Table of Contents >> Show >> Hide

- The Big Idea: Debt vs. Equity in One Minute

- Type 1: Debt Investment (Borrowed Money With a Schedule)

- Type 2: Equity Investment (Money for Ownership)

- Hybrid “In-Between” Investments (Because Business Can’t Resist a Combo Meal)

- How to Choose Between Debt and Equity (Without Guessing)

- Compliance Reality Check (U.S.): Equity Is Usually a “Security”

- Tax and Accounting Basics (Why Labels Matter)

- Investor Perspective: What Each Type Signals

- Common Mistakes (Learn These the Cheap Way)

- A Quick Funding Checklist (Before You Take a Dollar)

- Conclusion

- Experiences: What Small Business Owners Commonly Learn About Debt vs. Equity (Real-World Lessons)

- 1) The “Debt is cheaper!” moment… right up until the slow season

- 2) Equity feels painless… until you realize you gave away your best future years

- 3) Friends-and-family investing can be either beautiful or brutal

- 4) Crowdfunding brings capitaland a new job called “Investor Relations”

- 5) Hybrid instruments can reduce early frictionbut require future math

Every small business has the same two hobbies: (1) serving customers and (2) running out of money at the worst possible time.

When it’s time to raise capitalwhether you’re opening a second location, buying equipment, hiring help, or simply smoothing out

“why are invoices always late?” cash-flow chaosmost funding boils down to two types of investments:

debt and equity.

They both put cash into your business. They both come with strings. And they both have the power to turn a promising plan into

either a growth story… or a cautionary tale told at networking events with sad snack trays. This guide breaks down how each investment

works, when it fits best, what it costs (in dollars and/or control), and how to choose without accidentally selling your future for a

short-term boost.

Friendly note: This is general educational information, not legal, tax, or investment advice. For an actual deal, talk to a qualified attorney/accountant.

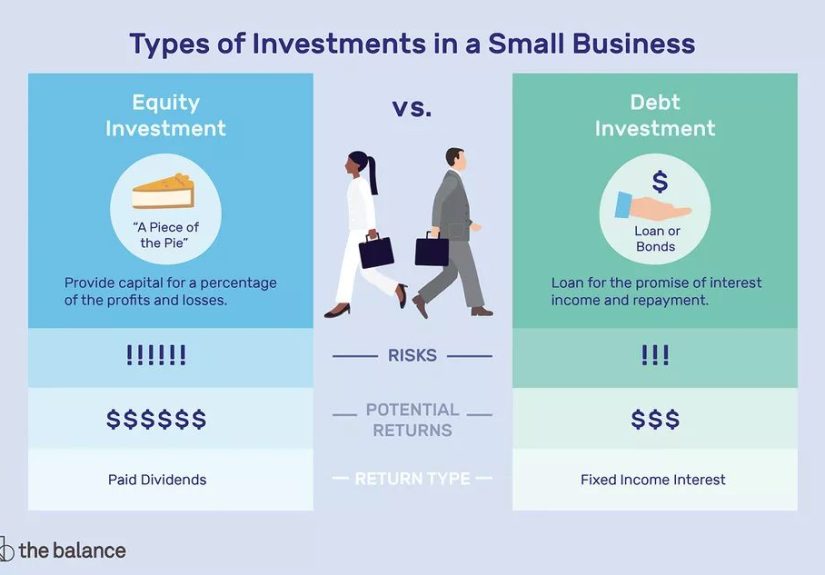

The Big Idea: Debt vs. Equity in One Minute

| Feature | Debt Investment | Equity Investment |

|---|---|---|

| What it is | Borrowed money you repay (usually with interest) | Money exchanged for ownership (shares or membership interest) |

| Typical “return” for the investor | Interest + repayment of principal | Share of future profits and/or value growth |

| Cash-flow impact | Regular payments (monthly/weekly) | No required repayment schedule |

| Control impact | Lender usually doesn’t run your business | Owners may want voting rights, info rights, or a board seat |

| Risk to business | Default risk if payments can’t be made | Dilution (you own less) + potential governance complexity |

| Best for | Predictable cash flow, assets, steady growth | High-growth bets, early-stage startups, “rocket fuel” goals |

Type 1: Debt Investment (Borrowed Money With a Schedule)

A debt investment is money your business must pay back, typically with interest, on an agreed timeline.

