Table of Contents >> Show >> Hide

- Keynes Wasn’t Just an EconomistHe Was a Real-World Money Manager

- What “Getting Fired” Means in Modern Asset Management

- Keynes’s Investing Style Would Set Off Modern Risk Alarms

- So Would Keynes Be Fired Today? The Honest Answer: “It Depends on the Client’s Spine.”

- What Would Keynes Need to Change to Keep the Job?

- What This Thought Experiment Teaches Modern Investors

- Conclusion

- Bonus: of Modern Money-Manager “Experiences” That Sound Like Keynes’s Trial by Committee

Picture this: John Maynard Keynes walks into a modern investment committee meetinglanyard on, PowerPoint ready,

and a performance chart that looks like a roller coaster designed by a caffeinated economist.

The chair clears their throat and says the sentence every manager dreads: “So… let’s talk about the last twelve months.”

It’s a fun thought experiment, but it’s also a serious question about how modern finance works:

Would Keynes’s stylebold, concentrated, and occasionally stomach-churningsurvive today’s career-risk culture?

Or would he be escorted out by compliance before he finished saying “animal spirits”?

Let’s run the trial the way modern markets would: not just on brains, but on benchmarks, drawdowns, governance,

and the unforgiving reality that investors often want “long-term” results by next quarter.

Keynes Wasn’t Just an EconomistHe Was a Real-World Money Manager

Keynes is famous for reshaping macroeconomics, but he also spent decades doing something even more emotionally difficult:

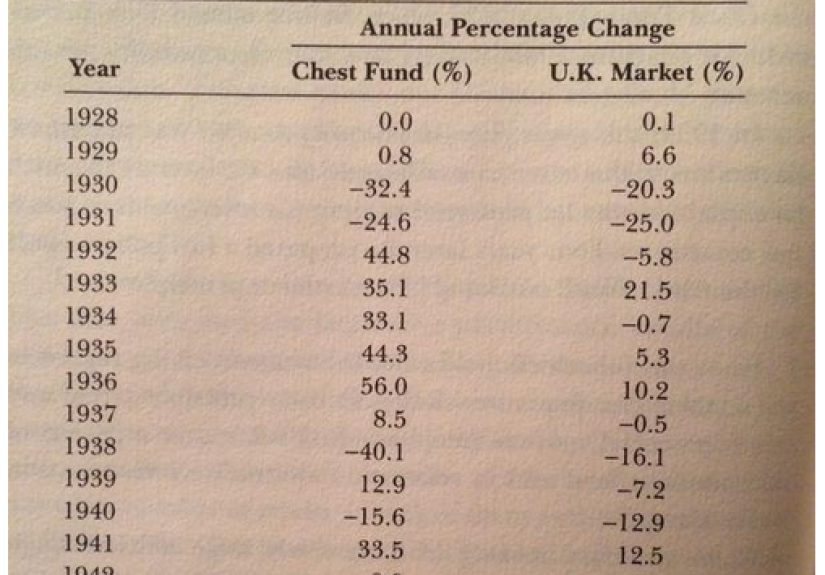

managing money through chaos. Historical research based on archived records shows he ran institutional portfolios,

including a Cambridge college endowment, and applied a distinctly hands-on approachstudying companies, writing internal memos,

and making big, high-conviction moves rather than spreading bets like peanut butter.

His investing story matters because it’s not a tidy “always right” legend. It’s a human investing story:

early stumbles, painful losses, a major strategy evolution, and then strong long-run results.

That arc is exactly what makes the “would he be fired?” question so modern.

What “Getting Fired” Means in Modern Asset Management

Today, money managers don’t usually get fired because they’re dumb. They get fired because they’re

out of sync with the mandateor because the client’s patience expires before the strategy’s edge shows up.

In institutional investing, termination is often a process, not a surprise: “watch lists,” probation periods,

and increasingly intense reviews that feel like a performance evaluation and a root canal happening at the same time.

The Modern Scorecard: It’s Not Just Returns

- Relative performance: Underperforming the benchmark (or peers) over 1-, 3-, and 5-year windows can trigger scrutiny

even if the strategy is behaving exactly as designed. - Drawdowns: A big drop can matter more than long-run averages because it drives client behavior, headlines, and board anxiety.

- Tracking error and “career risk”: The more a manager deviates from the benchmark, the more likely they’ll look brilliantor unbearable.

