Table of Contents >> Show >> Hide

- Why Interest Rates Feel Like the Market’s Thermostat

- Market Timing: The Trap Door Hidden Under “Pretty Good Logic”

- How Interest Rates Move Stocks (and Why “Growth” Gets the Sweats)

- How Interest Rates Move Bonds (Yes, Even “Safe” Ones)

- The Rate-Cycle Mirage: “I’ll Just Invest After the Fed Pivots”

- So What Should You Do Instead of Timing?

- Where the Yield Curve Fits (and Where It Doesn’t)

- Putting It All Together: A Simple “Rate-Aware” Playbook

- Conclusion: Respect Rates, Don’t Worship Them

- Extra: of Real-World “Been There” Experiences (Without Pretending We’re Psychic)

If you’ve ever tried to “wait for rates to come down” before investing, congratulations: you’ve joined the largest unofficial club in personal financeright next to “I’ll start exercising on Monday” and “This time I’ll remember my password.”

Interest rates matter. A lot. They influence what you pay on a mortgage, what a company pays to borrow, what a bond fund does on a rough Tuesday, and why your friend suddenly won’t stop talking about “cash yields.” But here’s the twist: knowing rates matter is not the same as successfully timing the market because of rates.

This article breaks down how interest rates ripple through stocks and bonds, why market timing tends to backfire (especially around rate moves), and what to do insteadwithout pretending you can outguess the Federal Reserve from your kitchen table.

Why Interest Rates Feel Like the Market’s Thermostat

Interest rates are the price of money. When rates rise, borrowing costs go up. When rates fall, borrowing costs ease. Simple, right? Then why does the market act like it just spilled coffee on its keyboard every time the Fed speaks?

Because markets don’t just react to today’s rate level. They react to expectationswhat investors think rates will be next quarter, next year, and beyond. That’s why you’ll sometimes see stocks rally on a rate hike (yes, really) if the hike was already expected or if the Fed hints it’s nearing the end of the cycle.

The key rates to know (without needing a PhD)

- Federal funds rate: The Fed’s benchmark short-term rate target. It influences many other short-term interest rates.

- Bond yields: Market-driven rates investors demand to lend money to the government or companies for different time periods.

- Discount rate (in valuation terms): The rate used to translate future cash flows into today’s dollars. Higher discount rates usually mean lower present values.

So when people say, “Rates are going up,” what they often mean is: the entire pricing ecosystem is shiftingloans, bond yields, valuation assumptions, and investor appetite for risk.

Market Timing: The Trap Door Hidden Under “Pretty Good Logic”

Market timing usually starts with a reasonable thought:

“If rates are rising, stocks might fallso maybe I should wait.”

The problem is that markets frequently reprice long before the headline is obvious. And the best days in the market tend to cluster around the worst daysmeaning if you step out “until things feel better,” you often miss the bounce that follows the panic.

Missing a few great days can hurt more than you think

Multiple major firms have shown versions of the same lesson: being out of the market for even a small number of the best days can drastically reduce long-term results. And those best days often show up during volatile, scary stretchesexactly when market timers are most likely to be sitting in cash.

Here’s a plain-English takeaway: if you try to dodge declines by jumping in and out, you’re not just betting on when to sell. You’re also betting on when to buy back in. That second bet is where many strategies quietly fall apart.

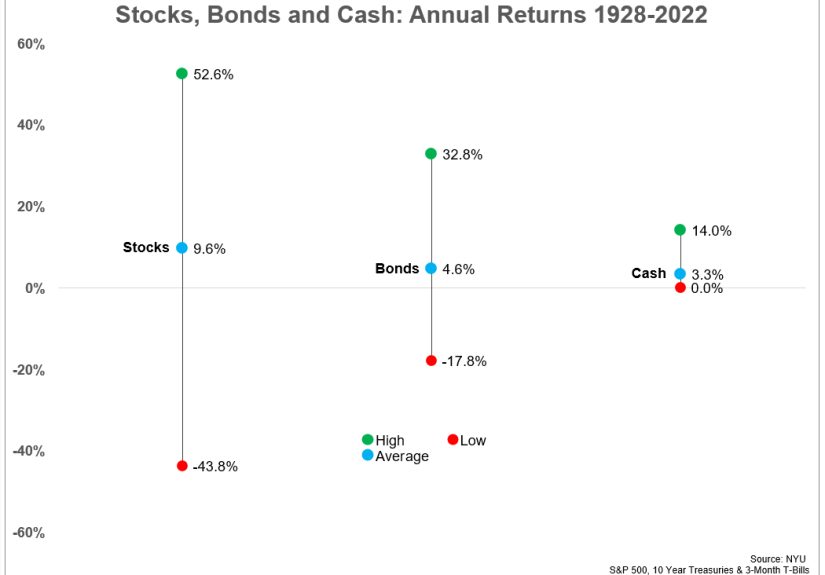

How Interest Rates Move Stocks (and Why “Growth” Gets the Sweats)

Interest rates affect stocks through several channels, but two are the biggest headline-makers:

1) The discount-rate effect: future profits become “worth less” today

Stocks represent a claim on future cash flowsearnings, dividends, buybacks, and business growth. When interest rates rise, the discount rate used in valuation models often rises too. A higher discount rate reduces the present value of future cash flows, which can pressure stock pricesespecially for companies whose profits are expected far in the future.

