Table of Contents >> Show >> Hide

- Why SaaS Startups Are Valued on Revenue Multiples

- The 6x-25x Revenue Range Explained

- The Metrics That Move SaaS Valuation Multiples

- Public Market Multiples vs. Private SaaS Valuations

- Why Some SaaS Startups Get 25x While Others Get 6x

- AI’s Impact on SaaS Startup Valuations

- How to Increase Your SaaS Valuation Multiple

- Founder Experiences: Lessons From the Valuation Conversation

- Conclusion

If you ask three investors what your SaaS startup is worth, you may get five answers, two spreadsheets, and one dramatic pause. Welcome to SaaS valuation, where the same company can look “reasonably priced” at 6x revenue, “strategic” at 12x, and “someone brought very expensive coffee to the board meeting” at 25x.

The frustrating truth is also the useful truth: SaaS valuation multiples are not magic numbers. They are shorthand for how the market prices growth, retention, profitability, risk, category leadership, and future optionality. A startup doing $5 million in ARR with weak retention and slow expansion is not valued like a startup doing $5 million in ARR with 120% net revenue retention, 80% gross margins, and a product customers treat like oxygen.

So, what is your SaaS startup worth? The answer often falls somewhere between 6x and 25x revenue, but the real work is understanding which end of the range you deserveand why.

Why SaaS Startups Are Valued on Revenue Multiples

SaaS companies are usually valued on ARR or revenue multiples because their economics can scale beautifully once the engine works. Subscription revenue is recurring, gross margins are often high, and the best SaaS companies can expand customer accounts over time without reselling from scratch every month.

That is why investors often look beyond current profit. A fast-growing SaaS company may be intentionally spending heavily on sales, marketing, engineering, and customer success. On paper, it might look unprofitable. In reality, it could be building a compounding revenue machine.

ARR vs. Revenue: What Buyers Actually Mean

When people say a SaaS startup is worth “10x revenue,” they often mean 10x annual recurring revenue, or ARR. ARR is the annualized value of recurring subscription contracts. It excludes one-time setup fees, consulting projects, hardware, and other revenue that does not reliably repeat.

For example, if your company has $3 million in ARR and buyers assign a 10x multiple, the enterprise value might land near $30 million. If your company has $3 million in total revenue but only $1.8 million is recurring, the valuation conversation will probably get less glamorous very quickly. Investors like recurring revenue. They are less excited about “we did a giant custom integration once and everyone cried but paid us.”

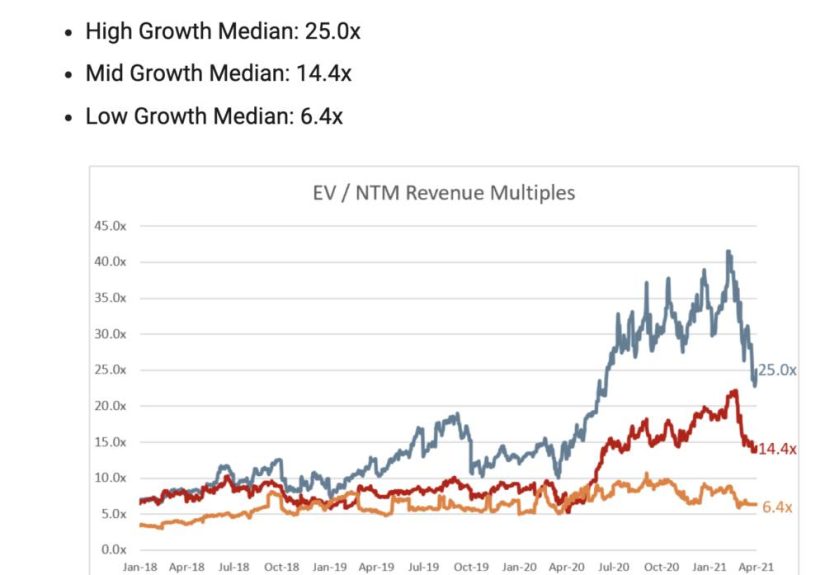

The 6x-25x Revenue Range Explained

A 6x to 25x revenue range sounds absurdly wide until you break it into quality bands. SaaS multiples are not randomly assigned by a mysterious spreadsheet goblin. They reflect how predictable, efficient, and defensible the business appears.

