Table of Contents >> Show >> Hide

- Dividend Basics (So the Math Has a Home)

- The Core Dividend Formulas You’ll Actually Use

- Step-by-Step: How to Calculate Dividends for Your Portfolio

- Dividend Calculator (Copy/Paste HTML + Works in the Browser)

- Common Dividend Calculation Mistakes (And How to Avoid Them)

- Dividends in ETFs and Funds: Yield Can Mean Different Things

- Taxes and Dividends (Quick, Practical Version)

- Quick Reference Cheat Sheet (Bookmark-Style)

- Real-World Experiences and Lessons (500+ Words of Practical “Been-There” Scenarios)

- Conclusion

Dividends are one of those investing topics that sound fancy until you realize they’re basically a company saying,

“Heretake some of our profits,” and shareholders saying, “Don’t mind if I do.”

The tricky part isn’t getting dividends (that depends on what you own), it’s knowing how to

calculate dividends correctlyper share, per year, as a yield, and across a whole portfoliowithout

accidentally turning your math into modern art.

This guide walks you through the most useful dividend formulas, shows clear examples, and includes a

copy-and-paste-friendly dividend calculator you can run right in your browser.

By the end, you’ll be able to answer questions like: “How much will I receive?”, “What’s the dividend yield?”, and

“Is this payout actually sustainableor is it one bad quarter away from disappearing?”

Dividend Basics (So the Math Has a Home)

A dividend is a portion of a company’s profit paid out to shareholders. Many dividend-paying companies follow a

regular schedule (often quarterly), but dividends can also be irregularlike special dividends that pop

up when a company has extra cash to distribute.

The 3 dividend dates that matter

- Declaration date: The company announces the dividend amount and schedule.

- Record date: The company checks its shareholder list to see who qualifies.

- Ex-dividend date: The cutoff for buying shares and still receiving the dividend.

The ex-dividend date is the one investors obsess over. Buy before it, and you generally get the dividend.

Buy on or after it, and the seller gets paid instead. (Yes, it feels personal.)

The Core Dividend Formulas You’ll Actually Use

1) Dividends Per Share (DPS)

Dividend per share (DPS) tells you how much dividend is paid for each share you own.

It’s the cleanest starting point for most dividend calculations.

Formula:

DPS = Total Dividends Paid ÷ Shares Outstanding

Example: A company pays $50,000,000 in dividends and has 100,000,000 shares outstanding.

DPS = 50,000,000 ÷ 100,000,000 = $0.50 per share

If you own 200 shares, your dividend for that period would be 200 × $0.50 = $100.

2) Total Dividends You Receive

Once you know DPS, your personal dividend amount is straightforward.

Formula:

Your Dividend = Shares You Own × DPS

Example: You own 120 shares. The dividend is $0.42 per share.

Your Dividend = 120 × 0.42 = $50.40

3) Annual Dividend (If the Company Pays Quarterly or Monthly)

Many companies pay dividends quarterly. Some pay monthly. To compare apples to apples, investors often

convert payouts to an annual figure.

Formula:

Annual Dividend Per Share = Dividend Per Period × Number of Periods Per Year

Example (quarterly): $0.75 per quarter × 4 quarters = $3.00 per share per year

Example (monthly): $0.10 per month × 12 months = $1.20 per share per year

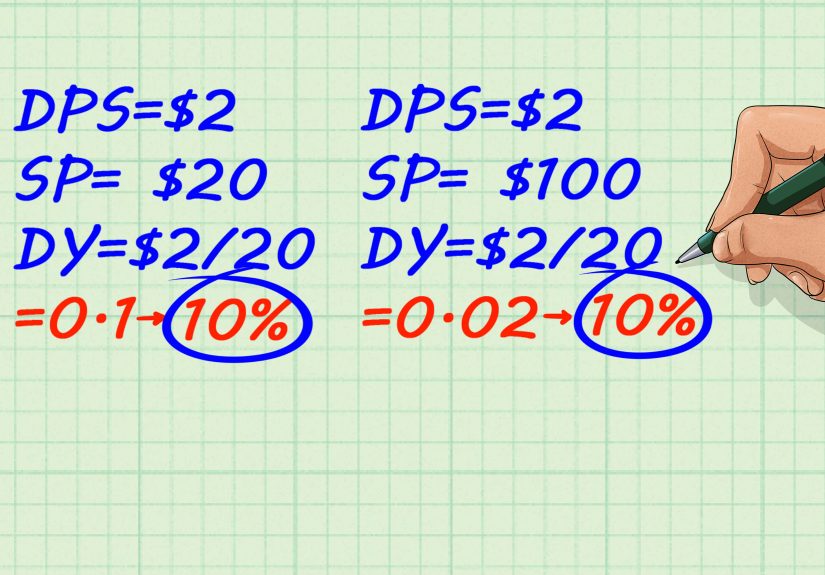

4) Dividend Yield (The “How Big Is This Dividend?” Percentage)

Dividend yield is the dividend expressed as a percentage of the stock price.

