Table of Contents >> Show >> Hide

- What Counts as an “Emerging Market,” Anyway?

- The Best Part: Why Emerging Markets Can Be Worth It

- The Worst Part: The Risks That Make EM Feel Like a Roller Coaster

- How to Invest in Emerging Markets Without Losing Your Mind

- Specific Examples of “Best & Worst” in Real Life

- Common Myths That Make EM Investing Harder Than It Needs to Be

- A Practical Checklist Before You Buy

- Conclusion: The Best & Worst Part in One Sentence

- Experiences Investors Commonly Have With Emerging Markets (Extra 500-ish Words)

Emerging markets investing is a little like ordering “spicy” at a new restaurant: sometimes you get a warm, flavorful kick, and sometimes your eyes water and you start making life promises you can’t keep.

The upside is realfaster-growing economies, expanding middle classes, and companies that can “leapfrog” older infrastructure. The downside is also realcurrency swings, political surprises, liquidity hiccups, and governance issues that can turn a calm portfolio into a suspense series.

This guide breaks down the best and worst parts of emerging markets (EM) investing, with practical ways to participate without turning your retirement plan into an extreme sport.

(Quick note: this is educational, not personalized investment advice.)

What Counts as an “Emerging Market,” Anyway?

“Emerging markets” isn’t just a vibeit’s often a formal classification used by index providers and fund companies.

One widely referenced framework evaluates markets based on things like investability, accessibility, and liquidity (basically: can global investors reliably buy and sell there without unusual obstacles?).

Markets can also move between categories over time, which matters because index changes can influence capital flows and volatility.

Why the label matters for your portfolio

- Index membership drives money movement: When a country is added to (or removed from) a major index, funds that track that index may buy or sellsometimes in big waves.

- “Investable” doesn’t mean “safe”: A market can be investable and still be volatile. Conversely, a market can have great growth prospects but be tough to access.

- Definitions vary: Different indexes and fund families draw lines differently, so two “emerging markets” ETFs might not hold the exact same countries or weights.

The Best Part: Why Emerging Markets Can Be Worth It

1) Growth Potential That Can Actually Move the Needle

Many emerging economies have higher long-term growth potential than mature economiesoften driven by demographics, urbanization, productivity catch-up, and rising consumption.

When that economic progress translates into corporate earnings growth, it can create meaningful equity returns over long horizons.

Not every country will follow the same path, and growth doesn’t guarantee stock performancebut the opportunity set is large and dynamic.

Another reason EM growth can matter: emerging market and developing economies make up a large share of global activity by purchasing power (PPP) measures, meaning their economic weight is hard to ignore.

Even if you invest primarily in U.S. companies, global revenue exposure is already part of the storyEM investing is a more direct way to participate in that growth engine.

2) Diversification: Different Economies, Different Drivers

The classic reason investors add international exposure is diversification. Emerging markets can behave differently than the U.S. and other developed markets because their business cycles,

interest-rate dynamics, commodity exposure, and domestic growth drivers may not match what’s happening in New York, London, or Tokyo.

Diversification isn’t a magical shield (correlations can rise during global stress), but it can help reduce reliance on any single country’s economic narrative.

Think of it as adding more instruments to the bandstill music, but not a one-guitar concert.

3) Valuations and “Re-Rating” Opportunities

Emerging markets periodically trade at lower valuations than developed markets for long stretches, partly because investors demand a risk premium for uncertainty.

That can be frustrating… until it isn’t.

When risks ease or sentiment shifts, markets can “re-rate,” meaning valuations rise without needing heroic earnings growth.

The catch is timing: re-rating shows up whenever it feels like it, not when your calendar reminder goes off.

4) Innovation and Leapfrogging (Yes, It’s a Real Thing)

Some emerging markets adopt new technologies quickly because they’re not as tied to older infrastructure.

Digital payments, mobile banking, and app-based commerce can scale rapidly when a large population goes from “underbanked” to “super-connected” in a decade.

That kind of change can create standout companiesand occasionally entire industries that grow faster than you’d expect.

The Worst Part: The Risks That Make EM Feel Like a Roller Coaster

1) Currency Risk: Your Returns Have a Second Language

When you invest internationally, you’re not just buying stocks or bondsyou’re buying them through a currency.

Even if a company performs well locally, a weaker local currency versus the U.S. dollar can shrink your returns when converted back.

The reverse is also true: currency gains can boost your results.

Some markets also use capital controls or face restrictions that can affect repatriating money, trading access, or settlement processes.

These aren’t everyday events, but they’re part of the “emerging” package.

2) Political and Policy Surprises

Political risk in emerging markets isn’t always about dramatic headlines. It can be quieter:

a sudden tax change, new rules for foreign ownership, shifting central bank credibility, trade policy shocks, or regulations that affect key industries.

