Table of Contents >> Show >> Hide

- What Does “Investing in Freedom” Mean?

- Why Emerging Markets Make This Conversation So Interesting

- The Problem With Market-Cap Weighting Alone

- How Freedom-Weighted Investing Works

- Why Freedom May Matter for Returns

- Freedom Investing Is Not the Same as ESG

- What Investors Should Like About the Freedom Thesis

- The Risks: Because Every Investment Thesis Needs a Seatbelt

- How to Think About FRDM in a Portfolio

- Specific Example: Why Taiwan and South Korea Matter

- Why “Talk Your Book” Is the Right Phrase

- Practical Lessons for Investors

- Experience-Based Reflections on Investing in Freedom

- Conclusion

Every investor has a “book.” Not the leather-bound kind sitting on a mahogany desk next to a globe and a suspiciously dramatic lamp, but a set of beliefs about how the world works. Some people believe in dividends. Some believe in innovation. Some believe in low-cost index funds, global diversification, and checking their portfolio less often than they check the fridge. “Talk Your Book: Investing in Freedom” is about a different but increasingly important idea: what if freedom itself is an investable factor?

The phrase “talk your book” usually means explaining the investments you own, like a polite version of saying, “Here is why my portfolio is brilliant and definitely not just emotionally attached to last year’s winners.” In this case, the “book” is the investment thesis behind freedom-weighted emerging markets: the belief that countries with stronger personal liberties, rule of law, property rights, open markets, and transparent institutions may create better long-term conditions for businesses and investors.

This idea became especially visible through conversations around the Freedom 100 Emerging Markets ETF, commonly known by its ticker, FRDM. The fund seeks to track an index that weights emerging market countries based on personal and economic freedom metrics rather than pure market capitalization. In plain English: instead of simply giving the biggest slice of the pie to the biggest markets, it asks whether the kitchen has clean rules, working lights, and a chef who will not suddenly confiscate the oven.

What Does “Investing in Freedom” Mean?

Investing in freedom is not just a slogan stitched onto a tote bag for finance conferences. It is an investment framework that considers whether a country’s institutions support human choice, business formation, capital protection, innovation, and fair competition. The idea is that freer societies may be better positioned to attract entrepreneurs, protect investors, enforce contracts, and allow companies to adapt when conditions change.

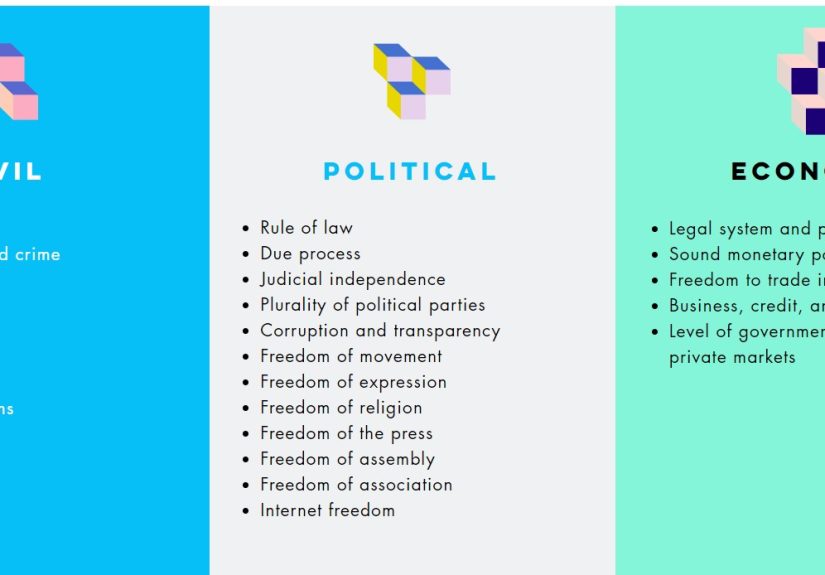

Freedom, in this context, usually blends two major categories: personal freedom and economic freedom. Personal freedom includes things like rule of law, safety, freedom of expression, civil society, movement, and basic individual rights. Economic freedom includes property rights, sound money, lighter but reliable regulation, open trade, and the ability to start and run businesses without wrestling a mountain lion made of paperwork.

The Human Freedom Index, published by the Cato Institute and the Fraser Institute, measures freedom across a broad set of personal and economic indicators. Its 2025 edition uses 87 indicators across 165 jurisdictions, including areas such as rule of law, security, movement, expression, legal systems, sound money, international trade, and regulation. That matters for investors because these are not abstract debate-club topics. They shape how companies operate, how shareholders are treated, and how predictable a market feels when things get spicy.

