Table of Contents >> Show >> Hide

- The Market’s Deal: Long-Term Rewards, Short-Term Chaos

- Volatility Is the Cover Charge (And It’s Not Refundable)

- The “Best Days” Problem: Why Trying to Dodge Pain Can Kill Returns

- Behavioral Finance: Your Brain Is Not a Neutral Observer

- The Other Unpopular Truth: Outperformance Is Rare (Especially After Costs)

- Why “Average” Is Actually a Superpower

- The “Cash Feels Safe” Illusion

- Acceptance in Practice: A Plan That Survives Your Emotions

- So What Is the Thing Most Investors Can’t Accept?

- Real-World Experiences: What Investors Often Go Through (And Learn)

- Conclusion

Educational content only. Not individualized financial advice.

Investors will argue about almost anythingstocks vs. real estate, dividends vs. growth, “buy the dip” vs. “wait for clarity.”

But there’s one truth that turns otherwise reasonable adults into spreadsheet-poisoned raccoons: the market does not hand out

great long-term returns in a tidy, emotionally comfortable package.

Here it is, the thing most investors simply cannot accept:

You can’t earn market-level returns without paying the price of uncertaintyand that price is volatility.

Not a little “oops” volatility. Real volatility. The kind that makes your portfolio look like it took the stairs down and the elevator up.

In other words: the market’s best features (growth and compounding) are attached to the market’s least charming personality traits

(drawdowns, whiplash headlines, and the occasional “Is capitalism over?” tweetstorm).

And you don’t get to unsubscribe from the annoying parts while keeping the gains.

The Market’s Deal: Long-Term Rewards, Short-Term Chaos

The stock market is a place where patient capital gets paid… eventually. The “eventually” is doing a lot of heavy lifting.

In the short run, prices move for a messy mix of reasons: earnings, interest rates, geopolitics, liquidity, sentiment,

positioning, algorithmic flows, fear, FOMO, and the fact that humans are extremely creative at panicking.

What many people want is a system that rewards good intentions instantly:

“I invested responsibly, so the market should behave responsibly.” Cute idea. The market did not get the memo.

What the market actually offers is more like a gym membership:

you pay consistently, the results show up slowly, and there will be days you wonder why you ever signed up.

This is why “I’m a long-term investor” is easy to say in a bull market and much harder to practice when your account balance is

down and the news sounds like a disaster movie trailer.

The long term is a wonderful place; the commute is what scares people.

Volatility Is the Cover Charge (And It’s Not Refundable)

A common mental trap is treating volatility like a malfunction.

It feels like something went “wrong” because your portfolio value dropped and nobody likes negative numbers.

But volatility isn’t a bugit’s a core feature of risk assets. It’s the admission price for the possibility of higher returns.

The SEC’s investor education materials put it plainly: risk and reward are tied together (“no pain, no gain”),

and your asset mix should match your time horizon and your ability to tolerate swings.

If you have a longer time horizon, you generally have more ability to wait out market ups and downs. If your goal is short-term,

taking less risk can make senseeven if it means lower expected returns.

This sounds obvious until you watch people with 20-year goals react to a bad quarter like they’re being chased by a bear.

Investors say they want growth, but what they often mean is: “I want growth with no discomfort.”

That product exists only in fairy tales and certain questionable ads.

The “Best Days” Problem: Why Trying to Dodge Pain Can Kill Returns

When markets get scary, the instinct is to step aside “until things calm down.”

The problem is that the market’s biggest up days often cluster around the same messy periods as the biggest down days.

If you sell after declines, you’re not just avoiding painyou’re increasing the odds you’ll miss the rebound.

Research and investor education from major firms has repeatedly shown how costly missing strong market days can be.

For example, Charles Schwab has highlighted that missing just the top 10 market days over a recent 20-year window

could cut annualized returns dramaticallynearly 40% less, in one illustration.

Fidelity has also shown that missing only a handful of the market’s best days over long periods can reduce ending wealth by roughly a third.

That’s a steep price for the emotional comfort of “doing something.”

The uncomfortable twist: those best days don’t send calendar invites.

They show up when the mood is grim, when headlines are loud, and when “waiting for clarity” feels responsible.

The market, it turns out, loves to recover precisely when many people are too stressed to participate.

A simple example

Imagine two investors with the same long-term plan. One stays invested through turbulence.

The other steps out during scary stretches and tries to jump back in “when it feels safer.”

The second investor doesn’t have to be wrong every timejust wrong during a small number of critical rebound days.

That’s how performance gaps happen: not via one giant mistake, but via a handful of emotionally-driven decisions.

Behavioral Finance: Your Brain Is Not a Neutral Observer

The stock market is a math problem, but investing is a psychology problem.

Your portfolio doesn’t live in a vacuum; it lives inside a human who checks headlines, feels emotions, and occasionally decides

the future must be predicted right now.

