Table of Contents >> Show >> Hide

- What “Market Timing” Actually Means

- Why Market Timing Is So Hard (Even for Pros)

- The “Missing the Best Days” Problem

- Common Market Timing Myths (and Why They’re So Tempting)

- What Works Better Than Market Timing

- When Market Timing Temptation Hits: A Quick Reality Check

- A Word on “Fancy” Timing Tools

- So… Is Market Timing Ever Useful?

- Conclusion: The Goal Isn’t Perfect TimingIt’s a Durable Strategy

- Experiences: What “Trying to Time the Market” Feels Like in Real Life (Extra Section)

Market timing sounds so simple in theory: “Buy before it goes up, sell before it goes down.”

That’s basically the same plan as “I’ll just guess the winning lottery numbers and then retire by Thursday.”

The problem isn’t that investors lack intelligenceit’s that markets are fast, emotional, noisy, and often rude.

They’ll drop on good news, rally on bad news, and make you question whether the universe is buffering.

The good news: you don’t need perfect timing to build wealth over time. The bad news: your brain will still

really want to try. Let’s break down why market timing is so difficult, what the research and real-world

experience suggest, and what you can do insteadwithout stapling yourself to financial TV.

What “Market Timing” Actually Means

Market timing is an active strategy where an investor shifts money in and out of the market (or between sectors

and asset classes) to benefit from short-term price movements. It can look like holding cash while “waiting for

the dip,” jumping from stocks to bonds because of a scary headline, or trying to rotate into whatever is “about to

take off.”

The two calls you have to get right

Here’s the part many people underestimate: timing isn’t one decisionit’s two.

You have to (1) get out at the right time, and (2) get back in at the right time.

Miss either step and you’re not “timing the market,” you’re just doing interpretive dance with your portfolio.

Why Market Timing Is So Hard (Even for Pros)

1) The market’s best days often cluster around its worst days

One of the most consistent findings across market commentary and historical analysis is that big up days and big

down days tend to happen near each otheroften during volatile, stressful periods. That’s brutal for market timers,

because the moments that feel scariest are often the same windows when the market can rebound sharply.

If you step out “until things calm down,” you may step out of the recovery, too.

2) News travels faster than feelingsbut faster than you, too

By the time a headline feels “confirmed,” markets have usually moved. Prices incorporate expectations, rumors,

data leaks, analyst notes, and institutional positioning long before the average person has finished refreshing

their feed. Timing based on news often means reacting after the factlike trying to dodge a wave after it already

soaked your socks.

3) You’re competing with systems built for speed

Modern markets include algorithmic trading, institutional flows, and rapid re-pricing. That doesn’t mean an

everyday investor can’t succeedlong-term investing is still accessiblebut it does mean short-term timing is a

tougher arena than it looks from the outside.

4) Costs, taxes, and whiplash are real

Timing strategies can increase trading costs, widen the spread between what you want and what you get, and trigger

taxes in taxable accounts. Even “free trades” aren’t truly free if frequent decision-making leads to worse

outcomes. Sometimes the biggest expense in investing is not a feeit’s an overconfident click.

5) Your brain is not a neutral observer

Behavioral finance is basically a fancy term for “humans panic and celebrate at inconvenient times.” Losses feel

bigger than gains. Uncertainty feels urgent. And when markets fall, it can feel safer to do somethinganything

even if the best move is to stick to the plan.

