Table of Contents >> Show >> Hide

- Why Your Down Payment Should Be Saved Differently

- Best Places To Save For A Down Payment

- Where You Probably Should Not Keep Your Down Payment

- How To Choose The Right Account Based On Your Timeline

- How Much Should You Save For A Down Payment?

- Do Not Forget Closing Costs

- Should You Use Retirement Money For A Down Payment?

- How To Make Your Down Payment Savings Grow Faster

- Real-Life Example: Choosing The Right Place To Save

- Experience-Based Tips For Saving A Down Payment

- Conclusion: So, Where Should You Save For Your Down Payment?

Saving for a home down payment can feel like trying to fill a swimming pool with a coffee mug. You add a little money, the market changes, home prices wiggle around, and suddenly your “almost there” fund looks like it needs a protein shake. The good news is that the place where you save your down payment can make a real difference. The even better news? You do not need to become a Wall Street wizard, memorize bond charts, or start talking about “liquidity” at dinner parties unless you want everyone to mysteriously leave the room.

The best place to save for a down payment depends on three big things: when you plan to buy, how much risk you can tolerate, and how quickly you need access to your money. A down payment is not ordinary savings. It is future house money. That means it should be protected, easy to access when closing day arrives, and earning as much interest as reasonably possible without exposing it to wild market swings.

In simple terms, your down payment should usually live somewhere boring. Beautifully boring. The kind of boring that does not lose 20% of its value right before you find the perfect kitchen island.

Why Your Down Payment Should Be Saved Differently

A down payment has a deadline. Retirement money may have decades to ride out the stock market. A vacation fund may be flexible. But a down payment often needs to be ready on a specific timeline, especially once you start making offers, scheduling inspections, and preparing for closing costs.

That deadline changes everything. If you are planning to buy within the next one to three years, safety and access usually matter more than chasing the highest possible return. Yes, earning more interest is nice. Nobody has ever complained, “Oh no, my money made too much money.” But losing principal right before applying for a mortgage is a much bigger problem than missing out on a slightly higher yield.

Best Places To Save For A Down Payment

1. High-Yield Savings Account

For most future homebuyers, a high-yield savings account is the simplest and most practical place to keep down payment savings. It works like a regular savings account, but it typically pays a much better interest rate than a traditional brick-and-mortar bank account.

The biggest advantage is flexibility. You can add money regularly, transfer funds when needed, and keep your cash separate from everyday spending. That last part matters. If your down payment sits in the same checking account you use for groceries, gas, subscriptions, and “just one little online order,” your money may slowly disappear like socks in a dryer.

Look for a high-yield savings account that is FDIC-insured if it is at a bank or NCUA-insured if it is at a credit union. This helps protect your money within federal insurance limits. Also check for monthly fees, minimum balance requirements, transfer rules, and whether the advertised rate is promotional or ongoing.

Best for: Buyers planning to purchase within one to three years who want safety, easy access, and steady interest.

2. Money Market Account

A money market account can be another strong option for saving a down payment. It is similar to a savings account but may offer check-writing privileges, debit access, or higher rates depending on the institution.

This can be helpful when you are getting closer to buying and may need to move money for earnest money deposits, inspections, appraisals, or closing costs. However, not all money market accounts are created equal. Some pay excellent rates, while others are basically regular savings accounts wearing a fancier hat.

Before opening one, compare the annual percentage yield, minimum deposit, fees, and access rules. Make sure the account is insured through an eligible bank or credit union. A money market account should help your down payment grow, not charge tiny fees until your dream-home fund develops a mysterious limp.

Best for: Savers who want a safe account with strong liquidity and possibly easier access than a standard savings account.

3. Certificate of Deposit

A certificate of deposit, or CD, can be useful if you know your buying timeline. With a CD, you lock up your money for a set term, such as six months, one year, or two years, in exchange for a fixed interest rate. The benefit is predictability. You know what rate you are getting, and your money is not exposed to stock market volatility.

The downside is access. If you withdraw early, you may pay a penalty. That does not mean CDs are bad. It simply means they work best when matched carefully to your homebuying schedule. For example, if you plan to buy in 18 months, you might use a 12-month CD for part of your savings and keep the rest in a high-yield savings account.