Many institutions say they want differentiated skill, but they often punish the discomfort that comes with it. - Style drift: If you’re hired as a value investor and quietly become a growth investor, allocators noticeand the exit interview begins.

- Operational and compliance risk: In the U.S., investment advisers operate under fiduciary expectations and marketing rules

that put major weight on disclosure, documentation, and substantiationnot just “trust me, I’m Keynes.” - Key-person risk: If the “genius” is the strategy, what happens when the genius is sick, distracted, or just having a bad year?

The uncomfortable truth: modern termination decisions are often as much about

governance optics as they are about investment truth. Nobody wants to be the person who kept a volatile manager…

right up until the newspaper called.

Keynes’s Investing Style Would Set Off Modern Risk Alarms

Based on the historical record analyzed by finance scholars and professional organizations, Keynes’s portfolios were

active, unconventional, and sometimes highly concentrated. He was willing to look wrong for a while,

and he wasn’t shy about making big calls. In today’s world, that immediately raises a question:

Is the client truly prepared for a strategy that can lagsometimes painfullybefore it wins?

1) Early Keynes: The “This Is Fine” Meme, but With Markets on Fire

Early in his investing career, Keynes experimented with approaches that look like “macro timing” in modern language.

Historical reconstructions of his activity indicate he didn’t consistently demonstrate market-timing ability in those early phases.

Translation: even Keynes had a period that would make a modern consultant write, “Performance headwinds observed; monitor closely.”

He also took positions that could be volatilesometimes extremely volatile.

In a modern institutional setting, significant volatility can trigger policy limits, risk committee meetings,

and that dreaded phrase: “This isn’t what we hired you for.”

2) Then Keynes EvolvedHard

The most investor-relevant part of Keynes’s story is that he changed his process.

Research on his records suggests he pivoted away from trying to outguess the entire market and moved toward something closer to

bottom-up stock selection: buying businesses he understood, holding them with patience, and concentrating capital in his best ideas.

That shift sounds familiar because it resembles what many modern investors would call

“high-conviction fundamental investing,” with characteristics that often overlap with

value tilts and a willingness to hold through “thick and thin.”

So Would Keynes Be Fired Today? The Honest Answer: “It Depends on the Client’s Spine.”

Whether Keynes survives in 2026 asset management comes down to one thing:

time horizon matched to strategy. In the right environment, he could be celebrated.

In the wrong one, he could be fired before his thesis finished unfolding.

Scenario A: The Typical Modern Client (Short Patience, Tight Benchmarks)

If Keynes were managing money for a client that reviews performance quarterly,

expects steady benchmark-like behavior, and panics when tracking error is high,

he’d have a problembecause his style would likely produce periods of uncomfortable divergence.

In that world, Keynes would face three modern hazards:

- The optics problem: Concentrated portfolios can look reckless when they’re temporarily down.

- The committee problem: Committees love processuntil process produces red numbers.

- The “why don’t you just own the index?” problem: The more you differ, the more you must explain.

Under this regime, yesKeynes might be fired early, not because he lacked skill,

but because his approach demands a level of patience that many modern mandates don’t truly allow.

Scenario B: The Right Modern Home (Endowments, Patient Capital, Clear Risk Budgets)

Put Keynes in a setting that can tolerate real active riskthink certain endowments,

foundations, or long-horizon pools that explicitly budget for tracking errorand the story changes.

In that environment, his strengths look very modern:

- Conviction: He was willing to be different, not just slightly different.

- Adaptability: He changed his process when evidence demanded itrare then, rare now.

- Communication: He documented thinking through memos and reviews, the ancestor of today’s “investment thesis write-up.”

- Long-term orientation: He acted like time was an asset, not an inconvenience.

In a patient setting, Keynes wouldn’t be fired for volatility; he’d be hired because he could withstand it.

He might even become a star “differentiated alpha” managerassuming he also survived modern compliance training.

What Would Keynes Need to Change to Keep the Job?

If Keynes time-traveled into today’s asset management industry, he wouldn’t need to abandon bold investing.

He’d need to translate it into modern systemsbecause in 2026, the market doesn’t just ask, “Were you right?”

It asks, “Can you prove you weren’t reckless on the way there?”