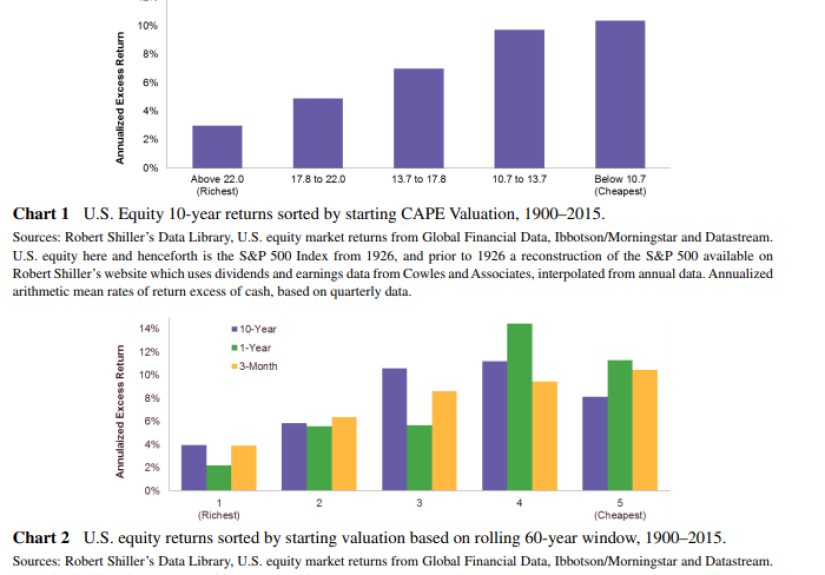

The “Missing the Best Days” Problem

Many investment firms and market educators have illustrated a frustrating reality: missing just a handful of the

market’s strongest days can significantly reduce long-term returns. The exact numbers vary depending on the time

period studied, but the message tends to be consistent across major firms:

the market’s biggest gains can be concentrated in surprisingly few days.

The trap is that market timers often miss those days because they happen during or right after scary periodswhen

a “wait and see” approach feels emotionally logical. In other words, the market hands out some of its best

returns when confidence is running low and group chats are full of doom.

A simple example (no crystal ball required)

Imagine two investors who both believe in stocks long-term:

- Alex invests steadily and stays invested through downturns.

- Taylor sells during scary moments and waits for a “clear sign” before buying back in.

Taylor might avoid part of the decline, but if Taylor misses only a small set of rebound days, Alex can still end

up ahead. And because rebounds can be sharp and fast, “waiting for clarity” can mean buying back in after prices

already climbed.

Common Market Timing Myths (and Why They’re So Tempting)

Myth 1: “I’ll get in once things feel safer.”

Markets typically move before the emotional environment feels safe. By the time headlines turn optimistic, prices

may already reflect that optimism. Your feelings are validbut they’re not a reliable market indicator.

Myth 2: “I’ll buy at the bottom.”

Market bottoms are easiest to identify in hindsight, right next to “should’ve called my friend back in 2017.”

In real time, bottoms look like chaos, not a coupon code.

Myth 3: “All-time highs mean it’s too late.”

Markets spend a lot of time near highs because long-term growth tends to push them upward over time. “High” can

still be followed by “higher.” A better question than “Is the market high?” is “Does my plan match my goals and

time horizon?”

Myth 4: “This time is different.”

Sometimes it ishistory doesn’t repeat perfectly. But “different” doesn’t automatically mean “I can time it.”

The future can be weird and still reward patience.

What Works Better Than Market Timing

1) Build a plan that matches your time horizon

If you need money next month, stocks are not a great place to park it. If you’re investing for years or decades,

volatility is part of the ride. The key is aligning risk with the timelineso you’re not forced to sell at a bad

time.

2) Use diversified asset allocation

A thoughtful mix of stocks, bonds, and cash (the exact mix depends on the person) can reduce the pressure to make

dramatic moves. Diversification doesn’t prevent losses, but it can help smooth the experience so you’re less

likely to panic-sell during downturns.

3) Consider dollar-cost averaging (DCA) if you’re nervous

If you have a lump sum and you’re worried about investing it all right before a pullback, dollar-cost averaging

can help you ease in over time. Historically, lump-sum investing often has a higher expected return because money

is invested sooner, but DCA can reduce regret and help people stick with the plan. The “best” approach is the one

you can follow without self-sabotage.

4) Rebalance instead of “predict”

Rebalancing means periodically bringing your portfolio back to its target mix. If stocks have surged and now

dominate your portfolio, rebalancing trims risk. If stocks have dropped and your allocation is lower than your

target, rebalancing can nudge you to buy at lower pricesautomatically, without needing a prophecy.

5) Create rules for what you’ll do during scary markets

The best time to write your “volatility rules” is when you’re calm. Examples:

- If the market drops, I will not make a major change for 72 hours.

- I will keep automatic contributions running unless my income changes.

- I will rebalance on a schedule (quarterly, semiannually, or annually) rather than reacting to headlines.

- I will keep an emergency fund so I don’t have to sell investments during a downturn.

When Market Timing Temptation Hits: A Quick Reality Check

Ask these five questions before you act

- What changed in my goals? (Not the newsmy goals.)

- Am I reacting to fear or greed? (Be honest. Your portfolio can’t see you, but I can.)

