Table of Contents >> Show >> Hide

- A 20% Drop Is Not a Tiny Correction. It Is a Real Shock.

- What Homeowners Feel First

- What Sellers and Buyers Do Next

- What Happens to the Broader Economy

- Does a 20% Drop Automatically Mean Another 2008?

- What Different People Should Worry About Most

- What Households Should Actually Do in This Scenario

- Experiences From a 20% Housing Price Drop

- Final Thoughts

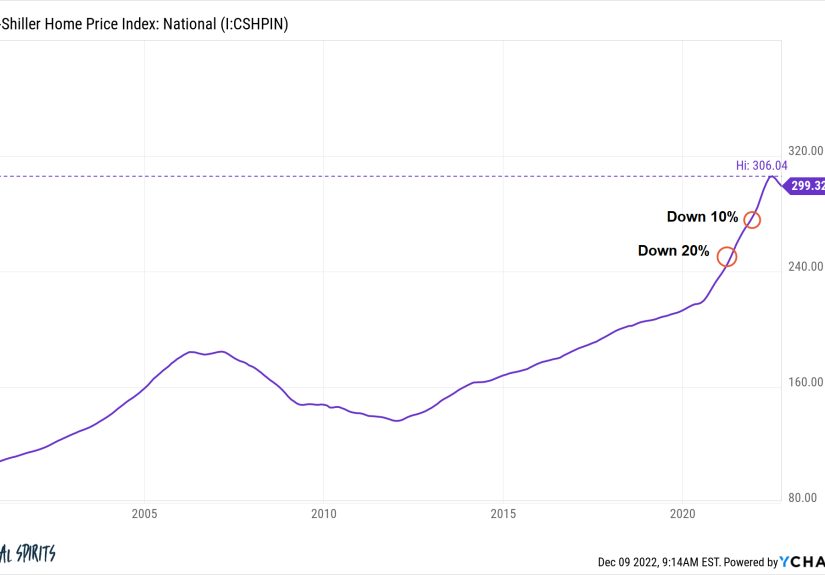

Let’s say the unthinkable happens, or at least the thing that makes homeowners stare at Zillow like it personally offended them: housing prices fall 20%.

That kind of drop is big enough to change dinner-table conversations, real estate listings, lender mood swings, and possibly the tone of every family group chat in America. It is not just a number on a chart. It can change how much equity people have, whether they can refinance, whether they can move, how much confidence buyers have, and how much the broader economy feels like wearing sweatpants for a while.

But here is the important part: a 20% drop does not hit everyone the same way. For some people, it is painful but manageable. For others, it can feel like the financial version of stepping on a Lego in the dark. The real outcome depends on when you bought, how much you put down, what kind of mortgage you have, whether you need to sell, and whether the economy is also struggling at the same time.

So what really happens if housing prices fall 20%? Let’s walk through it without panic, without doom confetti, and without pretending every homeowner is living the exact same story.

A 20% Drop Is Not a Tiny Correction. It Is a Real Shock.

In housing, a 20% decline is not a cute little “market adjustment.” It is a major repricing event. Home values do not usually move with the speed of meme stocks or crypto on espresso. Real estate is slower, heavier, and deeply tied to mortgages, jobs, confidence, and local supply.

When prices fall that much, it usually means one or more things are happening at once: affordability has cracked demand, sellers have lost leverage, credit may be tightening, or the broader economy is weakening. Sometimes it starts with high mortgage rates. Sometimes it starts with too much speculative buying. Sometimes it starts with job losses. Sometimes it is a lovely cocktail of all three.

A national 20% decline would also matter more than a local one. If one overheated market cools off, people call it regional pain. If home prices broadly fall by 20%, that starts affecting household balance sheets, consumer behavior, mortgage markets, and business confidence across the country. In other words, it stops being just a real estate story and starts auditioning for the role of economic headline.