A CD ladder can also work. That means splitting your money into several CDs with different maturity dates. This gives you some interest-rate benefits while keeping portions of your cash available at different times.

Best for: Buyers with a clear timeline who want a fixed rate and do not need immediate access to all their savings.

4. Treasury Bills

Treasury bills, often called T-bills, are short-term U.S. government securities. They are commonly available in terms such as four weeks, eight weeks, thirteen weeks, twenty-six weeks, and fifty-two weeks. They are backed by the U.S. government and can be a conservative place to park short-term savings.

T-bills may be appealing when rates are competitive and you are comfortable buying through TreasuryDirect or a brokerage account. However, they require more attention than a savings account. You need to understand maturity dates, reinvestment options, and how quickly you can access your money if your homebuying timeline changes.

For someone who enjoys spreadsheets, T-bills may feel elegant. For someone who thinks “maturity date” sounds like a personality test, a high-yield savings account may be easier.

Best for: Organized savers who want a conservative short-term option and are comfortable managing maturity dates.

5. Series I Savings Bonds

Series I savings bonds are designed to help protect savings from inflation because their rate includes an inflation-based component. They can be attractive in certain environments, but they are not perfect for every down payment plan.

The biggest issue is timing. I bonds generally cannot be redeemed during the first twelve months. If you redeem them before five years, you may give up the last three months of interest. That makes them a better fit for people with a longer timeline and a clear understanding of the rules.

If you might buy a home within the next year, I bonds are usually too restrictive. Your dream home will not wait politely while your savings bond becomes available.

Best for: Savers with a timeline longer than one year who want inflation-linked savings and understand redemption rules.

Where You Probably Should Not Keep Your Down Payment

The Stock Market

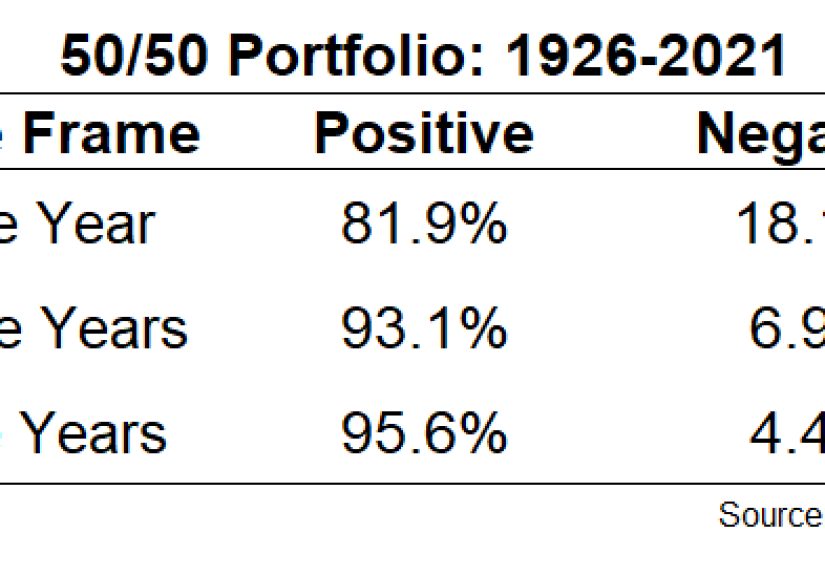

The stock market can be excellent for long-term wealth building, but it is usually not the best home for short-term down payment savings. Stocks, index funds, and ETFs can fall sharply in value. If that happens right before you need to buy, you may have to delay your purchase or sell at a loss.

If your homebuying timeline is five or more years away, investing part of your down payment fund may be reasonable depending on your risk tolerance. But if you are planning to buy soon, the market can be too unpredictable. A down payment should not need emotional support every time the market has a bad Tuesday.

Crypto or Speculative Investments

Cryptocurrency and speculative investments are generally too volatile for down payment savings. The potential for gains may look exciting, but the risk of losing a large portion of your money is real. Your down payment is not the place to gamble on dramatic price swings.

If you want to invest in speculative assets, keep that separate from the money you need for a home purchase. A house fund should be stable. It should not behave like a roller coaster operated by a raccoon.

