatility, policy changes, trade disruptions, and sudden risk-off sentiment. Several sources noted that 2025’s progress was interrupted by tariff-related turbulence and, later in the year, by a government shutdown that delayed some listings.

That is the biggest caveat. IPO windows do not stay open out of kindness. They stay open when equity markets are constructive, volatility is manageable, and investors believe they can make money after the bell-ringing photos are over.

So the market is back, but it is still conditional. If macro conditions worsen meaningfully, companies may delay again. If newly public stocks disappoint in a cluster, sentiment can cool fast. IPO recoveries are real, but they are rarely linear.

The Experience of the IPO Rebound: What It Feels Like on the Ground

The most interesting part of the IPO comeback may not be the statistics. It may be the mood shift inside companies preparing to go public. During the drought, the conversation inside late-stage firms often sounded cautious, defensive, and slightly exhausted. Boards asked whether an IPO was even worth the hassle. Finance teams built readiness plans that felt like emergency kits: useful to have, but maybe never needed. Employees with stock options started treating liquidity as a mythical event, somewhere between a unicorn and a functioning airport Wi-Fi connection.

That experience changed in 2025 and early 2026. Companies did not suddenly become reckless, but the tone became more practical and more hopeful. CFOs started spending time on real sequencing questions again: When should the roadshow begin? What metrics belong in the investor narrative? How much float is enough? Which investors want to learn the story early, and which ones are just sightseeing? That is a very different emotional landscape from “Let’s wait six more months and see if the market stops throwing furniture.”

For founders, the rebound has been a lesson in humility. A few years ago, many believed the public market would reward sheer top-line growth and a compelling founder aura. Today’s market has a more ruthless personality. It asks what your margins look like, how concentrated your customer base is, whether your churn is under control, and why public investors should believe this is the right moment. That can be painful, but it is also clarifying. Companies that make it through that gauntlet often emerge sharper. They know their story better because they had to earn it.

For employees, the experience is more personal. A stronger IPO market revives the old startup promise that equity might one day turn into something tangible: a down payment, student loan relief, a college fund, or simply proof that the last six years of all-hands meetings meant something. But the new era is also more measured. Employees are learning that liquidity may come in stages, not in one cinematic jackpot moment. Early-sale programs, staggered lockup releases, and broader participation structures reflect a more mature approach. Less fairy tale, more financial planning.

For investors, the comeback has felt like a return to discernment. They are not rejecting new issues. They are choosing more carefully. The excitement is real when a company has quality, but so is the punishment when it does not. That has restored a sense of consequence to the process. Good businesses can be rewarded dramatically. Weak ones can be humbled immediately. Frankly, that is how a healthy IPO market is supposed to work.

And for bankers, lawyers, and advisers, the rebound has probably felt like reentering a gym after a very long vacation. The muscles are still there, but everyone is stretching carefully. The market is active again. The pipeline is real. The meetings are back. But nobody with a memory wants to confuse “better” with “easy.” The experience of this rebound is not wild optimism. It is controlled confidence. That may not sound glamorous, but it is usually how sustainable markets begin.

Conclusion: The IPO Is Back, but in a Smarter Form

The rebirth of the IPO is not a return to the excesses of the last boom. It is something better: a reopening of the public market on stricter, more rational terms. Companies are arriving later, stronger, and more prepared. Investors are demanding better fundamentals and more realistic pricing. Private equity and venture capital finally have a more functional exit route. And a new generation of issuers, especially in AI, fintech, healthcare, and infrastructure-linked sectors, is proving that public listings can work again.

That does not mean every company should sprint toward a ticker symbol. It means the IPO is once again a viable destination, not a nostalgic memory. The market is open, but it is asking tougher questions. For the best companies, that is not a problem. It is an opportunity.

The IPO has been reborn. This time, it seems to have learned some manners.