What Homeowners Feel First

Your Mortgage Payment Usually Does Not Change, but Your Net Worth Does

If you already own a home with a fixed-rate mortgage, the first surprise is this: your regular principal-and-interest payment does not suddenly jump just because the market got grumpy. Your loan contract is still your loan contract. If your payment was affordable before the price decline, it may still be affordable after the price decline.

That is why a drop in home values does not automatically mean foreclosure or financial ruin. A falling market is not the same thing as a missed payment. Plenty of homeowners can ride out a price decline if they have stable income, a manageable monthly payment, and no urgent reason to sell.

What does change is your household balance sheet. Your home may be worth less on paper, which means your equity shrinks. That can feel abstract until you want to do something with that equity, like refinance, sell, remove PMI, open a HELOC, or use your home as a financial safety valve. Then it becomes very real, very fast, and very annoying.

The Equity Math Can Turn Mean Quickly

Here is the cleanest example. Suppose you bought a home for $500,000 with 10% down. You put down $50,000 and borrowed $450,000. If the home’s value falls 20%, the market value drops to $400,000.

Now look at the math. On day one, ignoring principal paydown, you owe $450,000 on a house worth $400,000. Congratulations, the market has handed you negative equity and absolutely no trophy.

This is why recent buyers are often the most exposed in a sharp downturn. If you bought recently with a small down payment, you have less equity cushion. If you bought years ago, made steady payments, and benefited from earlier appreciation, you may still have plenty of equity even after a 20% drop. One homeowner feels bruised. Another feels trapped. Same housing market, very different experience.

Negative equity matters because it limits flexibility. You may not be able to sell without bringing cash to closing. You may find refinancing harder because your loan-to-value ratio is now too high. You may lose the ability to tap equity for renovations, emergencies, or debt consolidation. And if life throws a second problem into the mix, such as job loss, divorce, or medical bills, a house that cannot be sold easily becomes a heavy financial object instead of a helpful asset.

PMI, Refinancing, and Home Equity Loans Get Trickier

When home values drop, loan-to-value ratios rise. Lenders care deeply about that ratio because it tells them how much cushion exists between the loan balance and the property value. A higher LTV can mean less favorable refinance terms, a denied cash-out refinance, trouble removing private mortgage insurance, or stricter standards for a HELOC.

So even if your monthly mortgage payment stays the same, your financial options may narrow. That is one of the less dramatic but very real effects of a housing downturn. It is not always a cinematic foreclosure scene. Sometimes it is simply a family discovering that the refinance plan they were counting on has quietly evaporated.

What Sellers and Buyers Do Next

Sellers Lose Pricing Power

If housing prices fall 20%, sellers usually move through the five classic stages of grief: confidence, denial, strategic repainting, price cut, and “maybe we’ll just wait until spring.”

In a declining market, listings sit longer. Buyers negotiate harder. Price reductions become normal instead of embarrassing. The polished confidence of “we expect multiple offers by Tuesday” turns into “the seller is willing to include appliances, patio furniture, and possibly emotional support.”

People who do not need to move may simply stay put. But homeowners who must move for work, family, or financial reasons often take the hit. If they have enough equity, they may still sell, just at a lower gain than expected. If they do not have enough equity, they may delay listing, rent out the property, attempt a short sale, or bring cash to closing.

Buyers May Get Lower Prices, but Not Always an Easy Ride

On paper, falling prices sound great for buyers. And yes, lower prices can improve the sticker affordability of homes. A house that was once wildly out of reach may drift back into reality. Buyers may also gain negotiating power, more time to think, and less pressure to waive every safeguard known to humankind.

But lower prices do not always mean easy affordability. If mortgage rates remain high, the monthly payment may still be painful. A cheaper house financed at an expensive rate can still produce a payment that makes your spreadsheet sigh heavily.

There is also a psychological problem. When prices are falling, many buyers wait for them to fall more. That reduces demand further. Lenders may respond by tightening standards. Appraisals can become more conservative. Suddenly the market is cheaper, but also more cautious, slower, and less forgiving.