These policy moves can hit certain sectors hard, and they can arrive with less warning than investors are used to in more established systems.

3) Governance, Transparency, and Accounting Differences

Developed markets aren’t perfect, but they tend to have more consistent reporting standards and enforcement norms.

In some emerging markets, investors may face:

weaker minority shareholder protections, related-party transactions, opaque ownership structures, or uneven disclosure practices.

That doesn’t mean “everything is a scam”it means the range of quality can be wide, and the penalty for assuming “it’s fine” can be steep.

This is also why index providers monitor “investability” and “accessibility” criteria:

if a market becomes harder for global investors to access fairly and transparently, its classification and index treatment can be questioned.

4) Liquidity Risk: When “Sell” Becomes a Negotiation

Liquidity risk is the risk you can’t buy or sell quickly at a reasonable price.

Emerging markets can have thinner trading volumes, fewer market-makers, and wider bid-ask spreadsespecially in smaller countries or during periods of stress.

In practical terms, this can amplify volatility because price moves more dramatically when fewer participants are willing to trade.

5) Concentration Risk Hiding in Plain Sight

Many investors assume an “emerging markets fund” is a broad global basket with evenly spread exposure.

In reality, broad EM indexes can be heavily weighted toward a handful of countries and sectors at any given time.

That can be fine if you understand itbut surprising if you thought you were buying “the developing world” and instead got “a large slice of a few giants.”

Translation: always check top holdings, country weights, and sector breakdowns before you commit.

This one habit can prevent a lot of “Wait… why did my EM fund move like that?” moments.

How to Invest in Emerging Markets Without Losing Your Mind

Choose your vehicle: ETF, mutual fund, or active strategy?

For most long-term investors, a diversified, low-cost EM ETF or index mutual fund is the simplest route.

It reduces single-country blowups, spreads company risk across hundreds (or thousands) of holdings, and avoids the “I tried to pick the next superstar market” trap.

Active funds can add value in areas where information is uneven and governance variesif the manager is truly skilled and fees are reasonable.

But “active” is not a synonym for “better,” and higher costs create a higher hurdle to outperform over time.

Size your allocation like a grown-up (even if you feel like a daredevil)

Emerging markets can be a powerful diversifier, but they’re typically more volatile than U.S. stocks.

That means position sizing matters.

A modest, consistent allocation that you rebalance can be healthier than a dramatic bet that you abandon after the first scary drawdown.

Rebalance instead of revenge-trading

Rebalancing forces you to “sell a little high and buy a little low” in a disciplined way.

It’s the opposite of revenge-trading, which is when you try to “win it back” because your portfolio bruised your ego.

(Your ego is lovable. It is not a CFA charter.)

Understand the risks you’re actually taking

- Equity risk: business cycles, earnings, and market sentiment.

- Currency risk: exchange rates can add or subtract from returns.

- Country and policy risk: regulations, taxes, trade shocks, and political transitions.

- Liquidity and settlement risk: trading can be more expensive or less reliable in stress periods.

Don’t ignore the boring stuff: fees, taxes, and structure

International investing can involve additional costs: fund expense ratios, trading spreads, withholding taxes on dividends, and occasional operational friction.

You don’t need to memorize every detail, but you should know where the leaks can happenbecause small leaks become big problems over long time horizons.

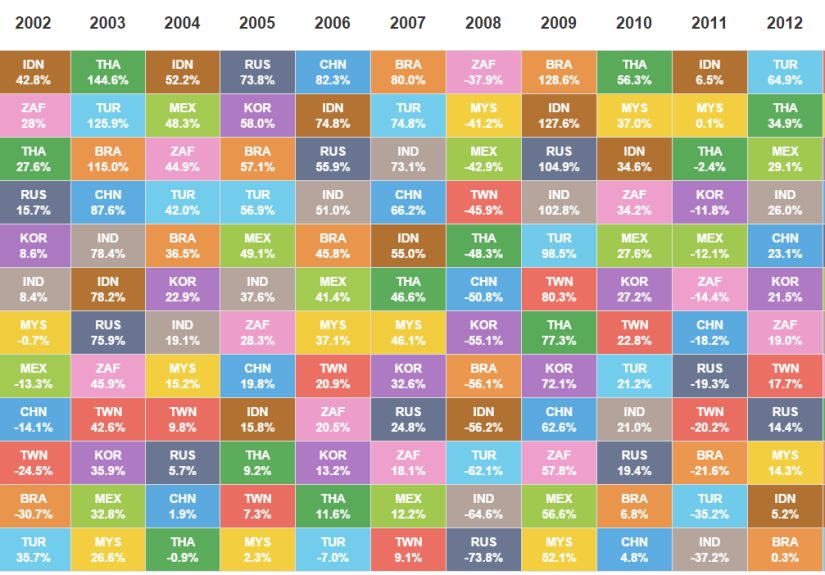

Specific Examples of “Best & Worst” in Real Life

Emerging markets often deliver their benefits and risks in the same story arc.

