Table of Contents >> Show >> Hide

- Why Markets Really Are Hard (Even for the Pros)

- Seth Klarman’s Core Philosophy: Margin of Safety and Common Sense

- What “Markets Are Hard” Means for Everyday Investors

- How to Apply “A Wealth of Common Sense” to Your Own Strategy

- Real-World Experiences: Living the “Markets Are Hard” Lesson

- Conclusion: Markets Are Hard That’s the Point

If you’ve ever stared at your brokerage account and thought, “I have absolutely no idea what I’m doing,” congratulations you’ve just tapped into the same uncomfortable truth that legendary investor Seth Klarman has been preaching for decades: markets are hard. Not “slightly tricky,” not “mildly confusing.” Hard.

Ben Carlson’s blog A Wealth of Common Sense captured this idea perfectly in his piece “Markets Are Hard: Seth Klarman Edition,” where he used Klarman’s words to remind investors that even the smartest people in the room are humbled by uncertainty.

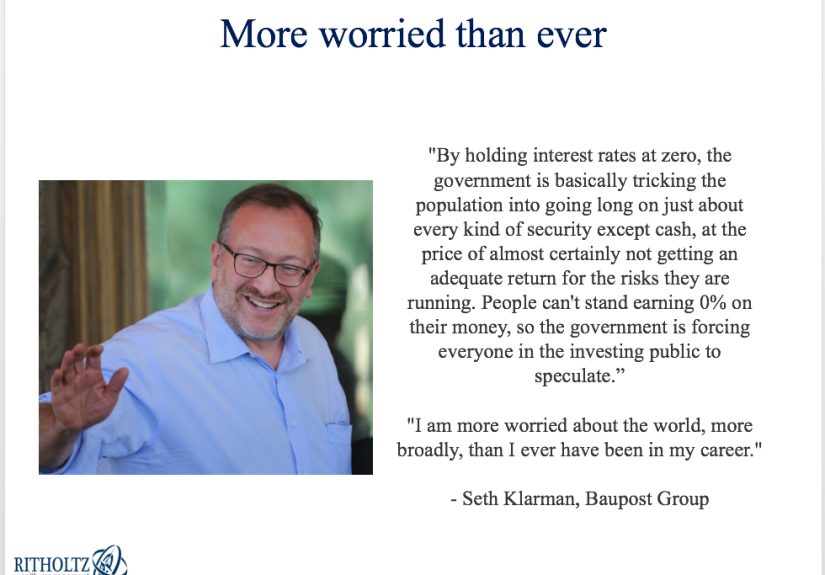

When a value-investing giant who runs tens of billions at Baupost Group says the game is difficult, the rest of us should probably put down the hot stock tips and listen.

In this article, we’ll unpack why markets are so challenging, what Seth Klarman’s “margin of safety” philosophy really means, and how you can apply his common-sense ideas to your own portfolio without needing a hedge fund, a PhD, or a crystal ball. Just a bit of patience, discipline, and a willingness to admit you don’t know everything.

Why Markets Really Are Hard (Even for the Pros)

Many investors secretly believe there’s a cheat code: the right newsletter, the right guru, the right model. But Klarman’s work and track record say the opposite. In his classic (and infamously hard-to-find) book Margin of Safety, he stresses that investing is difficult because valuation is imprecise, the future is unknowable, and humans are emotional.

Let’s break down a few reasons markets are so hard:

- The future refuses to sit still. Earnings, interest rates, politics, technology, pandemics, AI they all collide in ways that no spreadsheet fully captures.

- Prices move faster than information. By the time the story hits your favorite financial site, big investors may have already traded on it.

- Your brain is wired for survival, not for investing. Fear and greed hijack rational thinking, pushing people to buy high, sell low, and repeat.

- Short-term scores are loud; long-term outcomes are quiet. Daily price changes scream at you, while compounding quietly works in the background.

Klarman likes to remind people that the difficulty isn’t in understanding the basic math it’s in maintaining discipline when everyone around you is losing theirs. Summaries of his ideas repeatedly emphasize that avoiding big losses matters more than chasing big wins, especially in rough markets.

Seth Klarman’s Core Philosophy: Margin of Safety and Common Sense

Seth Klarman sits firmly in the value-investing tradition of Benjamin Graham and Warren Buffett, but he has his own twist: an obsessive focus on risk first, returns second.

That mindset is central to understanding why markets are hard and what to do about it.

Margin of Safety: Your Shock Absorber in a Rough Market

The concept of “margin of safety” is simple to describe and brutally hard to follow. Klarman argues that because valuation is uncertain and investors are prone to error, you should only buy an investment when it trades at a meaningful discount to your conservative estimate of its value.