Cash at Home

Keeping cash at home may feel simple, but it is risky. Cash can be lost, stolen, damaged, or spent too easily. It also does not earn interest and may be harder to document for mortgage underwriting. Lenders typically want to see clear records showing where your funds came from. A shoebox under the bed is not exactly a financial institution, no matter how confident the shoebox looks.

How To Choose The Right Account Based On Your Timeline

If You Plan To Buy Within 12 Months

Focus on safety and liquidity. A high-yield savings account or insured money market account is usually the strongest choice. You want your money available when you need it, especially once you are actively touring homes or preparing to make offers.

At this stage, avoid locking up too much money in long-term CDs or bonds. You may need funds quickly for earnest money, inspections, appraisal fees, or closing costs. A slightly lower return is acceptable if it keeps your money flexible.

If You Plan To Buy In 1 To 3 Years

You have more room to optimize. A combination approach can work well. Keep part of your money in a high-yield savings account for flexibility and place another portion in CDs or Treasury bills that mature before your target purchase date.

This gives you a balance of safety, interest, and access. It also prevents you from having all your money locked away when the right house appears sooner than expected.

If You Plan To Buy In 3 To 5 Years

With a longer timeline, you may consider a mix of safe cash products and conservative investments. However, be careful. The closer you get to your buying date, the more you should shift toward safer options.

For example, someone saving for a home in five years might invest a small portion early on, then gradually move the money into cash, CDs, or Treasury bills as the purchase date approaches. This reduces the chance of being forced to sell investments during a downturn.

How Much Should You Save For A Down Payment?

The old rule says you need 20% down, but that is not always true. Many buyers purchase homes with smaller down payments. Some conventional loan programs allow eligible buyers to put as little as 3% down, while FHA loans may allow qualified borrowers to put down as little as 3.5%. Some VA and USDA loans may require no down payment for eligible borrowers.

That said, saving more can still help. A larger down payment may lower your monthly mortgage payment, reduce interest costs, improve your offer strength, and help you avoid or reduce mortgage insurance. But saving forever has a cost too. If home prices rise faster than your savings, waiting for the perfect 20% may not always be the best move.

A practical target is to estimate your likely home price, minimum down payment, closing costs, moving expenses, and emergency fund. Do not empty your entire life into the down payment. Becoming a homeowner with zero backup cash is like buying a boat and forgetting water exists.

Do Not Forget Closing Costs

Your down payment is not the only cash you need. Closing costs can include lender fees, appraisal fees, title insurance, escrow costs, prepaid taxes, homeowners insurance, and other expenses. These costs commonly add thousands of dollars to the amount you need at closing.

A smart savings plan separates your money into categories: down payment, closing costs, moving costs, repair fund, and emergency fund. This makes the goal more realistic. It also prevents the unpleasant surprise of thinking you saved enough, only to discover the closing table brought friends.

Should You Use Retirement Money For A Down Payment?

Some buyers consider using retirement funds for a first home. In certain cases, qualified first-time homebuyers may be able to use up to $10,000 from an IRA without the 10% early withdrawal penalty, though regular income taxes may still apply depending on the account type and situation.

However, using retirement money should be approached carefully. That money is designed for your future. Pulling it out may reduce long-term growth, affect taxes, and create financial stress later. A home can build wealth, but it should not completely hijack your retirement plan.

Before using retirement funds, talk with a tax professional or financial advisor. The rules can be complicated, and mistakes may be expensive.

How To Make Your Down Payment Savings Grow Faster

Automate Your Savings

Automation is one of the best tools for saving a down payment. Set up an automatic transfer from checking to your down payment account every payday. Treat it like a bill. The only difference is that this bill pays Future You, who will hopefully be standing in a kitchen saying, “I cannot believe we own a garbage disposal now.”

Name The Account

Many banks allow you to nickname accounts. Instead of calling it “Savings,” name it “House Down Payment” or “Future Home Fund.” This small trick makes the goal more emotional and harder to raid for random purchases.

Save Windfalls

Tax refunds, work bonuses, cash gifts, side income, and refunds can speed up your progress. You do not need to save every extra dollar, but putting a large percentage toward your down payment can move the goal closer without changing your daily budget too much.