So buyers can benefit from a 20% drop, especially first-time buyers with stable income and strong credit. But they do not necessarily enter a magical paradise of cheap homes and free kitchen islands. They enter a market that may finally offer leverage, but also more uncertainty.

What Happens to the Broader Economy

Consumer Confidence Often Takes a Hit

Housing is not just shelter. For many households, it is the biggest asset they own. When that asset falls in value, people tend to feel less wealthy, less confident, and less eager to spend. That can show up in smaller ways first: fewer renovations, fewer big purchases, less travel, less willingness to take financial risks.

When millions of households all become a bit more cautious at the same time, the broader economy notices. Furniture stores notice. Contractors notice. Car dealerships notice. Economists, who are famously allergic to drama unless it is in a chart, notice too.

Construction and Real Estate Jobs Can Cool Down

If builders see weaker demand and softer prices, they may delay new projects, cut back starts, or rely more heavily on incentives. Real estate agents, mortgage brokers, home stagers, inspectors, movers, and renovation businesses can also feel the slowdown. Housing has a wide economic footprint. When it sneezes, a surprising number of industries reach for tissue.

This does not mean every price decline causes a deep recession. But a large housing correction can reduce activity in enough related sectors that the economic drag becomes real.

Banks and Lenders Get More Defensive

When collateral values fall, lenders usually become more careful. They may tighten underwriting, scrutinize appraisals, reduce risk appetite, or charge more for certain kinds of loans. That can create a feedback loop. Less credit means fewer qualified buyers. Fewer buyers can mean more downward pressure on prices.

This is one reason housing downturns can feel sticky. They are not only about lower prices. They are about the changing behavior of the people and institutions around those prices.

Local Governments Can Feel It Too

Home prices do not translate instantly into lower property tax bills because assessments often lag and local rules vary. Still, over time, weaker home values can put pressure on local tax bases, especially in places already dealing with budget stress. That can affect everything from school funding debates to infrastructure plans. Real estate is local, and so are many of the consequences.

Does a 20% Drop Automatically Mean Another 2008?

No. That is the headline answer, and it matters.

A 20% drop would be serious, but it would not automatically recreate the 2008 housing crash beat for beat. The conditions matter. The financial crisis was made worse by risky lending, speculative excess, fragile mortgage products, widespread negative equity, and a brutal recession. Prices fell, yes, but the damage became historic because many borrowers were poorly positioned to absorb the shock.

Today, many homeowners still have fixed-rate mortgages they locked in at low rates. Underwriting standards have generally been tighter than they were in the bubble era. Many existing owners also have larger equity cushions than homeowners had going into the last crash. Those are meaningful shock absorbers.

That said, “not automatically 2008” does not mean “totally fine, carry on.” A 20% national decline would still hurt. Recent buyers, investors with thin margins, overleveraged owners, and anyone forced to sell in a weak market could face real pain. If falling home prices happened alongside rising unemployment, then the risks would multiply. Housing trouble becomes much more dangerous when it teams up with income trouble. That duo has terrible chemistry and a long history.

What Different People Should Worry About Most

If You Already Own a Home

Your biggest question is not “What does the market say today?” It is “Do I need to move, borrow, or refinance soon?” If the answer is no, and your mortgage is affordable, a price drop may be unpleasant but survivable. You live in a home, not a stock ticker.

If the answer is yes, then equity becomes everything. Know your loan balance. Know your local market value. Know what selling costs would look like. People get into trouble when they assume last year’s value is still sitting there politely waiting for them.

If You Want to Buy

A falling market can create opportunity, but only if you buy for the right reasons. If you plan to stay for years, can comfortably afford the payment, and have reserves, buying during a downturn can work out very well. If you are counting on quick appreciation to save a stretched budget, you are basically asking the market to babysit your decision, and markets are not nurturing.