This is why fast-growing “story stocks” can be more rate-sensitive. If most of a company’s expected payoff is “later,” higher rates can shrink the value of that “later” more dramatically.

2) The economic effect: borrowing costs and spending behavior change

Higher rates can mean:

- Companies face higher costs to finance expansion or refinance debt.

- Consumers pay more for credit cards, auto loans, and mortgagesoften reducing discretionary spending.

- Investors can earn more from cash and short-term bonds, which may compete with riskier assets.

Lower rates can reverse many of these pressures, which is why rate-cut cycles often come with a different set of winners and losers.

A practical example (no spreadsheets required)

Imagine two companies:

- Company A earns steady profits today and pays dividends.

- Company B reinvests heavily and expects most profits years from now.

When rates rise, Company B’s long-dated future cash flows often take a bigger valuation hit than Company A’s near-term cash flows. That doesn’t mean Company A always “wins,” but it explains why rate headlines can reshuffle leadership among sectors and styles.

How Interest Rates Move Bonds (Yes, Even “Safe” Ones)

Bonds have a famously awkward relationship with interest rates: when rates go up, existing bond prices generally go down (and when rates fall, existing bond prices generally rise). This is not the universe being mean to you personally; it’s basic math.

Why bond prices fall when yields rise

If a newly issued bond pays 5% and your older bond pays 3%, your bond is less attractiveunless it sells at a discount. That discount is what makes its effective yield competitive again.

Duration: the “sensitivity dial” for bond price moves

Duration is a measure of how sensitive a bond (or bond fund) is to interest-rate changes. A higher duration generally means bigger price movement for a given change in ratesup or down.

Example: If a bond fund has an average duration of about 5 years, a 1 percentage-point rise in rates might translate into roughly a 5% price decline (before considering income, credit changes, and other moving parts). If rates fall by 1 percentage point, the price move could be roughly positive in the same neighborhood.

Duration isn’t a prophecy; it’s a risk gauge. But it’s one of the clearest ways to connect “rates moved” with “why my bond fund moved.”

Holding individual bonds to maturity vs. owning bond funds

If you own an individual bond and hold it to maturity, you’ll typically receive face value at maturity (assuming no default). Price fluctuations on the way can matter less if you truly don’t need to sell.

Bond funds don’t “mature” in the same way. They constantly buy and sell bonds, so their net asset value (NAV) can fluctuate more visibly when rates move. That’s not automatically badfunds also recycle into higher yields over timebut it changes the experience.

The Rate-Cycle Mirage: “I’ll Just Invest After the Fed Pivots”

This is a classic plan. It sounds tidy. It also tends to be expensive.

Why? Because markets often anticipate policy shifts well before the pivot is official. Investors trade on expectations, probabilities, and forward guidance. By the time the Fed actually cuts rates, the market may have already movedsometimes dramatically.

Also, rate cuts don’t always happen in a cheerful environment. Often, the Fed cuts because something is breaking, slowing, or scaring people. That can mean stocks are volatile even as rates fall.

So What Should You Do Instead of Timing?

You can respect interest rates without trying to day-trade them. Here are strategies that acknowledge rate reality while dodging the market-timing potholes.

1) Use dollar-cost averaging if you’re nervous

If you have a lump sum and fear investing it “right before rates spike,” consider investing it over time (weekly or monthly). Dollar-cost averaging won’t guarantee better returns, but it can reduce regret and help you actually follow through.

2) Match bond duration to your time horizon

Need money in 1–3 years? Taking long-duration risk may not be your best friend. Longer time horizon? You can usually tolerate more duration risk because you have time to earn income and let yields reset.

3) Build a “barbell” for cash + longer-term goals

Some investors keep:

- Short-term reserves in cash or very short-term instruments for stability, and

- Longer-term money diversified in stocks and intermediate-term bonds for growth and income.

This approach can reduce the urge to sell risk assets at the worst time just to feel safe.

4) Rebalance: a boring superpower

When rates change, different assets move differently. Rebalancing forces you to trim what grew and add to what fellsystematically. It’s like buying low and selling high… without needing to predict anything.