For example, a fast-growing consumer market can produce great companieswhile also facing currency volatility and policy changes that swing returns year to year.

Or a commodity-rich economy can enjoy booming terms of tradeuntil commodity prices fall, the fiscal outlook worsens, and investors demand a bigger risk premium.

Another common pattern: strong long-term potential paired with “event risk.”

In developed markets, surprises happen too, but emerging markets can react more sharply because liquidity is thinner and global investors may reduce exposure quickly when uncertainty rises.

Common Myths That Make EM Investing Harder Than It Needs to Be

Myth 1: “Emerging markets are always the fastest-growing investment”

Some emerging economies grow faster, but stock returns depend on valuations, earnings quality, capital flows, currency moves, and investor sentiment.

Growth helpsbut it’s not the only ingredient.

Myth 2: “Emerging markets are one thing”

Emerging markets are diverse: different political systems, central bank credibility, debt structures, export mixes, demographics, and governance standards.

Treating them as a single monolith is like reviewing “food” as a category. (Yes, pizza and kale are both food. No, they are not the same experience.)

Myth 3: “If it’s in a big ETF, it must be safe”

A broad ETF can reduce single-company risk, but it can’t remove systemic risk like currency devaluation, market closures, or policy shocks.

Indexing is a tool, not an invisibility cloak.

A Practical Checklist Before You Buy

- What’s the fund’s country concentration? Look at the top 5 countries and ask if you’re comfortable with that exposure.

- What’s the sector tilt? Tech, financials, energy, and materials can dominate at different times.

- Is the fund broad EM or something narrower? Some funds focus on “quality,” “value,” “small-cap,” or specific regions.

- What’s your time horizon? EM can punish short-term impatience and reward long-term discipline.

- How does it fit with your overall allocation? EM should complement your plan, not replace it.

Conclusion: The Best & Worst Part in One Sentence

The best part about investing in emerging markets is the chance to participate in long-run global growth and diversification; the worst part is paying for that opportunity with extra volatility, currency risk, and occasional “what just happened?” moments.

If you treat emerging markets like a long-term allocation (not a short-term prophecy), use diversified vehicles, keep position sizes reasonable, and rebalance with discipline,

you give yourself a better shot at capturing the upside without letting the downside hijack your entire portfolio strategy.

Experiences Investors Commonly Have With Emerging Markets (Extra 500-ish Words)

Investors who stick with emerging markets long enough tend to describe the experience with a mix of respect, mild disbelief, and an odd sense of pridelike finishing a marathon and immediately Googling, “Is it normal to feel like a confused superhero?”

That’s because EM investing rarely rewards the most confident person in the room. It tends to reward the most patient.

A common early experience is the “headline whiplash.” You buy an emerging markets fund because you believe in long-term growth. Two weeks later, your feed is packed with stories about elections, tariffs, central bank drama, or a currency sliding.

The market drops fast, and you learn a humbling truth: the market can re-price risk faster than you can reheat coffee.

Many investors respond by selling at the worst timethen watching the market rebound later, which is how EM teaches Lesson #1: your plan matters more than your mood.

Another experience is discovering what “diversification” really feels like. In a strong U.S. market, emerging markets can lag, sometimes for years.

That can make you question the entire pointuntil the cycle flips and EM becomes the part of your portfolio that’s quietly doing its job.

Investors who rebalance often describe this as the moment EM stops being a “bet” and starts being a “tool.”

They may trim EM after big run-ups (which feels emotionally wrong, like leaving a party early) and add after sell-offs (which feels emotionally wrong, like showing up to a party during cleanup).

But over time, that discipline can improve risk management.

Many investors also develop a sharper awareness of currency. They notice that even when companies seem fine, returns can be dragged down by exchange rates.

This can feel unfair at firstlike getting graded on a group project where the currency did none of the slides but still affected your GPA.

Eventually, investors learn to see currency risk as part of the package: it can hurt, help, or do nothing, and it’s one reason EM returns can look “messier” than U.S. returns.

Perhaps the most valuable experience is learning what you can control. You can’t control political events, commodity prices, or whether investors suddenly fall in love with (or flee from) risk.

But you can control fees, diversification, allocation size, rebalancing, and your time horizon.

Investors who embrace those controllables often say EM becomes less stressfulstill bumpy, but less emotionally expensive.

And that’s the real win: not avoiding volatility, but building a portfolio that can live with it.