It’s one of the most searched metrics in dividend investingand also one of the most misunderstood.

Formula:

Dividend Yield = Annual Dividend Per Share ÷ Current Share Price

Example: A stock pays $2.00 per share annually and trades at $50.

Yield = 2.00 ÷ 50 = 0.04 = 4%

Important: A high yield can mean “nice income,” or it can mean “the stock price fell because the

market thinks something is wrong.” Yield is a cluenot a verdict.

5) Dividend Payout Ratio (Is the Dividend Sustainable?)

The payout ratio shows what portion of a company’s net income is being paid out as dividends.

It helps you judge whether a dividend is comfortably funded or running on financial caffeine.

Formula:

Dividend Payout Ratio = Dividends Paid ÷ Net Income

Example: A company earns $1 billion and pays $400 million in dividends.

Payout Ratio = 400,000,000 ÷ 1,000,000,000 = 40%

Payout ratios vary by industry. Some mature companies return a large chunk of earnings.

Fast-growing companies may pay little (or nothing) and reinvest instead.

Step-by-Step: How to Calculate Dividends for Your Portfolio

Scenario A: You know the dividend per share

- Find the dividend per share (DPS) for the period (e.g., quarterly dividend).

- Multiply DPS by how many shares you own.

- If you want annual income, multiply by the number of payments per year.

Example: You own 350 shares. Quarterly dividend is $0.28.

Quarterly income = 350 × 0.28 = $98.00

Estimated annual income = $98.00 × 4 = $392.00

Scenario B: You only know the dividend yield

Sometimes you see a yield percentage first (like 3.5%) and want the dollars.

If you know the stock price and yield, you can estimate the annual dividend per share.

Formula:

Annual Dividend Per Share ≈ Dividend Yield × Share Price

Example: Yield is 3.5% (0.035) and price is $80.

Annual dividend per share ≈ 0.035 × 80 = $2.80

Then multiply by shares owned to estimate your annual dividend income.

Scenario C: You want portfolio-wide dividend income

For multiple holdings, calculate each position’s annual dividend income and add them up:

Formula:

Total Annual Dividend Income = Σ (Shares × Annual Dividend Per Share)

Mini example:

Stock A: 100 shares × $1.20 = $120

Stock B: 60 shares × $3.00 = $180

Stock C: 40 shares × $0.80 = $32

Total annual dividend income = $332

Dividend Calculator (Copy/Paste HTML + Works in the Browser)

Use this calculator to estimate:

your dividend payment, annual dividend income, and dividend yield.

Enter whatever you knowleave the rest blankand it’ll do the math it can.

Dividend Formula Calculator

Notes: This calculator assumes the dividend rate stays the same over a full year.

Real-world dividends can change, and some companies pay special dividends that shouldn’t be annualized.

Common Dividend Calculation Mistakes (And How to Avoid Them)

Mixing up “per payment” dividends with “annual” dividends

A $0.50 dividend might be quarterlymeaning $2.00 annually. Always check the payment frequency before you compare

two stocks. Otherwise you’ll compare a bicycle to a sandwich and wonder why the returns taste funny.

Annualizing a special dividend

Special dividends are one-time (or rare) payments. If you treat them as recurring, you’ll calculate a yield that looks

amazing… and then vanishes like a magician’s rabbit. Use regular dividends for forward-looking estimates.

Forgetting share changes and DRIPs

If you reinvest dividends through a DRIP, your share count can increase via fractional shares. That changes your next

dividend payment. Great for compounding, confusing for spreadsheetsunless you track it.

Dividends in ETFs and Funds: Yield Can Mean Different Things

With ETFs and mutual funds, you’ll see yield figures like “distribution yield,” “SEC yield,” or trailing 12-month yield.

These can be calculated differently depending on what’s included (income distributions only vs. income plus capital gains).