6x-8x Revenue: Solid, But Not Yet Premium

A SaaS company in the 6x-8x range may be healthy, but it usually has at least one meaningful constraint. Growth might be moderate. Net revenue retention may be average. The market might be competitive. The company may depend on founder-led sales. Or perhaps the product is useful but not deeply embedded in the customer’s workflow.

This range is not an insult. Many good businesses live here. A company growing 20% annually with decent margins and loyal customers can still create a strong outcome for founders. But investors generally reserve higher multiples for companies that show stronger signs of breakout potential.

9x-12x Revenue: Strong SaaS Fundamentals

The 9x-12x range is where the business starts to look more exciting. Growth is stronger, churn is under control, gross margins are attractive, and customers are expanding. The company may have a clear ideal customer profile, a repeatable sales motion, and evidence that the market is pulling the product forward.

At this level, buyers are not just purchasing today’s ARR. They are buying confidence. They believe the company can keep growing without needing to reinvent itself every quarter. The board meetings may still include tension, but fewer people are whispering, “What exactly does our sales team do again?”

13x-18x Revenue: Category Leader Potential

Companies in this range usually have a compelling combination of growth, retention, market size, and strategic importance. They may be category leaders in a niche, expanding into adjacent markets, or becoming essential infrastructure for a specific type of customer.

These companies often have strong net revenue retention, efficient customer acquisition, and credible expansion paths. They do not merely sell software; they become part of the customer’s operating system. When customers say, “We cannot run the business without this,” valuation multiples tend to perk up like a golden retriever hearing the word “walk.”

19x-25x Revenue: Rare Air

A 19x-25x revenue multiple is not normal. It is earned by companies with exceptional growth, elite retention, major market potential, and a credible claim to category dominance. These startups often have a “why now” tailwind, such as AI adoption, regulatory change, workflow automation, security urgency, or a massive shift in how businesses operate.

At this level, investors are pricing the company not only on what it is, but on what it could become. That is powerfuland dangerous. A premium valuation creates high expectations. If growth slows, churn rises, or competitors catch up, the same valuation that looked heroic can suddenly look like a very expensive hat on a very confused horse.

The Metrics That Move SaaS Valuation Multiples

Revenue is the starting point. The multiple is the story. Two SaaS startups with the same ARR can receive wildly different valuations because the quality of that ARR is different.

1. Revenue Growth Rate

Growth is still the main character in SaaS valuation. A company growing 70% annually will usually command a higher multiple than a company growing 15%, assuming retention and margins are not falling apart behind the curtain.

Growth tells buyers that the market wants what you sell. It also suggests that future revenue may be much larger than current revenue. However, not all growth is equal. Growth fueled by heavy discounts, weak-fit customers, or unsustainable ad spending is less valuable than growth driven by strong product-market fit and repeatable sales execution.

2. Net Revenue Retention

Net revenue retention, or NRR, measures how much revenue existing customers generate after expansion, contraction, and churn. If your NRR is above 100%, your existing customer base is growing even before you add new logos.

This is one of the most powerful valuation signals in SaaS. High NRR means customers stay, spend more, and deepen their relationship with the product. It also reduces pressure on new customer acquisition. If your customers expand every year, your growth engine gets a built-in tailwind. If they churn like they are escaping a haunted house, buyers will notice.

3. Gross Revenue Retention

Gross revenue retention shows how much recurring revenue remains before upsells and expansion. It answers a brutally simple question: do customers stay?

A company can have decent NRR because expansion from happy customers offsets churn from unhappy ones. That may work for a while, but buyers will still inspect gross retention closely. Strong gross retention suggests the product solves a durable problem. Weak gross retention suggests the company is constantly refilling a leaky bucket, which is exhausting and not particularly glamorous.

4. Gross Margin

Gross margin matters because SaaS valuation depends on scalability. A classic software company with 75%-85% gross margins has room to invest in sales, marketing, product, and support. A company with lower margins may still be valuable, especially if it includes services, AI compute, or payments revenue, but buyers will ask whether margins can improve over time.