If You Are an Investor

A 20% drop can create bargains, but it can also expose weak cash flow assumptions. Investors who bought with rosy rent projections, thin margins, or short-term financing may discover that “passive income” can become “actively stressful” when prices and sentiment turn south.

What Households Should Actually Do in This Scenario

If prices fall sharply, the smart move is usually boring, which is unfortunate for social media but excellent for real life.

First, protect liquidity. Cash is more useful than wishful thinking. A larger emergency fund matters more in a soft market because selling quickly may be difficult or expensive.

Second, avoid panic selling unless you truly need to move. A paper loss becomes permanent the moment you lock it in. If the home is affordable and fits your life, time can be your ally.

Third, understand your loan. A fixed-rate mortgage behaves differently from an adjustable-rate loan. Know whether you have PMI, when it can be removed, and how a lower appraisal could affect future options.

Fourth, do not treat your home like an ATM just because it behaved like one in the boom years. Falling markets are when households learn the difference between wealth and accessible wealth.

And finally, if you are in trouble, act early. Loan servicers are not famous for creating joy, but they are easier to work with before missed payments turn into a full crisis. Waiting until the problem is on fire rarely improves the paperwork.

Experiences From a 20% Housing Price Drop

Consider three common experiences that show how uneven a 20% price decline can feel.

The first is the recent buyer. Imagine a young couple who bought a starter home with 5% down after losing bidding war after bidding war. They finally got the keys, painted the nursery, and felt like they had outrun the market. Then prices slid. One year later, they discover their home is worth less than what they paid, and after closing costs they cannot sell without writing a check. They are not broke, and they are not automatically in danger, but they feel stuck. Their home has shifted from dream purchase to long-term commitment in a hurry. Their experience is emotional as much as financial. They stop thinking about upgrades and start thinking about patience.

The second is the long-time owner. She bought her home ten years ago, refinanced at a low fixed rate, and has built substantial equity. When prices fall 20%, she does not like it, but it does not derail her life. She still has room between what she owes and what the house is worth. Her payment is stable. She keeps living normally, although she postpones a cash-out remodel because the new math is less attractive. For her, the price decline is more of a psychological bruise than a financial emergency. She loses paper wealth, not her footing.

The third is the forced seller. He planned to stay, but a job transfer lands in another state. In a rising market, he would have sold quickly and left with a tidy gain. In a falling market, buyers are pickier, offers come in lower, and the timeline gets messy. He cuts the price twice, pays for repairs he thought he could ignore, and still gets less than expected. The move happens anyway because life does not wait for perfect market conditions. This is where falling prices hurt most: not always in theory, but in moments when people need flexibility and the market refuses to cooperate.

Then there is the first-time buyer watching from the sidelines. For years, every headline basically translated to “good luck, kid.” Suddenly, prices soften, open houses feel calmer, and negotiating is no longer a blood sport. This buyer has a stable income, a solid down payment, and the discipline to buy only what fits the budget. For this person, a 20% drop may be the first moment the market feels rational. It is not joyful for everyone, but it can open a door that had been locked for years.

These experiences matter because they reveal the truth behind the headline. A 20% fall in housing prices is not one story. It is a collection of very different stories happening at the same time: stress for some, relief for others, inconvenience for many, and opportunity for the patient. The market moves in averages. Real people do not.

Final Thoughts

If housing prices fall 20%, the biggest effects are usually not mysterious. Equity shrinks. Recent buyers become vulnerable. Refinancing gets harder. Sellers lose leverage. Some buyers gain opportunity. Lenders get cautious. Consumer spending can cool. And if job losses join the party, the situation gets more serious very quickly.

But a falling market does not doom every homeowner, and it does not guarantee a replay of the last housing crash. The real question is not whether prices fell. The real question is who has enough income, equity, patience, and flexibility to handle the fall. In housing, gravity matters. Balance sheets matter more.