In plain English: someone gives you cash now, and you promise to return it laterplus a little extra for the privilege.

Common debt options for small businesses

- Term loans: Borrow a lump sum and repay over time (often monthly).

- Lines of credit: Reusable borrowing up to a limit (like a business “cash buffer”).

- Equipment financing: Loan tied to equipment that often serves as collateral.

- SBA-guaranteed loans: Bank loans backed by a government guarantee program (eligibility/use rules apply).

- Invoice factoring or receivables financing: Turn unpaid invoices into immediate cash (for a fee).

- Merchant cash advances: An advance repaid from future salesfast, but often expensive.

Why debt is attractive (when it fits)

- You keep ownership: No dilution. No new co-owner asking why you bought “fancy” chairs.

- Predictable cost: Interest and fees can be modeled if you understand the true APR.

- Cleaner governance: Lenders care about repayment, not your brand color palette.

Where debt can bite

- Payments don’t care about your slow season: Debt must be serviced even when revenue is moody.

- Collateral and guarantees: Some loans require assetsor a personal guaranteeraising personal risk.

- Covenants and restrictions: Some lenders limit additional borrowing, owner draws, or major spending.

Example: Debt used the smart way

Imagine a local coffee roaster wants to buy a $70,000 commercial roaster that boosts capacity and improves quality. If the roaster’s

existing contracts already generate stable monthly revenue, a term loan might be a great fit.

- Loan amount: $70,000

- Use: Equipment purchase (asset-backed)

- Outcome: Higher output + better margins help cover monthly payments

The key is that the roaster is financing an asset that (a) lasts and (b) generates or protects cash flow. Debt loves boring, reliable math.

The paperwork you’ll usually see with debt

- Promissory note: The repayment promise (amount, rate, schedule).

- Security agreement: Collateral terms (if secured).

- Personal guarantee: If the owner personally backs the debt.

- Loan covenants: Rules you agree to follow (reporting, ratios, restrictions).

Type 2: Equity Investment (Money for Ownership)

An equity investment means you exchange part of your business ownership for capital. Instead of a repayment schedule,

investors “get paid” through a share of future profits (sometimes) and, more often, by owning a piece of a business that becomes more valuable.

Common equity sources

- Friends and family: Common early fundingalso common early awkwardness if expectations aren’t written down.

- Angel investors: Individuals investing in exchange for equity, often at early stages.

- Venture capital: Professional funds that target high-growth businesses and typically want governance rights.

- Equity crowdfunding: Raising smaller investments from many people under specific U.S. rules.

- Strategic investors: Partners investing for synergy (distribution, supply chain, brand fit).

Why equity can be powerful

- No mandatory payments: Helpful when cash flow is unpredictable or you’re reinvesting heavily.

- Risk-sharing: If the business struggles, you’re not automatically in default the way you can be with debt.

- Often comes with expertise: The right investor may bring relationships, hiring help, or industry credibility.

Where equity gets real (fast)

- Dilution: You own less of your company after the deal.

- Control and governance: Equity can come with voting rights, veto rights, board seats, and reporting obligations.

- Long-term cost can be huge: Selling 20% early can feel “cheap” later if the company becomes valuable.

Example: Equity with simple math

A small software startup raises $300,000 at a $2,000,000 pre-money valuation. Post-money valuation becomes $2,300,000.

The investor owns roughly 13.0% post-money ($300,000 ÷ $2,300,000).

That 13% might be a fair trade if the capital helps the startup reach product-market fit and scale. But it also means the founders

permanently share future upsideso the “price” is paid in ownership, not monthly payments.

The paperwork you’ll usually see with equity

- Term sheet: The headline deal terms (valuation, investment amount, key rights).

- Stock purchase agreement / membership interest agreement: The actual purchase terms.