AI has made this conversation more interesting. Some AI-enabled SaaS businesses grow quickly but carry higher infrastructure costs. Investors may love the growth but still ask whether the company can deliver software-like margins at scale. Translation: “Your demo is magical, but does every customer interaction require a bonfire made of GPU invoices?”

5. Sales Efficiency and CAC Payback

Customer acquisition cost, or CAC, is the money spent to acquire new customers. CAC payback measures how long it takes to recover that cost through gross profit. Shorter payback periods usually improve valuation because they show the company can reinvest capital efficiently.

A startup with a 10-month CAC payback can often grow faster with less dilution than one with a 30-month payback. Investors like growth, but they love efficient growth. Buying revenue at any cost is not a strategy. It is a very expensive hobby.

6. Rule of 40

The Rule of 40 combines revenue growth rate and profit margin. A SaaS company growing 30% with a 10% profit margin has a Rule of 40 score of 40. A company growing 60% while losing 20% also scores 40.

This metric helps investors compare different operating profiles. Younger companies may prioritize growth. Mature companies may emphasize profitability. The best companies balance both. The Rule of 40 is not perfect, and people debate how profitability should be measured, but it remains a useful lens for evaluating SaaS health.

Public Market Multiples vs. Private SaaS Valuations

Founders often look at public SaaS companies and try to apply those multiples directly to private startups. That can be helpful, but only as a reference point. Public companies are larger, more liquid, more transparent, and easier to compare. Private companies are riskier and less liquid, so buyers usually apply discounts unless the startup is growing much faster or sits in a strategically hot category.

During frothy markets, private valuations may outrun public comparables. During tighter markets, public multiples often pull private valuations back toward earth. This is why a valuation that felt “obvious” one year may feel ambitious the next. The business may be better, but the market’s appetite may have changed.

Why Some SaaS Startups Get 25x While Others Get 6x

The difference is rarely one metric. It is the full pattern. A 25x SaaS startup usually checks several boxes at once: fast growth, high retention, massive market, strong margins, low churn, differentiated product, and a credible path to becoming much larger.

A 6x SaaS startup may still be a great business, but it may lack breakout characteristics. Perhaps it serves a smaller market. Perhaps growth is steady but not spectacular. Perhaps customers like the product but do not expand usage. Perhaps the company relies on services-heavy implementation. Each of these factors can compress the multiple.

Example: Two Companies, Same ARR, Different Worlds

Imagine two SaaS companies with $10 million in ARR.

Company A is growing 18% annually, has 92% gross revenue retention, 103% net revenue retention, and 68% gross margins. It sells into a competitive market and requires significant onboarding services. A buyer might value it around 6x-8x ARR, or $60 million to $80 million.

Company B is growing 65% annually, has 96% gross revenue retention, 122% net revenue retention, 82% gross margins, and a strong AI-enabled workflow advantage in a large market. A buyer might consider 15x-20x ARR, or $150 million to $200 million. If strategic interest is intense, the multiple could stretch higher.

Same ARR. Completely different valuation story.

AI’s Impact on SaaS Startup Valuations

AI has created both valuation premiums and valuation anxiety. On one side, AI-native startups can grow faster, automate complex workflows, and attack markets that once seemed too labor-intensive for software. On the other side, AI can weaken traditional SaaS moats by making it easier to build features, switch vendors, or replace point solutions.

For founders, the key is proving that AI improves the business model, not just the pitch deck. Does AI increase customer value? Does it improve retention? Does it create proprietary data advantages? Does it lower service costs? Does it support usage-based expansion? Or is it just a chatbot wearing a tiny SaaS-branded cape?

Buyers are increasingly separating real AI leverage from AI decoration. The first can increase multiples. The second may briefly impress a demo audience before everyone returns to asking about churn.

How to Increase Your SaaS Valuation Multiple

You cannot control the entire market, but you can improve the story your metrics tell. The goal is to make your revenue more durable, more scalable, and more valuable.

Focus on Retention Before You Chase Growth

Growth with weak retention is like filling a bathtub with the drain open. It looks exciting until someone checks the water level. Improving onboarding, customer success, product adoption, and support quality can lift both gross retention and net revenue retention.

