Table of Contents >> Show >> Hide

- Before You Start: What Goodwill Impairment Is (and Isn’t)

- Step 1: Confirm the Unit of Account and the Timeline

- Step 2: Screen for Triggering Events (a.k.a. “Is Anything On Fire?”)

- Step 3: Decide Whether to Use the Optional Qualitative Assessment (Step 0)

- Step 4: Build the Reporting Unit’s Carrying Amount (Correctly)

- Step 5: Estimate the Reporting Unit’s Fair Value (Valuation Without the Drama)

- Step 6: Measure the Impairment Loss and Record the Journal Entry

- Step 7: Disclose, Document, and Fortify Your Controls

- Quick Recap: The 7 Steps in One Breath

- Common Questions People Ask (Usually Five Minutes Before the Deadline)

- From the Trenches: Experiences That Make Goodwill Impairment “Click” (About )

Goodwill is the accounting equivalent of “we paid extra because we believed in the magic.” It shows up when you buy a business for more than the fair value

of its identifiable net assetsbecause you’re paying for brand reputation, customer relationships, assembled workforce, synergies, and that mysterious

“we swear it’ll scale” factor.

The problem: magic can fade. Under U.S. GAAP, goodwill isn’t amortized for most public companies. Instead, it gets tested for impairment at least annually

(and more often if red flags pop up). If the value of a reporting unit drops below its carrying amount, you may need to write goodwill down and recognize

an impairment lossan expense that can be painful, headline-grabbing, and very popular with absolutely no one.

This guide walks through a practical, audit-friendly way to account for goodwill impairment in 7 steps. We’ll focus on U.S. GAAP concepts

(ASC 350) and keep it real with examples, judgment calls, and the stuff people only learn after the third “can you support that assumption?” email thread.

Before You Start: What Goodwill Impairment Is (and Isn’t)

It is:

- A reduction of goodwill’s carrying amount when a reporting unit’s value falls.

- An expense on the income statement (often presented in operating income, depending on your policy).

- Not a cash outflowmore like an accounting bruise from earlier optimism.

It isn’t:

- A “catch-all” write-down for every bad quarter (the test has rules and documentation expectations).

- A reversal-friendly situationonce goodwill is impaired under U.S. GAAP, you generally don’t write it back up later.

- A substitute for testing other assets: long-lived assets and indefinite-lived intangibles have their own impairment guidance.

Step 1: Confirm the Unit of Account and the Timeline

Goodwill impairment testing happens at the reporting unit level. In plain English: you don’t test the entire company as one blob

unless your reporting structure truly works that way. You test the pieces of the business that are managed and reviewed with separate economics.

What to do

- Identify reporting units and confirm they align with how management views the business (and how you report results internally).

- Confirm goodwill allocation to reporting units is up to dateespecially after acquisitions, reorganizations, or changes in segments.

- Know your test date: many companies pick an annual testing date (e.g., October 1), but you can also test in interim periods if triggering events occur.

Common pitfalls

- Using outdated reporting units after a reorg (“We changed how we manage the business, but our goodwill stayed in 2019.”)

- Forgetting that goodwill has to be assigned to reporting units as of the acquisition date and revisited when the structure changes.

Step 2: Screen for Triggering Events (a.k.a. “Is Anything On Fire?”)

Even if you do an annual test, you also need to consider whether interim impairment testing is required. That’s where triggering events come in:

negative changes that suggest a reporting unit’s fair value may have declined.

Examples of common triggers

- Macroeconomic issues: recession fears, higher interest rates, tighter credit markets

- Industry declines: shrinking demand, new disruptive competitors, reduced market multiples

- Company performance issues: missed forecasts, margin compression, churn spikes, loss of key customers

- Changes in strategy: restructurings, plans to sell or dispose of a reporting unit

- Market signals: sustained stock price decline (for public companies), lower market cap vs. book value

Practical tip

Build a quarterly “impairment watchlist” memo. Keep it short, consistent, and factual: what changed, why it matters, what metrics moved (revenue,

EBITDA, churn, backlog, multiples), and whether it points to a need for deeper testing.

Step 3: Decide Whether to Use the Optional Qualitative Assessment (Step 0)

U.S. GAAP allows an optional qualitative assessmentoften nicknamed “Step 0.” The goal is to decide whether it’s

more likely than not (greater than 50%) that a reporting unit’s fair value is below its carrying amount. If you conclude “no,”

you can skip the quantitative test for that reporting unit for that period.

When Step 0 makes sense

- The reporting unit is performing well and key value drivers are stable.

- You have strong “headroom” from a recent valuation (fair value comfortably above carrying value).

- The economy/industry hasn’t shifted in a way that hits your specific unit.

When to go straight to quantitative testing

- You’ve got clear negative indicators (missed targets, unit profitability issues, market multiple compression).

- Auditors (or your own internal controls) expect a quantified analysis due to risk.

- Management needs a valuation anyway for planning, financing, or investor communications.

Humor break (because impairment testing can be emotionally expensive)

If your Step 0 memo reads like “Everything is fine” while your stock price chart looks like a ski slope, Step 0 may not be your best friend.