The key is to read the label: two yields with the same percentage may not represent the same type of payout.

Taxes and Dividends (Quick, Practical Version)

In taxable accounts, dividends are generally reportable, even if reinvested. Brokerages typically provide Form 1099-DIV

to summarize what you received.

Some dividends may be classified as qualified dividends and taxed at long-term capital gains rates

if certain requirements are met (including a holding period around the ex-dividend date). Others are ordinary

dividends taxed at ordinary income rates. For most investors, the “qualified vs. ordinary” breakdown shows up

clearly on tax forms, but it’s still worth understanding what drives the differenceespecially if you’re designing a

dividend strategy for a taxable account.

Quick Reference Cheat Sheet (Bookmark-Style)

- DPS: Total Dividends Paid ÷ Shares Outstanding

- Your Dividend: Shares You Own × DPS

- Annual Dividend/Share: Dividend/Payment × Payments per Year

- Dividend Yield: Annual Dividend/Share ÷ Current Share Price

- Payout Ratio: Dividends Paid ÷ Net Income

Real-World Experiences and Lessons (500+ Words of Practical “Been-There” Scenarios)

Dividend math is simple on paper, but real life loves curveballs. Here are common experiences investors run into when

they start calculating dividendsand what tends to click after you’ve wrestled with the numbers for a while.

1) The “Wait… why did my dividend change?” moment

A lot of people assume dividends are fixed forever. Then a company raises (or cuts) the dividend, and the spreadsheet

starts throwing surprises. The lesson: treat dividend estimates like weather forecasts. If you base your budget on a

“guaranteed” dividend income figure, you may get soaked. Many investors learn to keep a range (best case / expected /

conservative) rather than one single number.

2) The “High yield” trap that looked like a deal

A double-digit yield can be tempting, especially when savings accounts feel boring. But high yield can happen because

the dividend is large… or because the stock price fell hard. Investors often learn to pair yield with payout ratio,

earnings stability, and industry context. In other words, a 10% yield isn’t automatically a bargainsometimes it’s a

warning label printed in very cheerful font.

3) DRIP compounding is powerful… and sneaky

Reinvesting dividends through a DRIP feels slow at first. Then, a year later, you notice you own 0.37 shares you don’t

remember buying. Two years later, you own 1.86 “bonus” shares. The experience most investors report is that DRIPs are

boring in the best way: they quietly build share count, and share count quietly builds future dividends. The math lesson

is simple: if your shares go up over time, your dividend income can rise even if the dividend rate stays unchanged.

The practical lesson: track your share count, not just the dividend rate.

4) Comparing stocks vs. ETFs: same word, different meaning

Investors often discover that “yield” for an ETF can represent distributions that vary month to month and may include

different components depending on the fund. Someone may calculate expected income using last month’s distribution and

annualize itonly to see a different pattern the next quarter. The real-world fix: use trailing 12-month distributions

when possible for a smoother estimate, and recognize that funds can distribute income differently than individual stocks.

5) The “ex-dividend date” misunderstanding

A classic experience: someone buys a dividend stock the day before payout, expecting easy money, and then sees the stock

price drop around the ex-dividend date. That’s not the market being rude; it’s the market adjusting. Dividends are value

transferred from company to shareholders, so prices often reflect that transfer. The lesson most investors take away is:

buying solely for the dividend date rarely creates free profit. The dividend can be greatjust don’t confuse it with a

coupon code.

6) Getting serious: building a “dividend dashboard”

After calculating dividends a few times, many investors end up building a simple dashboard: holdings, shares, DPS, payment

frequency, estimated annual income, and yield. The experience here is surprisingly motivating: turning your dividend stream

into a measurable number makes it feel real. It also helps you notice patternslike which positions drive most of your

income, or how a dividend increase changes your annual cash flow.

If there’s one big takeaway from these real-world scenarios, it’s this: dividend calculations aren’t just math problems.

They’re decision tools. Once you can calculate dividends confidently, you can compare opportunities clearly, spot red flags

faster, and design an income plan that’s built on realitynot wishful rounding.

Conclusion

Calculating dividends isn’t complicatedbut it does require using the right formula for the right question.

Start with dividend per share, scale it to your shares owned, annualize it carefully, and use dividend yield and payout

ratio to judge what the numbers mean. If you want a shortcut, use the calculator above to estimate payments and yields in

seconds (without accidentally annualizing a one-time dividend and getting your hopes up).