Table of Contents >> Show >> Hide

- First, Let’s Agree on the Vocabulary (Because Words Matter)

- Why Timing Makes Everyone Look Guilty (or Brilliant)

- Recessions Since World War II: The Timeline vs. the Term

- Bear Markets: When Stocks Throw a Full-Body Tantrum

- So… Do Presidents “Cause” Recessions and Bear Markets?

- The Overlap Story: When Recessions and Bear Markets Link Arms

- Election Years, Policy Uncertainty, and the “Narrative Premium”

- How to Read This History Without Turning It Into a Political Horoscope

- Conclusion: The Big Takeaway (No, It’s Not “Blame Whoever’s in Office”)

- Experiences Related to Presidential Terms, Recessions & Bear Markets (500+ Words)

The United States has a favorite pastime: blaming (or crediting) the President for the economy.

Gas prices go up? “Thanks, White House.” Stocks rip higher? “Genius leadership.”

A recession hits? Suddenly everyone becomes an amateur macroeconomist with a hot take and a Twitter thread.

But the relationship between presidential terms, recessions, and bear markets is less like a straight line

and more like a bowl of spaghetti: tangled, messy, and occasionally splattered on your shirt at the worst possible time.

This article untangles the timelines, explains the mechanics, and shows what history actually suggestswithout pretending any single person controls a $28+ trillion economy with a magic wand.

First, Let’s Agree on the Vocabulary (Because Words Matter)

What counts as a recession?

In everyday conversation, “recession” gets treated like a simple scorecard: two straight quarters of negative GDP and boomrecession.

Real life is messier. In the U.S., the most widely cited referee is the National Bureau of Economic Research (NBER), which dates recessions

using a broad set of indicators (output, income, employment, and more) to identify peaks and troughs in economic activity.

That’s why some recessions don’t neatly match the “two negative quarters” rule of thumb.

What counts as a bear market?

A “bear market” is typically described as a broad market decline of about 20% or more from a recent high.

Different organizations add extra details (like a minimum duration), but the spirit is the same:

prices drop, optimism evaporates, and your group chat suddenly becomes a support group.

What is a presidential “term” in economic reality?

A presidential term is a neat four-year box on a civics poster. The economy, however, does not care about neat boxes.

Policies take time to pass, time to implement, and time to show up in dataoften well after the ribbon-cutting photo op.

The result: presidents frequently inherit late-stage cycles and get judged on outcomes they didn’t fully create.

Why Timing Makes Everyone Look Guilty (or Brilliant)

Three timing quirks drive most of the confusion:

- Policy lags: Fiscal and regulatory changes can take quarters (or years) to show up in hiring, investment, and inflation.

- Recession calls are backward-looking: Official recession dating is typically confirmed after the fact, not in real time.

- Markets are forward-looking (and dramatic): Stocks often move months before economic data turns, and they can overshoot in both directions.

Translation: a recession can begin early in a term because the prior cycle was already rolling over, while the policy response credited to the current administration

might not show benefits until lateror even the next term. It’s like getting graded on a group project where half the team already turned in their part before you joined.

Recessions Since World War II: The Timeline vs. the Term

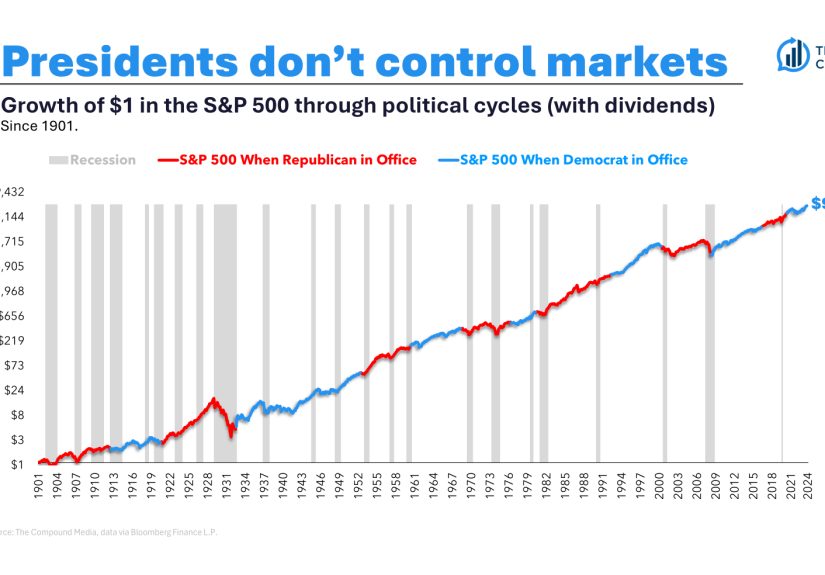

Below is a simplified view of post-1945 recessions (as dated by the NBER) and which president(s) were in office during those months.

This isn’t a “who caused what” chart; it’s a “what overlapped with whose calendar” chart.