Cut The Big Leaks

Small savings help, but big recurring expenses matter more. Review subscriptions, insurance premiums, car costs, dining out, and housing expenses. A $15 subscription is not nothing, but refinancing a high-interest debt or reducing a major monthly cost can create much bigger savings momentum.

Real-Life Example: Choosing The Right Place To Save

Imagine a buyer named Sarah who wants to buy a $350,000 home in about two years. She hopes to save $25,000 for a down payment and another $10,000 for closing costs and moving expenses. She already has $12,000 saved.

Sarah might keep $5,000 in a high-yield savings account for flexibility, place $5,000 in a 12-month CD, and put $2,000 in a money market account. Each payday, she automatically adds money to the high-yield savings account. When the CD matures, she can decide whether to renew it, move it into savings, or use a shorter-term CD depending on how close she is to buying.

This plan is not flashy. It will not impress anyone on a finance podcast. But it protects her principal, earns interest, and keeps her money available before she needs it. For a down payment, that is exactly the point.

Experience-Based Tips For Saving A Down Payment

One of the most useful lessons about saving for a down payment is that motivation comes and goes, but systems keep working. At the beginning, saving can feel exciting. You open the account, create the spreadsheet, imagine the front porch, and maybe even start mentally placing furniture in a home you have not bought yet. Then real life shows up. The car needs tires. Rent increases. A friend plans a destination wedding. Suddenly, the down payment fund looks less like a dream and more like a very demanding house-shaped piggy bank.

This is why the best down payment strategy is not only about choosing the right account. It is about building a system you can live with. A high-yield savings account is helpful, but the habit of funding it consistently matters even more. The account is the bucket. Your behavior is the faucet.

A practical approach is to create a “down payment rule” for yourself. For example, you might decide that 15% of every paycheck goes directly into your house fund. You might also send 50% of any bonus, tax refund, or side income into the account. This gives you structure without making your life miserable. Saving for a house should require discipline, not a lifestyle where you stare sadly at a restaurant menu and order tap water with emotional damage.

Another helpful experience is keeping your down payment separate from your emergency fund. It is tempting to look at one big savings balance and feel rich. But money without labels can cause confusion. If you have $30,000 saved but $10,000 is your emergency fund, $5,000 is for closing costs, and $3,000 is for moving and repairs, your actual down payment is not $30,000. Clear labels prevent accidental overconfidence.

It also helps to review your progress monthly, not daily. Checking your down payment account every morning will not make it grow faster. It may only make you impatient. A monthly review is enough to track deposits, compare rates, adjust your target, and celebrate progress. Homebuying is already emotional. Your savings plan should not become another full-time drama series.

Many buyers also underestimate the power of staying flexible. You may start with a goal of buying in two years, then realize you need three. Or you may find the right home earlier than expected. Because life does not always follow the spreadsheet, keeping at least part of your down payment in a liquid account is wise. CDs and Treasury bills can be useful, but do not lock up every dollar unless you are very confident about your timeline.

Finally, remember that the “perfect” down payment account does not exist. Rates change. Banks update offers. Your timeline may shift. The goal is not perfection; the goal is progress with protection. Choose a safe, insured, accessible place for your money, automate your savings, avoid unnecessary risk, and keep your homebuying fund clearly separated from everyday spending. That combination may not sound glamorous, but neither does a smoke detector, and both can save you from disaster.

Conclusion: So, Where Should You Save For Your Down Payment?

For most homebuyers, the best place to save for a down payment is a federally insured high-yield savings account or money market account. These options provide the right balance of safety, interest, and access. If your timeline is clear, short-term CDs or Treasury bills may help you earn a bit more while keeping risk low. If your timeline is longer, you may have more flexibility, but your down payment should become more conservative as your purchase date gets closer.

The most important rule is simple: do not put short-term house money somewhere it can shrink dramatically. Your down payment has a job. It is there to help you buy a home, not audition for a financial thriller.

Save consistently, keep the money separate, protect your principal, and make sure you can access the funds when the right home appears. A smart down payment strategy will not just help you buy a house. It will help you arrive at closing with confidence, breathing normally, and maybe even enough cash left to buy a decent welcome mat.