Why Emerging Markets Make This Conversation So Interesting

Emerging markets are the financial world’s adventure section. They can offer faster growth, younger populations, expanding middle classes, and attractive valuations. They can also bring political uncertainty, currency swings, weaker accounting standards, capital controls, liquidity issues, and the occasional regulatory plot twist that arrives with no warning and no snacks.

Traditional emerging market indexes are usually market-cap weighted. That means the largest public companies and the largest markets often receive the biggest weights. Market-cap weighting is simple and efficient, but it does not ask whether a country has strong civil liberties, reliable courts, open markets, or investor-friendly governance. It just asks, “How big are you?” which is useful, but not exactly a full personality test.

The MSCI Emerging Markets Index, for example, captures large- and mid-cap companies across emerging market countries and covers about 85% of the free float-adjusted market capitalization in each country. As of April 30, 2026, its top constituents included Taiwan Semiconductor Manufacturing, Samsung Electronics, SK Hynix, Tencent, and Alibaba. That shows how modern emerging markets are no longer just commodity exporters and old-school banks. They are deeply tied to semiconductors, technology platforms, manufacturing, finance, and consumer growth.

The Problem With Market-Cap Weighting Alone

Market-cap weighting has one big advantage: it lets the market decide. Investors do not need to forecast which country will grow faster or which government will behave better. The index simply owns more of what has already become large. That is elegant, cheap, and hard to beat over time.

But there is a catch. In emerging markets, the biggest markets are not always the freest markets. A country can have huge companies while also having weak shareholder protections, unpredictable regulation, censorship, state influence, or capital restrictions. That does not automatically make every company in that country a bad investment, but it does mean investors may be taking risks that are not fully visible in a simple valuation chart.

Imagine buying a beautiful apartment at a discount, only to discover the building rules are rewritten every Tuesday by a committee that does not believe in door locks. That is the kind of governance risk freedom-focused investors are trying to avoid.

How Freedom-Weighted Investing Works

A freedom-weighted strategy starts with a different question: which emerging markets offer better institutional foundations for growth? The Freedom 100 Emerging Markets ETF seeks to track the Life + Liberty Freedom 100 Emerging Markets Index, using personal and economic freedom metrics as primary factors in its country selection and weighting process.

Instead of simply copying the largest emerging market exposures, the strategy gives greater weight to countries with stronger freedom scores. Countries with lower freedom scores can receive smaller allocations or be excluded. The result is a portfolio that may look very different from a standard emerging market benchmark.

As of mid-May 2026, FRDM’s country exposures were heavily tilted toward Taiwan and South Korea, with meaningful allocations to Chile, Poland, Brazil, Malaysia, South Africa, Thailand, Mexico, the Philippines, and Indonesia. The fund also reported a high active share versus the MSCI Emerging Markets Index, meaning its holdings differ significantly from a traditional benchmark. Translation: this is not your average emerging markets smoothie. It has different ingredients, a different recipe, and probably more opinions.

Why Freedom May Matter for Returns

The investment case for freedom is built on a practical chain of logic. Stronger rule of law can help protect property. Better legal systems can improve contract enforcement. Open trade can expand opportunity. Sound money can reduce uncertainty. Freedom of expression and information can help markets process reality faster, even when reality is wearing clown shoes.

Companies do not grow in a vacuum. They grow inside systems. A business operating in a country with reliable courts, transparent regulations, and respect for shareholders may have more room to innovate and compound capital. A business operating under unpredictable political pressure may still succeed, but investors may demand a higher risk premium because the rules can change quickly.

This is why freedom-weighted investing sits somewhere between values-based investing and risk-based investing. Yes, it can appeal to investors who want their money aligned with democratic values and human rights. But it is also a hard-nosed investment argument: governance, property rights, and personal liberty can affect cash flows, valuations, and long-term market confidence.

Freedom Investing Is Not the Same as ESG

Many investors hear “values” and immediately think ESG. But freedom-weighted investing is not exactly the same thing. ESG typically focuses on environmental, social, and governance characteristics at the company level. Freedom investing focuses more on country-level institutions: personal liberties, economic openness, rule of law, and protection from coercion.

That difference matters. A company can score well on certain ESG metrics while operating in a country with weak political freedoms. A freedom-weighted framework asks whether the broader system allows individuals, entrepreneurs, workers, journalists, courts, and investors to function with meaningful independence.