Think of it like buying a house worth $300,000 for $210,000 after a thorough inspection. Even if your estimate is a little off, you’ve built in a cushion. In stock-market terms, that cushion is what protects you when earnings disappoint, sentiment shifts, or the economy hits a pothole.

According to multiple analyses of Klarman’s work, this margin-of-safety approach is less about predicting the future and more about admitting you can’t predict it.

That’s a key piece of common sense many investors ignore in the heat of a bull market.

Price Is Not the Same as Value

Another Klarman staple: price is what you pay, value is what you get. This echoes Buffett, but Klarman applies it with ruthless patience. Commentators on his philosophy consistently highlight his insistence that risk isn’t just about volatility it’s about overpaying.

Markets become especially hard when people forget this. When the price of a stock goes up, many investors assume the company is “winning.” When the price drops, they assume the business is broken. Value investors like Klarman flip that thinking: prices going down can be an opportunity, not a verdict, as long as the underlying business remains solid.

Patience, Discipline, and the Couch-Potato Portfolio

Klarman has joked that their money sometimes looks like a couch potato compared with the hyperactive trading of others.

That’s deliberate. He’s more than willing to hold large cash positions when opportunities are scarce, even if it makes him look out of step in the short term.

Many quotes attributed to Klarman boil down to a simple theme: the greatest edge you can have is a long-term orientation, plus the endurance to stick with it when markets are turbulent.

That sounds boring until you compare it with the emotional roller coaster of chasing hot stocks, meme trades, or speculative bubbles.

What “Markets Are Hard” Means for Everyday Investors

It’s easy to read about Seth Klarman and think, “Cool, but I don’t run a multi-billion-dollar hedge fund.” Fair. But the lessons behind “Markets Are Hard: Seth Klarman Edition” translate surprisingly well to regular people managing 401(k)s, IRAs, or simple brokerage accounts.

1. Accept Uncertainty Instead of Fighting It

Many investors waste enormous energy trying to forecast where the S&P 500 will be next quarter or guessing which sector will lead next year. Klarman’s philosophy suggests a different approach: accept that you don’t know, and build a portfolio that works even if your guesses are wrong.

Practically, that means:

- Diversifying across asset classes and sectors, instead of betting everything on one theme.

- Using value and quality filters, not just chasing stories or momentum.

- Keeping some dry powder (cash or short-term safe assets) for when opportunities arise.

2. Focus on Risk Management Before Returns

Articles on Klarman’s investing rules consistently emphasize his mantra: avoid big losses.

It’s not about never losing money that’s impossible. It’s about building a process that avoids catastrophic mistakes.

For individual investors, that can mean:

- Refusing to buy businesses you don’t understand, no matter how popular they are.

- Avoiding leverage just to “juice returns.” Margin debt can turn volatility into disaster.

- Keeping position sizes reasonable so one bad idea doesn’t sink the ship.

3. Embrace Boredom as a Feature, Not a Bug

Markets are hard partly because they reward behavior that feels wrong. Doing nothing sitting on your hands while prices swing feels passive. But as value investing commentators point out, patience is one of Klarman’s main superpowers.

If your portfolio strategy is sound, “boring” can be a compliment. Rebalancing once or twice a year, buying when assets you understand become cheap, and otherwise letting compounding do the heavy lifting is far more aligned with a margin-of-safety mindset than day-trading every headline.

4. Don’t Outsource Your Judgment to Narratives or Technology

Even as firms like Baupost experiment with AI as a “capable assistant,” Klarman is clear: it’s a tool, not a decision-maker.

He worries that overreliance on shortcuts whether that’s AI outputs, social-media sentiment, or hype-driven narratives can erode genuine thinking.

For an everyday investor, that means:

- Use tools for research and organization, but make your own judgment on risk and value.

- Be skeptical of any service promising “guaranteed” market-beating results.

- Remember that not having an opinion is better than having a bad, rushed one.

How to Apply “A Wealth of Common Sense” to Your Own Strategy

Ben Carlson’s blog isn’t just about clever titles; it’s about shrinking complex market realities into simple, usable ideas. When he puts Klarman’s warning that markets are hard front and center, the message is practical: design your approach assuming it will be tough.

Build a Margin-of-Safety Mindset in Three Steps

- Slow down your decisions. Before buying a stock, fund, or bond, ask: “What would have to be true for this to be cheap?” If you can’t answer clearly, you’re guessing.