- Investor rights: Information rights, voting rights, protective provisions, board structure.

- Cap table updates: Ownership trackingbecause “we’ll remember who owns what” is not a strategy.

Hybrid “In-Between” Investments (Because Business Can’t Resist a Combo Meal)

Real life often blends debt and equity. Two common hybrid structures:

Convertible notes

A convertible note starts as debt and can convert into equity lateroften at a discount or with a valuation cap.

It’s popular when a company is too early to price a valuation confidently but needs capital now.

SAFEs (Simple Agreements for Future Equity)

A SAFE isn’t debt in the classic sense (no interest and no maturity date like a typical loan), but it can convert to equity later.

Terms vary by deal, and the trade-offs still revolve around dilution and future ownership.

Hybrids can reduce early negotiation frictionbut they can also create “surprise dilution” later if founders don’t model outcomes.

Translation: you can’t ignore the cap table just because it’s wearing a trench coat.

How to Choose Between Debt and Equity (Without Guessing)

The right type depends less on what sounds cool at brunch and more on your business fundamentals. Here’s a practical framework.

Choose debt when…

- You have predictable cash flow and can comfortably make payments even in slower months.

- You’re financing assets (equipment, vehicles, inventory) that support revenue generation.

- You want to keep ownership and control tightly held.

- Your growth plan is steady and you don’t need “hypergrowth” capital.

Choose equity when…

- Cash flow is uncertain and you can’t safely commit to fixed payments.

- You’re aiming for rapid growth that requires upfront hiring, R&D, or aggressive marketing.

- The business value could increase dramatically with the right funding and support.

- You want strategic partners who can help you scale (not just a check).

Many healthy businesses use both

It’s common to use equity early (when risk is high and cash flow is light) and add debt later (when revenue becomes stable).

Think of equity as “risk capital” and debt as “efficient capital” once the business can support it.

Compliance Reality Check (U.S.): Equity Is Usually a “Security”

In the U.S., selling ownership interests typically involves securities laws. That doesn’t mean you can’t raise equity;

it means you should do it correctlyoften through an exemption pathway and with proper disclosures and documentation.

Equity crowdfunding, private placements, and other exempt offerings have specific rules. The takeaway is simple:

don’t wing it. If you’re taking equity investment, talk to a securities attorneyespecially if you’re raising from multiple people.

Tax and Accounting Basics (Why Labels Matter)

Debt and equity aren’t just different feelingsthey can be treated differently for tax and accounting purposes.

Generally, interest on business debt may be deductible, but limitations can apply depending on business structure and circumstances.

Equity payments (like dividends or distributions) are typically not treated the same way as interest.

Also, the line between “debt” and “equity” can get blurry with unusual instruments or poorly documented “loans” from owners.

The safer route is clear paperwork, reasonable terms, and professional guidanceespecially when owners are lending money to their own company.

Investor Perspective: What Each Type Signals

Debt investors usually want predictability

Lenders generally look for repayment ability, collateral, and risk controls. Their upside is limited to interest and fees,

so their main goal is not losing money. (Wild concept, right?)

Equity investors usually want upside

Equity investors accept higher risk in exchange for potentially bigger returns if the business grows. They care about market size,

unit economics, team strength, and exit possibilities (selling the company, buybacks, dividends, etc.).

Common Mistakes (Learn These the Cheap Way)

- Using short-term, high-cost financing for long-term problems: If your business model is broken, expensive capital won’t fix it.

- Underestimating cash-flow pressure: Debt payments can turn “slow month” into “panic month.”

- Messy equity from friends/family: Vague promises lead to future conflictwrite it down.

- Ignoring control terms: A small equity check can still come with big veto rights.

- Not modeling dilution: Convertibles and SAFEs can surprise founders later.

- Failing to align expectations: Some investors want quick returns; others want long-term growth. Mismatch = friction.

A Quick Funding Checklist (Before You Take a Dollar)

- Can the business afford payments in a worst-case “bad quarter” scenario?

- What exactly is being fundedassets, inventory, hiring, marketing, runway?

- What’s the true cost (APR/fees for debt; dilution/control for equity)?