Step 4: Build the Reporting Unit’s Carrying Amount (Correctly)

The quantitative test compares fair value of the reporting unit to its carrying amount, including goodwill. That means you need a clean,

supportable carrying amount as of the test dateno mystery balances, no “we’ll reconcile it later,” and definitely no “plug” accounts.

What to do

- Assemble net assets assigned to the reporting unit (assets minus liabilities).

- Include goodwill allocated to that reporting unit.

- Ensure other impairments are considered first where applicable (for example, long-lived assets under separate guidance).

- Document allocations for corporate assets, shared services, and intercompany itemsconsistency matters.

Common pitfalls

- Using management reporting numbers that don’t tie to the general ledger.

- Forgetting working capital, lease liabilities, or unit-level debt assumptions that affect carrying amount.

- Not aligning the “unit” in the valuation with the “unit” in the accounting records.

Step 5: Estimate the Reporting Unit’s Fair Value (Valuation Without the Drama)

Fair value estimation is where accounting meets finance, and where spreadsheets gain sentience. Common approaches include:

Common valuation approaches

- Income approach (often a discounted cash flow model): projected cash flows discounted to present value.

- Market approach (guideline public company or transactions): valuation based on market multiples applied to your metrics.

- Cost approach: less common for operating businesses, more relevant for asset-heavy or early-stage scenarios.

Key assumptions that need support

- Revenue growth rates and margins (tie to budgets, pipeline, historical performance, industry outlook)

- Discount rate (often linked to WACC and risk profile)

- Terminal growth rate or exit multiple (should be consistent with long-term economics)

- Working capital and capex needs (don’t ignore “boring” cash drains)

Specific example: simple market approach snapshot

Suppose your reporting unit generated $12 million of EBITDA. Comparable companies trade around 7.0x EBITDA (after considering differences in size, risk, and growth).

A rough fair value estimate might start near $84 million (12 × 7.0), then adjust for debt-like items or non-operating assets depending on your valuation framework.

Most real-world analyses use more than one approach and reconcile them. The goal isn’t to chase a “perfect” numberit’s to arrive at a reasonable fair value,

supported by evidence, and consistent with the reporting unit definition.

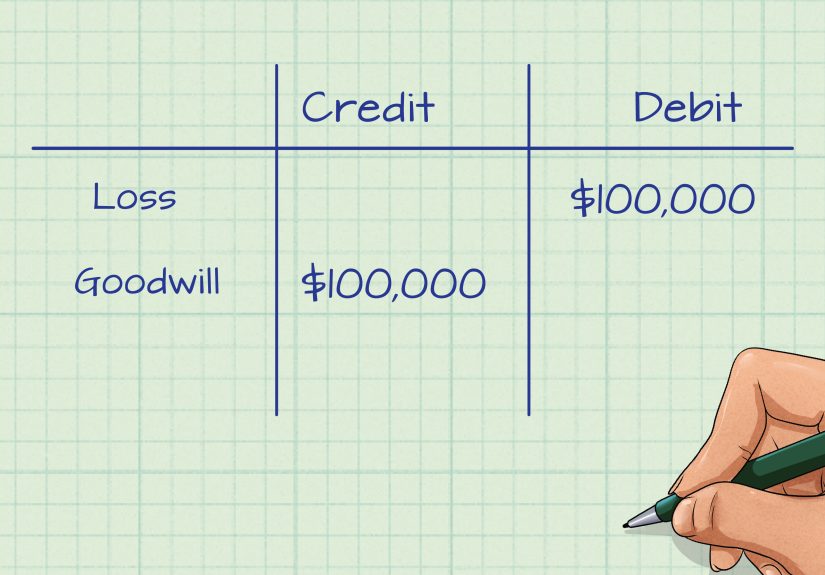

Step 6: Measure the Impairment Loss and Record the Journal Entry

Under the current U.S. GAAP model, the impairment loss is generally the amount by which the reporting unit’s carrying amount exceeds its fair value,

limited to the goodwill balance allocated to that reporting unit.

Worked example (with numbers you can actually audit)

- Carrying amount of reporting unit (including goodwill): $120 million

- Estimated fair value of reporting unit: $100 million

- Implied “gap”: $120m − $100m = $20 million

- Goodwill allocated to reporting unit: $30 million

- Impairment loss recorded: min($20m, $30m) = $20 million

Journal entry (typical)

Debit: Goodwill impairment loss (P&L) $20,000,000

Credit: Goodwill (Balance Sheet) $20,000,000

What happens next

- The reduced goodwill becomes the new accounting basis.

- Under U.S. GAAP, goodwill impairment losses generally cannot be reversed in future periods even if business performance improves.

Tax note (don’t let book and tax fight in the hallway)

Goodwill impairment is a book expense. It does not automatically create a current tax deduction. In many cases, U.S. tax goodwill

(for asset acquisitions) is amortized over 15 years regardless of book impairment, so you may see book/tax differences and deferred tax effects.

Work closely with your tax team to assess tax basis, deductibility, and deferred tax implications for your facts.

Step 7: Disclose, Document, and Fortify Your Controls

The accounting entry is the easy part. The hard part is being able to explain itclearlyto auditors, regulators (if applicable), lenders, investors,

and your future self who will absolutely forget why you picked that terminal growth rate.