- Demand a discount to fair value. You don’t have to calculate fair value to the penny, but you should at least have a rough sense of earnings power, balance-sheet strength, and competitive position. Then aim to buy only when prices look clearly favorable, not just “not terrible.”

- Always think about the downside first. What if earnings drop? What if rates stay higher than expected? What if sentiment turns? If a modest change in assumptions makes the thesis fall apart, that’s not a wide margin of safety.

Use Common Sense to Balance Your Portfolio

Klarman’s work and commentary from multiple investment writers paint a consistent picture: markets will regularly tempt you to abandon common sense.

In good times, you’ll be tempted to take more risk than you should. In bad times, you’ll want to bail out at exactly the wrong moment.

A “wealth of common sense” approach might look like:

- Having a written investment plan with target allocations and clear rules for rebalancing.

- Using low-cost, diversified funds as your core holdings and being very selective with individual stock picks.

- Matching your risk level to your actual time horizon and emotional tolerance, not to market noise.

Real-World Experiences: Living the “Markets Are Hard” Lesson

Theory is nice, but markets teach through experience sometimes very expensively. To bring the “Markets Are Hard: Seth Klarman Edition” idea to life, it helps to look at how real investors (and would-be Klarman disciples) actually encounter these lessons.

Experience 1: The Investor Who Discovered Volatility the Hard Way

Imagine an investor named Alex who started investing in a roaring bull market. Every dip was quickly bought, every growth stock seemed unstoppable, and every online community promised that “this time is different.” Alex came to believe that markets were only hard for people who “didn’t get it.”

Then the cycle turned. Interest rates rose, speculative favorites crashed, and many of the companies Alex owned went from “market darlings” to “why does this business exist?” Alex realized that he had been buying based on price momentum, not underlying value. He had no margin of safety, no framework for risk, and no plan beyond “it always comes back.”

Looking back, Alex could see that a Klarman-style mindset would have forced different questions:

- What is this business actually worth, independent of the current stock price?

- Am I paying a conservative price, or am I paying for perfection?

- If earnings disappoint or sentiment sours, do I have a cushion or am I standing on a cliff?

That painful experience became Alex’s initiation into the reality that markets are hard precisely because they lull you into thinking they’re easy, right before they remind you who’s in charge.

Experience 2: The “Boring” Investor Who Quietly Wins

Now picture Jordan, who took a different route. Influenced by Klarman’s emphasis on margin of safety and Carlson’s “wealth of common sense” framing, Jordan built a portfolio of diversified index funds and a small basket of carefully chosen value stocks. No meme trades, no options, no 10x promises.

For years, Jordan’s approach looked dull compared with friends bragging about speculative wins. But when volatility surged and high-flying names collapsed, Jordan’s drawdowns were milder. More importantly, Jordan had the confidence to stay the course because each holding was selected with risk and valuation in mind, not just excitement.

Over a full market cycle, Jordan’s “boring” strategy quietly outperformed many of the flashy approaches simply by avoiding big, permanent losses a very Klarman-esque outcome. The experience reinforced a key truth: the market is hard, but you don’t make it easier by playing a harder game. You make it easier by choosing a game with rules you can actually follow.

Experience 3: Using Tools Without Losing Judgment

Finally, consider Taylor, an analyst at a small firm that began experimenting with AI tools, much like Baupost has reportedly done.

AI helped Taylor sift through filings, detect wording changes in annual reports, and speed up basic research. But Taylor noticed a subtle risk: it was easy to start trusting the tool more than their own judgment.

Remembering Klarman’s warnings about shortcuts that dull critical thinking, Taylor decided to treat AI as a research assistant, not an investment committee. The tool could surface information, but decisions had to flow through a margin-of-safety lens: Is this business understandable? Is the price clearly favorable? What’s the downside?

Taylor’s experience highlights a modern version of the same old lesson: markets are hard, and technology doesn’t change that. It can help you gather data faster, but it can’t replace judgment, discipline, or the willingness to be patient when the crowd is restless.

Conclusion: Markets Are Hard That’s the Point

“Markets Are Hard: Seth Klarman Edition” isn’t just a clever headline from A Wealth of Common Sense. It’s a compact philosophy: markets are hard, so you must be humble; the future is unpredictable, so you must demand a margin of safety; humans are emotional, so you must build systems that protect you from yourself.

You don’t have to copy Klarman’s every move to benefit from his approach. You just need to internalize a few simple, powerful ideas:

- Focus on risk first, return second.

- Recognize that price is not the same as value.

- Use patience, discipline, and a long-term mindset as your edge.

Markets will always be hard. But with a margin-of-safety mindset and a little common sense, they don’t have to be impossible.