In emerging markets, this country-level lens can be especially important. Political risk can overwhelm company fundamentals. A great company may struggle if its home market faces sanctions, capital controls, arbitrary regulation, or a collapse in investor trust. Even the best boat has problems when the ocean turns into soup.

What Investors Should Like About the Freedom Thesis

1. It Adds a Governance Filter

Traditional emerging market funds may own countries with very different levels of transparency and investor protection. A freedom-based approach tries to reduce exposure to markets where political and civil risks are unusually high.

2. It Creates Differentiated Exposure

Because freedom weighting differs from market-cap weighting, the portfolio may hold more of certain countries that are underrepresented in standard benchmarks. Taiwan, South Korea, Chile, and Poland may receive more attention than they would in a broad cap-weighted emerging market fund.

3. It May Align Money With Beliefs

Some investors do not want their emerging market allocation dominated by countries where civil liberties are weak. Freedom investing gives them a way to express that preference without abandoning the asset class entirely.

4. It Focuses on Long-Term Institutions

Economic growth is not only about population size or GDP headlines. Institutions matter. Property rights, courts, capital markets, education, innovation, and open information flows all help determine whether growth can become shareholder value.

The Risks: Because Every Investment Thesis Needs a Seatbelt

Freedom-weighted investing sounds appealing, but it is not magic. No ETF walks across water, cures underperformance, and makes your coffee. Investors still need to understand the risks.

First, freedom-focused funds may underperform traditional emerging market funds when excluded or underweighted countries perform well. If a less-free market has a huge rally, a freedom-weighted strategy may miss much of it. That is not a bug; it is part of the design. But investors must be emotionally ready for it, because nothing tests conviction like watching the thing you avoided go up 40% while your portfolio politely clears its throat.

Second, concentration risk matters. If a freedom-weighted fund has large exposure to Taiwan and South Korea, it may be highly sensitive to semiconductor cycles, technology demand, currency moves, and regional geopolitical risks. Different does not automatically mean safer. Sometimes different just means you have swapped one set of risks for another set wearing nicer shoes.

Third, methodology risk is real. Freedom scores depend on data, definitions, and weighting systems. Measuring liberty is important, but it is not as clean as measuring a stock price. Reasonable people can debate how much weight to give rule of law versus regulation, or whether recent political changes are reflected quickly enough.

Fourth, emerging market risk never disappears. Investors may still face currency volatility, liquidity challenges, foreign market regulation, accounting differences, tax issues, and geopolitical uncertainty. ETFs also trade throughout the day, so their market prices can differ from net asset value, especially during volatile periods.

How to Think About FRDM in a Portfolio

For many investors, a freedom-weighted emerging market fund is best understood as a satellite allocation rather than a full replacement for global diversification. It can sit beside broad U.S. and international equity funds, offering a more opinionated approach to emerging markets.

One simple framework is to ask three questions. First, do you want emerging market exposure at all? Second, do you want that exposure to be broad and market-cap weighted, or filtered by institutional quality? Third, are you comfortable being meaningfully different from the benchmark?

If your answer to the third question is “absolutely not, I panic when my portfolio looks different from my neighbor’s,” then a freedom-weighted strategy may cause unnecessary stress. But if you believe institutions matter and you are comfortable with tracking error, the idea becomes much more interesting.

Specific Example: Why Taiwan and South Korea Matter

Taiwan and South Korea are useful examples because they combine emerging market classification with deep technology ecosystems. Taiwan is central to global semiconductor manufacturing, while South Korea is home to major companies in memory chips, electronics, autos, batteries, and advanced manufacturing.

These markets also score better on many institutional and personal freedom measures than several other emerging economies. A freedom-weighted approach may therefore allocate more capital to them, especially when compared with indexes that are more heavily influenced by the size of China’s market.

However, this exposure is not risk-free. Taiwan faces geopolitical risk. South Korea faces cyclical export risk and corporate governance debates. Semiconductor-heavy portfolios can swing when global demand for chips changes. So the freedom thesis should not be confused with a guarantee. It is a lens, not a crystal ball.

Why “Talk Your Book” Is the Right Phrase

The beauty of “Talk Your Book: Investing in Freedom” is that it forces investors to be honest. Every portfolio is a statement. A total U.S. market fund says, “I believe in the broad productivity of American capitalism.” A global market-cap fund says, “I do not know who will win, so I will own the world.” A dividend portfolio says, “Please send cash, preferably quarterly.”

A freedom-weighted emerging market portfolio says, “I believe the quality of a country’s institutions matters enough to shape where my capital goes.” That is a book worth talking about because it connects investment mechanics with political economy, history, governance, and personal values.