- What happens if the plan underperformsdefault risk or dilution risk?

- Is the paperwork clear and professional (and reviewed by pros)?

- Do you understand your cap table after the deal (and after future rounds)?

Conclusion

The two primary investment types in a small businessdebt and equitysolve the same problem (capital needs)

with very different trade-offs. Debt is structured, repayment-driven, and ownership-preservinggreat for stable cash flow and asset-backed growth.

Equity is flexible, risk-sharing, and often growth-fueledgreat for early-stage uncertainty and ambitious expansion, but it costs ownership and can

reshape control.

A smart funding decision isn’t about choosing the “best” type in generalit’s about choosing the right match for your cash flow, growth pace,

risk tolerance, and long-term goals. When in doubt: model the numbers, pressure-test your assumptions, and get professional help before you sign.

Your future self will thank you (and will stop stress-refreshing your bank account app).

Experiences: What Small Business Owners Commonly Learn About Debt vs. Equity (Real-World Lessons)

You can read a thousand explainers and still learn the most from what actually happens when money hits your bank accountand then leaves it.

Below are common real-world experiences founders and small business owners report when they use debt and equity. These are composite scenarios

drawn from typical patterns, not one specific company.

1) The “Debt is cheaper!” moment… right up until the slow season

Owners often choose debt because it feels straightforward: borrow, build, repay, done. The surprise comes when revenue dips.

A landscaping business, for example, might take a loan in spring to buy a truck and equipment, expecting summer sales to cover payments.

If weather, staffing issues, or client delays hit, the payments still show up on schedule. Many owners learn to build a “payment buffer”

(cash reserves for 2–3 months of payments) before taking on debtor they structure debt so the payment schedule matches the seasonality

of the business.

2) Equity feels painless… until you realize you gave away your best future years

Equity can feel like a relief: no monthly payments and room to reinvest. The hard lesson often arrives later, when the business becomes meaningfully

profitable. A retail brand might raise $250,000 for 25% early on, then grow into a business throwing off strong cash every year. At that point,

the “cheap” equity ends up being expensive because the company is now sharing profits indefinitelyor negotiating a buyback at a high valuation.

Owners often learn to raise only what they need, plan milestones carefully, and consider whether a smaller roundor a hybrid instrumentcould reduce

long-term dilution.

3) Friends-and-family investing can be either beautiful or brutal

Many small businesses start with friends-and-family funding. The experience is often positive when expectations are crystal clear:

Is this a loan with interest? An equity stake? A gift? A convertible note? The brutal version happens when it’s “sort of an investment”

with no documents. Years later, when the business is doing well (or struggling), misunderstandings appear. A common lesson is that the relationship

needs protection too: written terms, realistic timelines, and clear communication prevent the Thanksgiving-table negotiation nobody asked for.

4) Crowdfunding brings capitaland a new job called “Investor Relations”

Equity crowdfunding can be a powerful way to raise money and build a community of customers who are literally invested. The experience many founders

share is that it also increases communication duties: updates, reporting, and answering questions from a large group of small investors.

The upside is a marketing flywheel and customer loyalty; the downside is time and administrative complexity. Founders who thrive here build a simple,

consistent update cadence and invest early in clean bookkeeping so reporting isn’t a last-minute scramble.

5) Hybrid instruments can reduce early frictionbut require future math

Convertibles and SAFEs often feel like the “easy button” early on. The common experience is that they delay the hard conversation about valuation,

which is convenientuntil conversion. Later, when a priced equity round happens, founders may discover they’re giving up more ownership than expected

because multiple notes convert at once, each with caps and discounts. The founders who avoid the shock model multiple scenarios before signing:

“What happens if we raise at a $3M valuation? $6M? What if we raise less than planned?” The lesson is simple: hybrids still affect ownership, just on

a different timetable.

Across all these experiences, one theme repeats: capital doesn’t just fund growthit changes the rules of your business. Debt changes your cash-flow

obligations; equity changes your ownership and governance. The “best” choice is the one you can live with in both a great outcome and a messy one.