He’d likely adapt in five practical ways

- Define the mandate in writing: A clear investment policy statement that says,

“Expect volatility and deviation; judge us over full cycles.” - Risk budgeting: Instead of “big bets because I’m brilliant,” it becomes

“big bets because the portfolio has explicit risk capacity for them.” - Liquidity discipline: Modern allocators care deeply about liquidity under stress. Keynes would need to show

he can meet redemptions without selling the crown jewels at the worst time. - Process transparency: Not revealing every trade, but consistently documenting why positions exist

and what would change his mind. - Compliance-first marketing: In the U.S., marketing and performance presentation are regulated.

Keynes would need to learn that “trust my genius” is not a disclosure policy.

What This Thought Experiment Teaches Modern Investors

“Would Keynes be fired?” is really a mirror held up to modern finance. It highlights how often the industry says it wants

long-term thinking while structurally rewarding short-term comfort.

Three lessons worth stealing from Keynes (without stealing his drawdowns)

- Match strategy to capital: If you can’t hold through ugly periods, don’t hire a manager whose edge

requires holding through ugly periods. - Measure the process, not just the scoreboard: Great strategies can lose for a while. Bad strategies can win for a while.

The job is separating “temporary pain” from “broken thesis.” - Beware the tyranny of the benchmark: Benchmarks are useful tools, but they can become cages.

Some of the best long-run outcomes come from being willing to look different.

Conclusion

Would Keynes have been fired as a money manager today? In many modern settings, yeshe could have been fired early,

especially during periods of sharp underperformance or uncomfortable volatility. Not because he was incompetent,

but because his style demanded patience, risk tolerance, and governance clarity that many clients claim to have but don’t.

But in the right mandateone built for long horizons and honest active riskKeynes could thrive.

The real punchline is this: the world didn’t get less Keynesian; it just got more quarterly.

And if you force long-term investors to behave like short-term judges, you’ll fire a lot of talent right before it pays off.

Bonus: of Modern Money-Manager “Experiences” That Sound Like Keynes’s Trial by Committee

A large pension plan hires an equity manager with a simple pitch: “We buy undervalued businesses and hold them patiently.”

The plan’s investment policy explicitly allows meaningful tracking error because leadership wants something

different from the index. Everyone is happyuntil the first year of underperformance shows up.

At the next quarterly review, the manager arrives with a calm explanation: fundamentals improved, valuations got cheaper,

and the team added to positions. The risk officer arrives with a different document: a chart showing the manager

underperformed the benchmark for four straight quarters and now sits in the bottom quartile of peers.

The committee members nod politely at the “fundamentals” slides, then stare lovingly at the peer ranking like it’s a report card.

Someone asks the most modern question imaginable: “Why can’t you just underperform… less?”

It’s meant as a joke, but it lands like a performance mandate. Another member asks whether the strategy “still works,”

as if markets provide warranty coverage. A third wonders aloud if the manager’s process has “drifted,”

even though the portfolio looks exactly like it did in the original pitchcheap companies, concentrated bets,

and a deliberate refusal to chase what’s currently popular.

This is where Keynes would recognize the room immediately.

He spent years defending equity exposure when conservative institutions preferred bonds and certainty.

In modern form, the same debate happens with different labels: “risk budget,” “downside capture,” “factor exposure,”

and “portfolio construction.” But the emotional center is identical: institutions love the idea of boldness

until boldness produces discomfort.

Many firms handle this moment with a “watch list.” The manager is told, gently, that performance will be monitored more closely.

The manager hears: “We’re halfway to firing you.” The plan sponsor tells stakeholders they’re being prudent.

Behind the scenes, staff begin collecting replacement candidatesusually those with strong recent performance,

because nothing says “disciplined long-term investing” like hiring yesterday’s winner.

In some cases, the manager gets terminated at the worst possible time: valuations are lowest, sentiment is bleak,

and the strategy’s expected returns are actually improving. The plan locks in the pain, hires a new manager

with a different style, and then watches the old manager rebound elsewherenow that the market cycle has turned.

Everybody learns the wrong lesson: “That manager was risky.” The real lesson was governance:

the plan’s risk tolerance existed in the policy manual but not in the decision-making muscle.

If Keynes were in that meeting, he’d likely argue that the job is not to eliminate discomfort; it’s to be paid for bearing it.

Modern institutions can still do thatwhen their mandates are honest, their horizons are real,

and their committees can endure being temporarily unpopular with their own performance dashboards.