Post-1945 U.S. Recessions and the Oval Office_ATTACHMENTS

| Recession (NBER peak → trough months) | President(s) in office during recession months | What people tend to remember |

|---|---|---|

| Nov 1948 → Oct 1949 | Harry S. Truman | Post-war adjustment, inventory swings |

| Jul 1953 → May 1954 | Dwight D. Eisenhower | Post-Korea slowdown |

| Aug 1957 → Apr 1958 | Dwight D. Eisenhower | Credit tightening, industrial dip |

| Apr 1960 → Feb 1961 | Dwight D. Eisenhower (majority), John F. Kennedy (tail end) | “Hand-off recession” politics |

| Dec 1969 → Nov 1970 | Richard Nixon | Inflation concerns, policy tightening |

| Nov 1973 → Mar 1975 | Richard Nixon (start), Gerald Ford (most) | Oil shock + inflation (“stagflation”) vibes |

| Jan 1980 → Jul 1980 | Jimmy Carter | Inflation + aggressive tightening era |

| Jul 1981 → Nov 1982 | Ronald Reagan | Volcker disinflation pain, then recovery narrative |

| Jul 1990 → Mar 1991 | George H. W. Bush | Oil spike + credit stress; “jobless recovery” memory |

| Mar 2001 → Nov 2001 | George W. Bush | Dot-com bust aftermath, investment slump |

| Dec 2007 → Jun 2009 | George W. Bush (start), Barack Obama (end) | Financial crisis, housing collapse, long scars |

| Feb 2020 → Apr 2020 | Donald Trump (45th) | Pandemic shock; fastest “down then up” economic whiplash |

Notice the pattern: major recessions often straddle administrations, and many begin when political narratives are just warming up.

That’s not a conspiracy; it’s the math of cycles, lags, and the fact that January 20 is not an economic reset button.

Bear Markets: When Stocks Throw a Full-Body Tantrum

Bear markets don’t always need a recession

Bear markets are common enough that reputable market research firms describe them as a normal part of investing. Historically, the market has recovered from them

but not on your preferred timeline, and definitely not on the same schedule as your vacation plans.

Importantly, a bear market can happen without a recession. Example: the 1987 crash was brutal in markets, but it did not turn into a classic NBER-dated recession.

Meanwhile, recessions and bear markets often travel together because corporate earnings, credit conditions, and consumer confidence tend to sink at the same time.

But “often” is not “always,” which is why blanket statements like “a bear market means recession” tend to age poorly.

A few modern examples people actually recognize

- 2000–2002 (Dot-com bust): Markets fell hard as tech valuations collapsed; the recession itself (2001) was shorter than the market pain.

- 2007–2009 (Global Financial Crisis): A recession and a bear market that felt like they were trying to set emotional records.

- 2020 (Pandemic shock): A historically short recession, plus a very fast bear market/rebound sequence.

- 2022 (Inflation + rate hikes): A bear market driven by tightening financial conditions and inflation anxiety, even without a newly dated NBER recession.

So… Do Presidents “Cause” Recessions and Bear Markets?

Presidents influence the economy, but they do not operate solo. A practical way to think about it is:

the President can steer, but the economy is a giant ship with multiple steering wheelsCongress, the Federal Reserve, global supply chains, energy markets, geopolitics,

demographics, productivity, and whatever surprise event is lurking behind the next headline.

What a president can influence (sometimes meaningfully)

- Fiscal policy: Taxes, spending, stimulus, and budget priorities (with Congress).

- Regulation: The “rules of the road” for energy, banking, health care, labor, and more.

- Trade policy: Tariffs, treaties, and supply chain incentives.

- Confidence and communication: Messaging can soothe or spooksometimes more than it “should.”

What a president cannot reliably control

- Fed policy: The Federal Reserve is designed to be independent; it reacts to inflation and employment conditions.

- External shocks: Wars, pandemics, oil embargoes, sudden credit events, and technological bubbles.

- Business-cycle gravity: Expansions don’t last forever; imbalances eventually matter.

That’s why it’s more accurate to say recessions and bear markets happen during presidential terms, not necessarily because of them.

Attribution is tempting, but history is rarely that tidy.

The Overlap Story: When Recessions and Bear Markets Link Arms

When a recession hits, corporate earnings expectations usually fall, layoffs rise, and credit conditions often tighten.

Stocks, being the caffeinated anticipators they are, tend to price in those stresses earlyand sometimes exaggerate them.

Market research frequently finds bears are shorter than bulls in duration, and recoveries can be sharpoften arriving when the news still feels awful.

This is why “I’ll get back in when things feel safer” is a strategy that sounds great in a spreadsheet and struggles in the real world.

Quick Reality Check: The Market Often Turns Before the Headlines

Recessions are typically confirmed after the fact; markets move ahead of confirmation.

This is why the most painful days in a bear market can be followed by the most powerful ralliessometimes before your brain has accepted what just happened.