Disclosure checklist (high-level)

- Goodwill rollforward and allocation by reporting unit (as applicable)

- Impairment loss amount, where it’s recorded in the income statement

- Key facts and circumstances leading to impairment (triggering events)

- Valuation methods used (income approach, market approach, etc.)

- Significant assumptions and sensitivity (especially if impairment risk remains)

Documentation checklist (the “audit-proof me” file)

- Reporting unit determination memo (and any changes from prior years)

- Goodwill allocation support and tie-out to the GL

- Triggering events analysis (quarterly or interim, if relevant)

- Step 0 qualitative assessment memo (if used)

- Valuation model(s), inputs, source data, and reconciliation of approaches

- Management review evidence (sign-offs, review notes, meeting minutes)

Practical controls that reduce pain later

- Standardize templates for Step 0 and interim trigger reviews.

- Keep a consistent approach year over year unless facts change (and document when they do).

- Perform “assumption challenge” sessions: ask what would need to be true for the model to be wrong.

Quick Recap: The 7 Steps in One Breath

- Confirm reporting units, goodwill allocation, and test timeline.

- Screen for triggering events and decide if interim testing is needed.

- Use (or skip) the optional qualitative assessment (Step 0).

- Build a clean, supportable reporting unit carrying amount.

- Estimate fair value using appropriate valuation approaches and evidence.

- Measure impairment (limited to goodwill) and record the journal entry.

- Disclose, document, and strengthen controls for repeatability.

Common Questions People Ask (Usually Five Minutes Before the Deadline)

“If we fail Step 0, does that mean we must record an impairment?”

Not necessarily. Failing Step 0 just means you need the quantitative test. The quantitative analysis may still show fair value exceeds carrying amountno impairment.

“Can we avoid impairment by changing assumptions?”

You can’t “assumption” your way out of reality without consequences. Reasonable assumptions must be consistent with evidence: budgets, market data, performance trends,

and risk. If your assumptions are doing backflips, auditors will notice.

“Is goodwill impairment a sign the acquisition was a mistake?”

Sometimes. Sometimes it’s macro conditions, interest rates, valuation multiple compression, or a shift in strategy. It’s a signal that expected economic benefits changed

but context matters.

From the Trenches: Experiences That Make Goodwill Impairment “Click” (About )

If you ask accountants what goodwill impairment feels like, you’ll hear the same theme: it’s never just a calculationit’s a story. And the story is what everyone

will ask about. One controller described it like this: “The spreadsheet took a week. The conversations took a quarter.” That sounds dramatic until you’ve lived through

the follow-ups: Why now? Why this unit? Why that discount rate? Why did the margin forecast change? Why didn’t you see it earlier?

A common real-world scenario starts with a subtle trigger: a reporting unit misses forecast by 8% in Q2, then 12% in Q3. Management shrugs and says it’s “timing.”

But the market doesn’t always accept timing as a business model. Comparable company multiples contract, financing costs rise, and suddenly the fair value cushion you

relied on last year is thinner than a dollar-store napkin. This is when Step 0 becomes less of a shortcut and more of a fork in the road: either you have strong

evidence that value still exceeds carrying amount, or you’re about to spend quality time with a valuation model.

Another “classic” is the reorg. A company merges two operating groups, moves leadership, and changes how performance is reviewed. Everyone updates the org chart and

Slack channelsthen forgets goodwill is still assigned to the old reporting units. Months later, the impairment test arrives, and the team realizes the valuation is

built around the new structure while the accounting carrying amounts are still mapped to the old one. Fixing that mapping often takes longer than the valuation itself,

because you’re forced to defend allocations for shared assets, corporate costs, and intercompany balances. Lesson learned: when the business changes shape, goodwill

doesn’t magically teleport; you have to move it with documentation.

People also underestimate how emotional impairment can be for leadership. Internally, an impairment charge can feel like a public admission that the acquisition

didn’t deliver what was promised. That’s why the best teams treat impairment testing like a governance process, not an ambush. They involve finance leaders early,

align assumptions with approved budgets, and make sure the narrative is consistent: if the valuation assumes a rebound next year, the operating plan better explain

hownew products, pricing changes, retention programs, cost reductionssomething concrete.

The most practical experience-driven tip is also the least glamorous: write down your rationale as you go. Don’t wait until the end to “tell the story.”

Keep a running memo of what changed since the last test (macroeconomics, industry multiples, performance, strategy), what data you relied on, and how you concluded.

When auditors ask why your terminal growth rate is 3.0% instead of 2.5%, the worst answer is “because that’s what we used last year.” The best answer is a short,

evidence-based explanation tied to long-term inflation expectations, industry growth, and the unit’s maturity stage. It doesn’t need to be poeticjust defensible.

Finally, many teams discover that impairment testing can actually improve decision-making. A thoughtful valuation forces clarity: which products drive cash flow,

where margins are realistically headed, and what assumptions are doing the heavy lifting. Even when the result is “no impairment,” the process can spotlight risks

early enough to actbefore the only “action” left is a journal entry.