Behavioral finance gives names to the gremlins:

Loss aversion

Losses feel worse than gains feel good. That imbalance pushes investors to sell after declines to avoid more pain

and then hesitate to re-enteroften keeping money in “safe” places long after the danger has passed.

Some investor education materials explicitly warn that this can lead to under-diversification and missed opportunity.

Recency bias

The latest market move feels like it will continue forever.

After a big rally: “It’s unstoppable.”

After a big drop: “It’s the end.”

Neither extreme is usually true, but recency bias makes balanced planning feel boring and “out of touch.”

Overconfidence

Many investors believe they can outsmart the crowdespecially after a few wins.

But evidence suggests frequent trading can backfire. A well-known academic study examining tens of thousands of brokerage accounts

found that the households that traded the most earned meaningfully lower returns than the market over the period studied.

In plain English: being busy can be expensive.

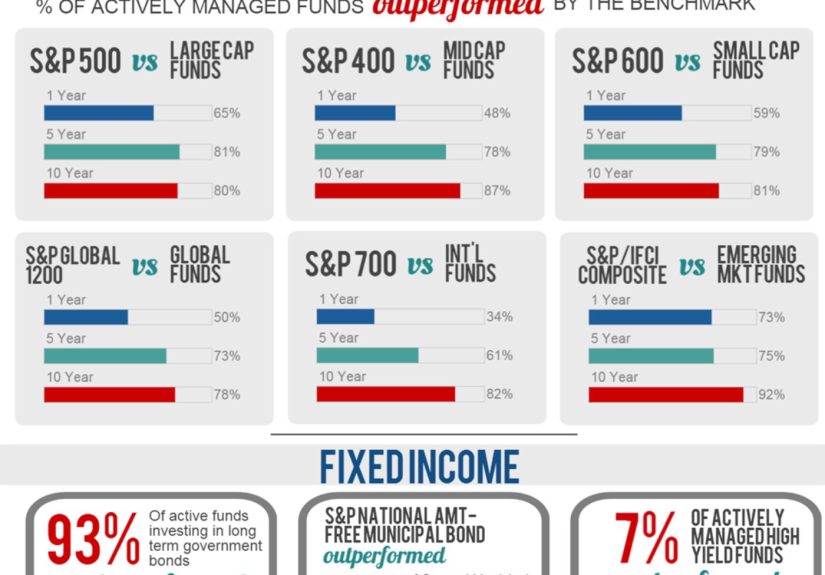

The Other Unpopular Truth: Outperformance Is Rare (Especially After Costs)

Even if you accept volatility, there’s another reality investors struggle with:

most people and most funds don’t beat broad benchmarks over long stretchesespecially after fees and taxes.

This isn’t a moral judgment; it’s the math of competition.

It’s easy to find a fund or strategy that wins in a single year. It’s much harder to find one that keeps winning

across market cycles, styles, and environments. That’s why so many investors end up chasing last year’s winners

buying what just did well, then selling when leadership changes.

Industry reporting frequently highlights this challenge. For example, commentary based on long-run comparisons has noted that

a large majority of actively managed funds have underperformed the S&P 500 over a 10-year periodfigures near nine out of ten

have been cited in some summaries.

Morningstar reporting has also described low success rates for active stock-picking funds versus passive peers in recent periods,

along with weak long-term persistence among winners.

None of this means active management is “bad.” It means the hurdle is high.

The market return is what you get by default (before costs). To beat it, someone else must lag it, and the group as a whole

has to overcome fees, trading costs, and taxes. That’s a tall order.

Why “Average” Is Actually a Superpower

Many investors secretly believe average returns are a personal failure.

But in a world where most participants underperform after costs, capturing broad market returns efficiently can be a winning outcome.

“Average” becomes impressive when you achieve it consistently and let it compound.

This is where humility becomes an investing edge.

Not the gloomy “I can’t do anything” kindmore like “I’ll focus on what I can control” humility:

- Costs (fees, spreads, unnecessary trading)

- Taxes (asset location, turnover, timing of sales)

- Diversification (not betting your future on one theme)

- Time horizon (matching risk to the timeline)

- Behavior (sticking with the plan when it’s uncomfortable)

The “Cash Feels Safe” Illusion

When volatility spikes, cash becomes emotionally attractive. It doesn’t wiggle. It doesn’t argue with you.

It also quietly loses purchasing power when inflation runs hotter than your interest rate.

Even large firms have pointed out that holding cash can carry its own risk: you may avoid market drawdowns,

but you might also fail to keep up with the rising cost of living.

Cash has an important jobemergency funds, near-term goals, and planned spending.

The mistake is treating cash as a long-term growth engine.

It’s a seatbelt, not a racecar.

Acceptance in Practice: A Plan That Survives Your Emotions

If volatility is unavoidable, the goal isn’t to eliminate discomfort.