Election Years, Policy Uncertainty, and the “Narrative Premium”

Election cycles layer politics on top of economics. That can raise uncertainty for businesses and investors, especially around taxes, regulation, and trade.

Markets don’t just react to data; they react to what they think policy will do to future cash flows.

One reason election-year market commentary becomes so loud is that nearly any outcome can be explained after the fact:

if the market rises, it’s because “investors love stability.” If it falls, it’s because “investors hate uncertainty.”

The truth is usually a blend of earnings expectations, interest rates, and global conditionsplus a generous splash of human emotion.

How to Read This History Without Turning It Into a Political Horoscope

If you want to be smart about presidential terms, recessions, and bear markets, here are the habits that actually help:

1) Separate timelines: economy vs. market vs. politics

The economy is measured monthly and quarterly. Markets move daily (or faster). Politics moves… emotionally.

When you treat them as one synchronized storyline, you end up confusedand possibly buying high and selling low, which is the financial version of stepping on a LEGO barefoot.

2) Focus on mechanisms, not mascots

Ask: What’s happening with inflation? Rates? Credit spreads? Corporate margins? Employment? Energy prices?

Those forces matter under any administration, and they often explain market moves better than a partisan headline.

3) Remember that “normal” includes ugly chapters

Bear markets and recessions are not proof the system is broken; they’re part of how cycles reset excesses and reprice risk.

That doesn’t make them fun. It just makes them familiar.

Conclusion: The Big Takeaway (No, It’s Not “Blame Whoever’s in Office”)

Presidential terms create clean calendar boundaries; recessions and bear markets do not.

Recessions are broad economic contractions dated with hindsight. Bear markets are investor mood swings with receipts.

Sometimes they overlap, sometimes they don’t, and they frequently straddle administrationsmaking simplistic blame (or praise) feel satisfying but misleading.

The more useful question isn’t “Which president caused the downturn?” It’s:

What conditions were buildingand how did policy, the Fed, and global events interact with those conditions?

That lens is less entertaining at parties, but it’s much better for understanding reality.

Experiences Related to Presidential Terms, Recessions & Bear Markets (500+ Words)

If you’ve ever lived through a bear market during a heated political season, you know the feeling: your portfolio is down, your news feed is on fire,

and even your uncle who “doesn’t follow markets” suddenly has a strong opinion about the yield curve.

What makes these periods uniquely intense is that they don’t just hit your moneythey hit your sense of control.

A common investor experience goes like this: the market slides 10%, and people call it “healthy.” Then it drops 15% and everyone starts saying “opportunity.”

Somewhere around 20%, the vocabulary changes to “bear market,” and the emotional thermostat breaks.

You begin to notice that every headline feels personal. A jobs report isn’t a statisticit’s a plot twist.

A policy speech isn’t just messagingit’s a potential catalyst that might decide whether you can remodel the kitchen this year.

During election-linked uncertainty, many investors describe a particular kind of mental whiplash:

one day you’re convinced “the market hates uncertainty,” the next day you’re convinced “the market loves gridlock,” and by Friday you’re convinced

the market is a sentient being that exists purely to test your patience. The reality is simpler and more annoying:

markets are discounting machines, and they can change their minds as new information arrivesespecially around interest rates, inflation, and corporate earnings.

Politics matters, but it’s rarely the only variable in the equation.

People who have been through a few cycles often describe the same hard-earned lesson:

the worst part isn’t the decline; it’s the doubt.

The doubt shows up as late-night checking, the urge to “do something,” and the temptation to turn macro headlines into a personal to-do list.

It’s also when storytelling gets dangerous. Humans crave a single cause. “It’s the president.” “It’s the Fed.” “It’s the war.” “It’s the bubble.”

Sometimes one factor dominates, but more often it’s a messy blendand the market can begin recovering even while the story still sounds terrible.

Another widely shared experience: the “missed rebound” regret.

In many bear markets, the strongest up days cluster around the most volatile periods.

Investors who jump out after a painful drop may feel temporary reliefuntil the market snaps back and the math becomes brutal.

People then face a second emotional hurdle: buying back in feels like admitting they were wrong, even if it’s the rational move.

This is why disciplined habits (like regular contributions, rebalancing rules, and time horizons that match your goals) tend to matter more than

perfectly predicting politics or recessions.

Finally, there’s the experience of perspective returningslowly, then all at once.

After the dust settles, many investors report that the period that felt like “the end of everything” often becomes “that weird time I learned what risk really feels like.”

They remember that recessions are real and painful, but also that expansions have historically been the economy’s normal state.

They remember that bear markets can be frightening, but also that markets have historically recovered.

And they remember that presidents matterespecially on policybut that the economy is bigger than any single administration.

If there’s a practical emotional takeaway, it’s this:

the goal during politically noisy market downturns isn’t to be fearless; it’s to be consistent.

Consistency doesn’t make headlines quieter, but it can keep your long-term plan from getting mugged by short-term panic.