Build a Repeatable Sales Motion

Founder-led sales can get a company started, but buyers want to know whether the machine works without the founder personally charming every prospect. Document the sales process, define your ideal customer profile, track conversion rates, and prove that new reps can become productive.

Improve Gross Margins

Review hosting costs, support load, implementation work, and service delivery. If your product requires too much manual effort, margins may stay compressed. Automating onboarding, improving self-service features, and reducing custom work can make revenue more scalable.

Show Expansion Paths

Premium SaaS businesses often expand through additional seats, usage, modules, data products, integrations, or higher-tier plans. If customers can grow inside your platform, buyers can underwrite future revenue more confidently.

Know Your Category Narrative

Valuation is partly financial and partly narrative. Are you a niche workflow tool, a vertical operating system, a compliance platform, an AI automation layer, or a mission-critical system of record? The clearer your category story, the easier it is for investors and acquirers to understand why your company deserves a premium.

Founder Experiences: Lessons From the Valuation Conversation

The first experience every SaaS founder should expect is this: investors will admire your growth, then immediately ask how expensive it was. A pretty ARR chart is wonderful, but it becomes much less charming if every dollar of new ARR requires a suitcase of cash and three heroic salespeople sprinting through airports.

One common founder mistake is treating valuation as a scoreboard instead of a financing tool. A higher valuation feels great, especially when announced in a press release with dramatic words like “accelerate,” “transform,” and “delighted.” But a valuation that is too high can become a trap. If the company does not grow into it, the next round becomes painful. Down rounds, flat rounds, heavy preferences, and awkward board conversations can follow. The goal is not to win the valuation headline. The goal is to raise capital on terms that help the company build long-term value.

Another lesson: buyers and investors do not only evaluate the numbers; they evaluate the reliability of the numbers. Clean revenue recognition, accurate cohort data, clear churn definitions, and trustworthy pipeline reporting matter. If your metrics require a 45-minute explanation and a spiritual interpretation, the buyer may discount them. Good finance hygiene can lift confidence, and confidence can lift multiples.

Founders also learn that not all ARR is equally lovable. Enterprise ARR with multi-year contracts, strong retention, and expansion potential generally receives more credit than fragile SMB revenue with high churn. That does not mean SMB SaaS is bad. It means the motion must be understood. A high-volume, low-touch SMB model can be excellent if acquisition is efficient and churn is predictable. The danger is pretending one model behaves like another.

There is also a timing lesson. Valuation depends on market cycles. In hot markets, buyers may pay aggressively for growth. In cautious markets, they ask harder questions about profitability, retention, and cash burn. A founder cannot control interest rates, public market sentiment, or whether the phrase “AI agent” causes investors to levitate that quarter. But founders can control operational discipline. Companies with strong fundamentals survive valuation mood swings better than companies built purely for the trend of the moment.

Finally, founders should remember that strategic value can exceed financial value. A startup might be worth 8x revenue to a financial buyer but 15x to a strategic acquirer if it fills a product gap, protects a market position, or unlocks a new customer segment. Strategic premiums are real, but they are not guaranteed. They usually appear when the acquirer has urgency, the product is hard to replicate, and the startup has proof that customers care.

The best practical advice is simple: build the business you would want to buy. Make revenue recurring. Keep customers. Expand accounts. Improve margins. Understand your unit economics. Reduce dependency on heroic individuals. Tell a clear market story. Then, when someone asks what your SaaS startup is worth, you can answer with more than a shrug and a suspiciously colorful spreadsheet.

Conclusion

A SaaS startup can be worth 6x revenue, 25x revenue, or somewhere in the beautifully chaotic middle. The multiple depends on growth, retention, gross margins, sales efficiency, profitability, market size, strategic relevance, and the buyer’s belief in your future. Revenue gets you into the conversation. Revenue quality determines whether the conversation ends with a polite nod or a premium term sheet.

If you want a higher SaaS valuation, do not chase the multiple directly. Improve the machine behind it. Build a product customers keep, expand, and recommend. Create a repeatable go-to-market motion. Protect margins. Show a credible path to durable growth. In other words, make the business easier to believe in. Valuation follows belief, and belief follows evidence.

Note: This article is for educational and editorial purposes only. SaaS valuation ranges vary by market conditions, company stage, buyer type, sector, financial profile, and deal structure.