- Do I have a written plan? If not, today is not the day to freestyle.

- Am I making two good decisions? (Exit and reentry.)

- What’s the cost of being wrong? Missing a rebound can be expensive.

A Word on “Fancy” Timing Tools

Some strategies try to time the market using technical indicators, sentiment gauges, or leveraged products.

Regulators and investor educators frequently warn that certain complex products (like leveraged and inverse ETFs)

are designed for short-term objectives and can behave very differently over longer periods than people expect.

If the product itself is built for daily moves, using it for long-term timing can introduce extra risk and

confusiontwo things your future self will not thank you for.

So… Is Market Timing Ever Useful?

For most everyday investors, “timing” is better applied to behaviors than predictions:

- Timing your savings: invest regularly and increase contributions when possible.

- Timing your risk: reduce exposure as your need for the money gets closer.

- Timing your rebalancing: rebalance systematically, not emotionally.

That’s not as thrilling as calling the exact bottombut it’s dramatically more realistic. And realism is

underrated in a world where everyone on the internet is somehow up 400% “this week.”

Conclusion: The Goal Isn’t Perfect TimingIt’s a Durable Strategy

Market timing is hard because it asks for precision in a system built on uncertainty. You need to be right twice,

while competing with fast-moving information, institutional flows, and your own very human emotions. Meanwhile,

markets can deliver their biggest gains when the world feels the shakiest.

A durable investing strategy usually looks less like a superhero landing and more like a routine:

diversify, invest consistently, rebalance, manage risk, and keep enough cash on hand so life doesn’t force you to

sell at the worst possible moment. It’s not flashybut flashy is overrated. Consistency is how compounding does

its best work.

Educational only, not financial advice. If you’re unsure what fits your goals and situation, consider

talking with a qualified financial professional.

Experiences: What “Trying to Time the Market” Feels Like in Real Life (Extra Section)

If you’ve ever tried to time the market, you already know the emotional plotline. It usually starts with a

reasonable sentence like, “I’ll just wait until things settle down.” Then the market does what markets do: it

refuses to coordinate its schedule with your comfort level.

One common experience is the “cash trap”. Someone sells during a scary dropmaybe the news is

nonstop, maybe their portfolio feels like it’s meltingand they move to cash “temporarily.” At first, it feels

like relief. No more watching red numbers. No more anxiety. But then the market bounces. Not gently. Not with a

polite invitation. It jumps when you least expect it, and suddenly the investor is staring at higher prices with

a new fear: “What if I buy back in and it drops again?”

That’s the second half of the trap: the moment you sell, you’re no longer deciding whether to investyou’re

deciding when to be wrong publicly. If you buy back in and the market falls, you feel foolish. If you

don’t buy back in and the market rises, you feel left behind. Either way, your emotions are doing push-ups on

your attention span.

Another familiar experience is the “headline hamster wheel.” You tell yourself you’ll reenter

when there’s “good news.” But the news cycle is a machine that can always produce one more scary story. Even when

things improve, commentary often sounds like: “Yes, but what about this risk?” Market timing can become

a lifestyle where you’re always waiting for certainty in a world that doesn’t offer it.

People also report the “all-time high hesitation.” They finally work up the courage to invest,

but then the market hits a record high, and they freeze. It feels like showing up to a party after everyone has

eaten the best snacks. But markets can hit many all-time highs over long periods because growth tends to compound.

The emotional brain treats “high” as “danger,” while the long-term brain sees “high” as “normal along the way.”

And then there’s the classic: “I nailed it once, so I can do it again.” Many investors have one

lucky momentmaybe they sold before a downturn or bought during a dipand that success imprints like a movie

montage. The problem is that markets don’t reward confidence; they reward outcomes. A single good call can

encourage bigger bets, more frequent trades, and a stronger belief in a personal “signal,” even when future

outcomes don’t cooperate.

Finally, some people describe the “sleep test”. They realize that the real win isn’t beating the

market by a fraction; it’s building a strategy that lets them sleep, focus on school or work, and live their life

without turning every market move into a mood swing. That’s often where the best long-term approach begins:

less prediction, more process. Instead of asking, “What will the market do next?” they ask, “What will I do next

no matter what the market does?”

In other words, the most valuable “timing” skill isn’t calling tops and bottoms. It’s learning when to stop

negotiating with your emotions and start following your plan.