The goal is to build a system that keeps you from turning discomfort into permanent damage.

Here’s a practical framework:

1) Set a time horizon for each goal

Retirement in 25 years is not the same as a down payment in 18 months.

Match the investment mix to the timelinethis is foundational risk management.

2) Pick a diversified allocation you can live with

Diversification doesn’t guarantee profits or prevent losses, but it can reduce the chance that one bad bet ruins your plan.

A blend of assets (often including stocks and bonds) can help manage the ride.

3) Automate contributions

Automatic investing turns discipline into a default. It helps you keep buying through ugly periods

which, inconveniently, is often when future returns are being seeded.

4) Rebalance with rules, not feelings

Rebalancing is the grown-up version of “buy low, sell high.”

It can force you to trim what ran up and add to what fellwithout requiring you to predict the future.

5) Create an “I Will Not Panic” checklist

When markets drop, do not ask, “What do I feel like doing?”

Ask:

- Has my goal changed?

- Has my time horizon changed?

- Has my ability to take risk changed?

- Is my allocation still appropriate?

- Am I reacting to headlines or to my plan?

So What Is the Thing Most Investors Can’t Accept?

It’s not a secret indicator or a missing spreadsheet cell. It’s a mindset shift:

There is no “high-return path” that avoids uncertainty.

You can reduce risk, but you typically reduce expected return.

You can chase return, but you must tolerate a bumpier ride.

You can try to time the market, but the odds of missing critical rebound days are realand the penalty can be massive.

The best investors aren’t the ones with superhuman prediction skills.

They’re the ones with a repeatable process, realistic expectations, and the emotional stamina to stay invested

when the market is doing its best impression of a roller coaster.

Accepting volatility doesn’t mean loving it.

It means recognizing it as the cover charge for participation in long-term growthand deciding, calmly,

that your plan is worth the price.

Real-World Experiences: What Investors Often Go Through (And Learn)

The ideas above feel clean on paper. Real life is messier. Here are a few common, relatable experiencesbased on patterns

financial professionals and investor education sources frequently describeshowing how acceptance (or lack of it) plays out.

1) “I’ll just wait until things settle down.”

One investor moved most of their portfolio to cash after a sharp market drop, promising to “get back in” once headlines improved.

Weeks turned into months. By the time the news felt calmer, prices had already rebounded. They re-entered slowly, still nervous,

and spent the next year feeling behind. The lesson wasn’t “never hold cash.” It was that waiting for emotional comfort is not a

reliable market signaland safety can be expensive when it keeps you sidelined during recoveries.

2) The “best fund last year” merry-go-round

Another investor loved researching funds and rotated into whichever one had the hottest recent returns.

It felt productive, like “optimizing.” But leadership changed often, and the switching created whipsaw: selling after a dip,

buying after a run-up, and paying hidden costs along the way. Eventually, they simplified: a diversified core portfolio,

fewer moving pieces, and a rule that changes require a specific reason (not just envy of last year’s winners).

Their returns improved mostly because their behavior improved.

3) Overconfidence after a winning streak

A trader had a great year picking individual stocks. The wins felt like proof of skill, so position sizes grew.

Then a market rotation hit and the same approach stopped working. Losses arrived quickly, and the stress was worse because the

investor had built a lifestyle expectation around recent results. The turning point came with a hard admission:

a few good calls do not guarantee a repeatable edge. They kept a smaller “fun money” account for active ideas and rebuilt the

rest around long-term, diversified holdings. The big change wasn’t knowledgeit was humility and risk control.

4) Panic-selling that becomes permanent

Some investors sell during scary markets planning it as a “temporary” move.

But after selling, buying back feels emotionally harder than selling did.

If prices rise, it feels like you missed out and you wait for a pullback. If prices fall, it feels like you were right and you

wait for “confirmation.” Either way, the decision drifts from tactical to permanent. Investors who escaped this loop often did

it by using structure: automatic contributions, a rebalancing rule, and fewer portfolio check-ins.

They didn’t become fearlessthey became less reactive.

5) The quiet power of a boring plan

One investor built a simple allocation matched to their timeline, automated contributions, and rebalanced twice a year.

During volatile periods, they focused on controllables: spending, savings rate, and staying diversified.

Their friends had more exciting storiesbig bets, dramatic exits, perfectly timed re-entries (at least in retellings).

But over time, the boring plan did what compounding does: it stacked small advantages. The lesson was surprisingly emotional:

acceptance feels like boredom in the moment, and like relief years later.

Conclusion

Most investing mistakes are not intelligence problems. They’re expectation problems.

If you expect returns without discomfort, you’ll keep trying to escape volatilityand that escape attempt can become your biggest cost.

Accept the market’s deal, build a plan you can stick with, and let time do what it does best: compound.