5) Focus on what rates actually change for you

Instead of “Where will the Fed go next?”, ask:

- Am I taking more stock risk than I can stomach?

- Is my bond risk aligned with when I’ll need the money?

- Do I have enough liquidity for emergencies?

- Am I diversified across sectors, styles, and maturities?

Those questions produce decisions you can controlunlike guessing the next press conference mood.

Where the Yield Curve Fits (and Where It Doesn’t)

The yield curve compares interest rates across different maturities (like 3-month, 2-year, 10-year Treasuries). When shorter-term yields exceed longer-term yields, the curve can “invert,” and investors often interpret that as a warning sign about future economic growth.

Important nuance: the yield curve is a signal, not a stopwatch. Even when it has been informative historically, it doesn’t tell you when something will happen or how markets will behave in the meantime.

In practice, the yield curve can be a useful context tool for risk managementbut it’s a shaky foundation for “sell everything now, buy it back later.”

Putting It All Together: A Simple “Rate-Aware” Playbook

When rates are rising

- Expect bond volatility, especially in longer-duration holdings. Understand your duration exposure.

- Review equity mix: highly valued, long-duration growth stocks can be more sensitive to discount-rate changes.

- Avoid all-or-nothing moves: rising rates don’t automatically mean stocks must collapse; the economy and earnings matter too.

- Keep contributions steady if you’re a long-term investorvolatility can be your friend when you’re buying regularly.

When rates are falling

- Don’t assume it’s all good news: cuts can happen because growth is weakening.

- Bonds may benefit (prices can rise as yields fall), but credit risk can also matter more in downturns.

- Stay diversified: leadership can rotate quickly across sectors as expectations shift.

Always

- Keep a realistic emergency fund so you’re not forced to sell investments during turbulence.

- Rebalance periodically instead of reacting to headlines.

- Choose a strategy you can repeat in good markets and bad ones.

Conclusion: Respect Rates, Don’t Worship Them

Interest rates influence stock valuations, bond prices, and investor behavior in powerful ways. But the market usually prices rate expectations before they become obvious, and the most dramatic market days often arrive during the most uncomfortable headlines. That combination is why “market timing & interest rates” is such a temptingand often costlypair.

The smarter approach is to be rate-aware, not rate-obsessed: match bond duration to your timeline, diversify across assets, rebalance, and invest consistently. You don’t need to predict the next rate decision to build a resilient plan. You need a plan that doesn’t fall apart when the next rate decision arrives.

Extra: of Real-World “Been There” Experiences (Without Pretending We’re Psychic)

Below are common experiences investors report when interest rates are moving fast. Think of these as “investing campfire stories”useful because they’re familiar, not because they’re magical.

Experience #1: The “I’ll wait until rates come down” stall

A typical investor sees rates rising and parks money in cash “temporarily.” At first, it feels smart: cash yields improve, headlines sound scary, and nobody gets fired for doing nothing. The problem shows up later. Markets often rebound before the news feels safe, and the investor waits for a perfect signal that never arrives. Eventually they buy back inusually after prices have already recovered. The lesson isn’t “cash is bad.” The lesson is that indefinite waiting is a strategy that quietly turns into market timing.

Experience #2: The bond fund surprise

Another investor buys a bond fund for “stability” and is shocked when it declines during a period of rising rates. They expected bonds to be the calm part of the portfolio. What they learned (the hard way) is duration: longer-maturity bond exposure can drop when yields rise, even if the bonds are high quality. The better outcome comes when they understand what they own, adjust duration to match their timeline, and remember that higher yields can improve future income over time. The lesson: bonds reduce volatility, but they’re not immune to rate math.

Experience #3: The “Fed pivot” fantasy draft

Some investors try to time the exact moment the Fed will shift from hiking to cutting. They watch every inflation print like it’s the season finale of a prestige drama. When a cut finally happens, they expect instant stock fireworksonly to discover that cuts can occur during economic slowdowns, when earnings expectations are falling and markets are jumpy. They learn that the market is a forward-looking voting machine: it can rally before cuts and wobble during cuts. The lesson: policy direction matters, but context matters more.

Experience #4: The calm investor with a process

Then there’s the investor who does the unglamorous stuff: they keep an emergency fund, invest on a schedule, diversify, and rebalance once or twice a year. When rates rise, they don’t panic-sell; they check whether their bond duration still fits their needs and whether their stock allocation still matches their risk tolerance. When rates fall, they don’t assume “easy money forever”; they stay diversified and keep contributing. Their experience isn’t thrilling, but it’s repeatable. The lesson: a process beats predictions.

If there’s one universal “experience” worth aiming for, it’s this: make decisions you can defend even when the next headline tries to rent space in your brain.