Practical Lessons for Investors

The first lesson is that benchmarks are not neutral. They are rules-based portfolios built on assumptions. Market-cap weighting assumes size should determine weight. Freedom weighting assumes institutions should influence weight. Equal weighting assumes every holding deserves the same starting line. None of these is perfect. Each one tells a story.

The second lesson is that low valuation alone is not enough. A market can be cheap for a good reason. If investors fear regulation, expropriation, capital controls, or weak shareholder rights, a low price-to-earnings ratio may be less of a bargain and more of a warning label.

The third lesson is that values and returns do not have to live in separate bedrooms. Investors can care about freedom and still ask rigorous questions about performance, fees, diversification, liquidity, and risk. In fact, they should. A noble thesis with poor implementation is still poor implementation.

Experience-Based Reflections on Investing in Freedom

One of the most useful ways to understand “Investing in Freedom” is to imagine the experience of a long-term investor reviewing an emerging markets portfolio during a period of global uncertainty. At first, the investor may look only at performance charts. Which fund is up? Which fund is down? Which one has the smoothest line? This is normal. Humans love charts because charts look official, even when they are quietly laughing at our confidence.

But after spending more time with international investing, the investor starts noticing that returns are not created by numbers alone. Behind every stock market is a legal system, a currency regime, a political structure, a culture of entrepreneurship, and a relationship between citizens and the state. When those systems work well, companies may have room to grow. When those systems weaken, even strong businesses can face sudden obstacles.

Consider an investor who bought a broad emerging market fund years ago because it seemed diversified. Later, they discover that a large portion of the fund is concentrated in a few countries and mega-cap companies. Some holdings are in markets where the government can heavily influence corporate decisions. Others are in countries with stronger legal institutions but smaller representation in the index. The investor realizes that “emerging markets” is not one thing. It is a crowded airport with many gates, several delayed flights, and at least one person arguing with the luggage scale.

This is where the freedom lens becomes practical. It gives the investor another checklist. Does this country protect property rights? Are minority shareholders treated fairly? Can businesses access capital? Is information allowed to flow? Are courts reasonably independent? Can entrepreneurs build without constantly wondering whether the rulebook will be thrown into a volcano?

These questions do not produce perfect answers, but they improve the conversation. Instead of asking only, “Is this market cheap?” the investor asks, “Why is it cheap, and what risks am I being paid to accept?” Instead of asking only, “Which country has the biggest GDP?” the investor asks, “Which country gives businesses and citizens enough freedom to turn growth into durable shareholder value?”

Another experience investors often have is emotional discomfort from tracking error. A freedom-weighted strategy can look very different from a standard emerging markets benchmark. When it outperforms, the investor feels like a genius philosopher with a brokerage account. When it underperforms, the same investor may wonder whether freedom is overrated and whether the benchmark is smirking.

That is why position sizing matters. A freedom-focused ETF may be easier to hold when it plays a clear role in the portfolio. It can be a complement to broad global exposure, not a heroic all-in bet. Investors who understand this are less likely to panic when short-term results differ from the index.

The final experience is more personal. Some investors simply feel better knowing their capital is tilted toward countries with stronger civil and economic freedoms. That feeling alone should not replace due diligence, but it is not meaningless. Money is not just math. It is stored effort, deferred consumption, and a quiet vote for the systems we believe can create a better future.

Investing in freedom, at its best, is not about pretending the world is simple. It is about admitting the world is complicated and building a portfolio that reflects more than yesterday’s market capitalization. It says that institutions matter, incentives matter, human rights matter, and long-term investors should pay attention to the soil in which companies grow. After all, even the strongest tree has a tough time compounding in bad soil.

Conclusion

“Talk Your Book: Investing in Freedom” is more than a catchy title. It is a reminder that every investment strategy carries a worldview. Freedom-weighted investing argues that personal liberty, economic openness, property rights, rule of law, and transparent institutions are not just moral preferences; they may also be practical ingredients for healthier capital markets.

This does not mean investors should blindly buy any fund with the word “freedom” in the name. Fees, holdings, valuation, diversification, liquidity, and risk still matter. But it does mean investors should think carefully about what their emerging market exposure actually owns. A portfolio is not only a spreadsheet. It is a map of assumptions.

For investors seeking emerging market exposure with a stronger institutional-quality filter, freedom-weighted investing offers a thoughtful alternative. It may not win every year, and it will not eliminate risk, but it asks one of the most important questions in global investing: where can capital, people, and ideas move with the greatest chance of flourishing?